Sales Flat for Three Years, Cash Drops by 70% – XREAL Pushes for Hong Kong Stock Listing, What Secrets Are Hidden in the Prospectus?

04/03 2026

04/03 2026

706

706

On April 1, 2026, Chinese AR glasses company XREAL submitted its prospectus to the Hong Kong Stock Exchange, with the ambition of becoming the "pioneer global smart glasses stock."

Founder Xu Chi posted on WeChat Moments: "The tenth year of XREAL marks a fresh start."

Image source: WeChat Moments of XREAL founder Xu Chi

This statement carries different significance for different individuals. For investors who have endured 12 rounds of financing, it might signify a long-awaited exit opportunity; for potential new investors, it represents a 354-page document that requires careful analysis.

The prospectus is at hand. Let's delve into the figures.

01

Doubled Gross Margin Amidst Negative Sales Growth

Let's begin with the positives.

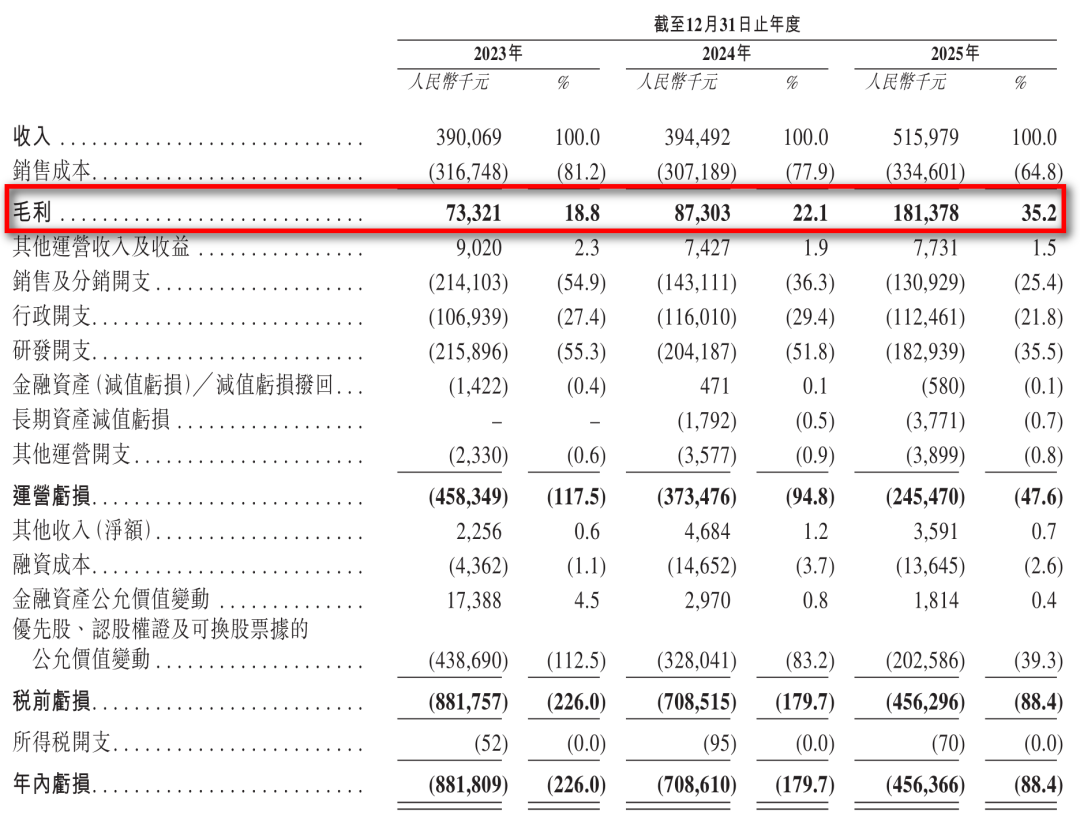

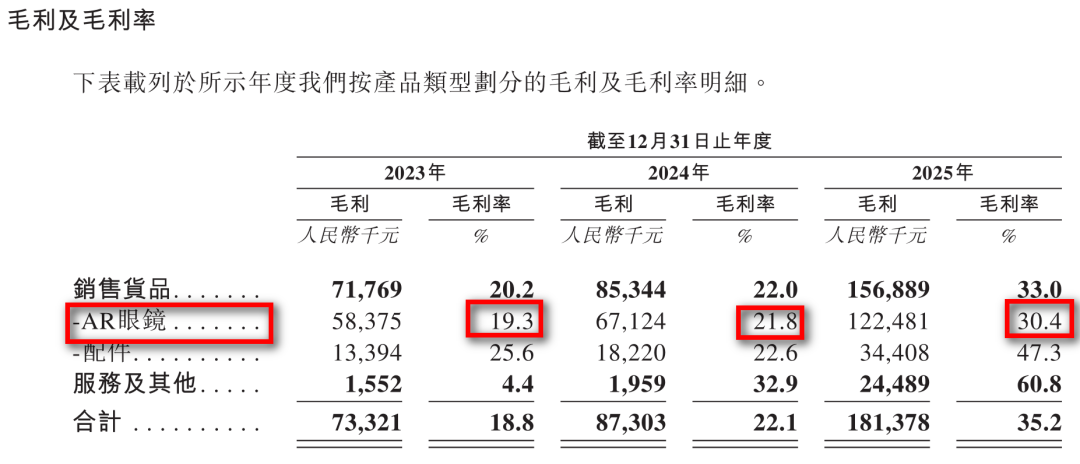

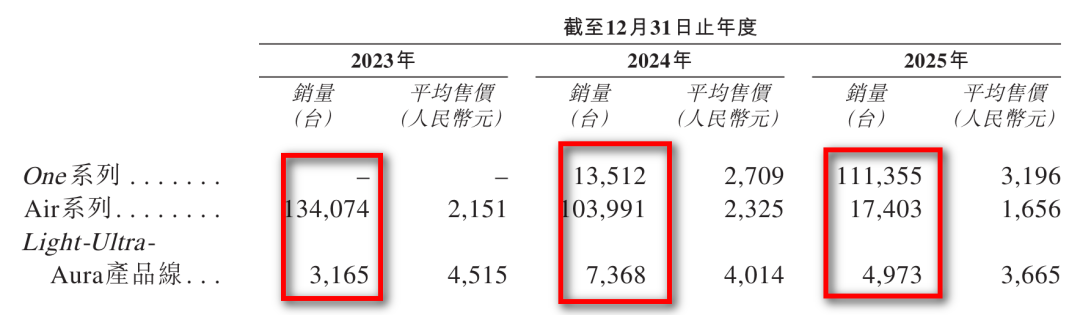

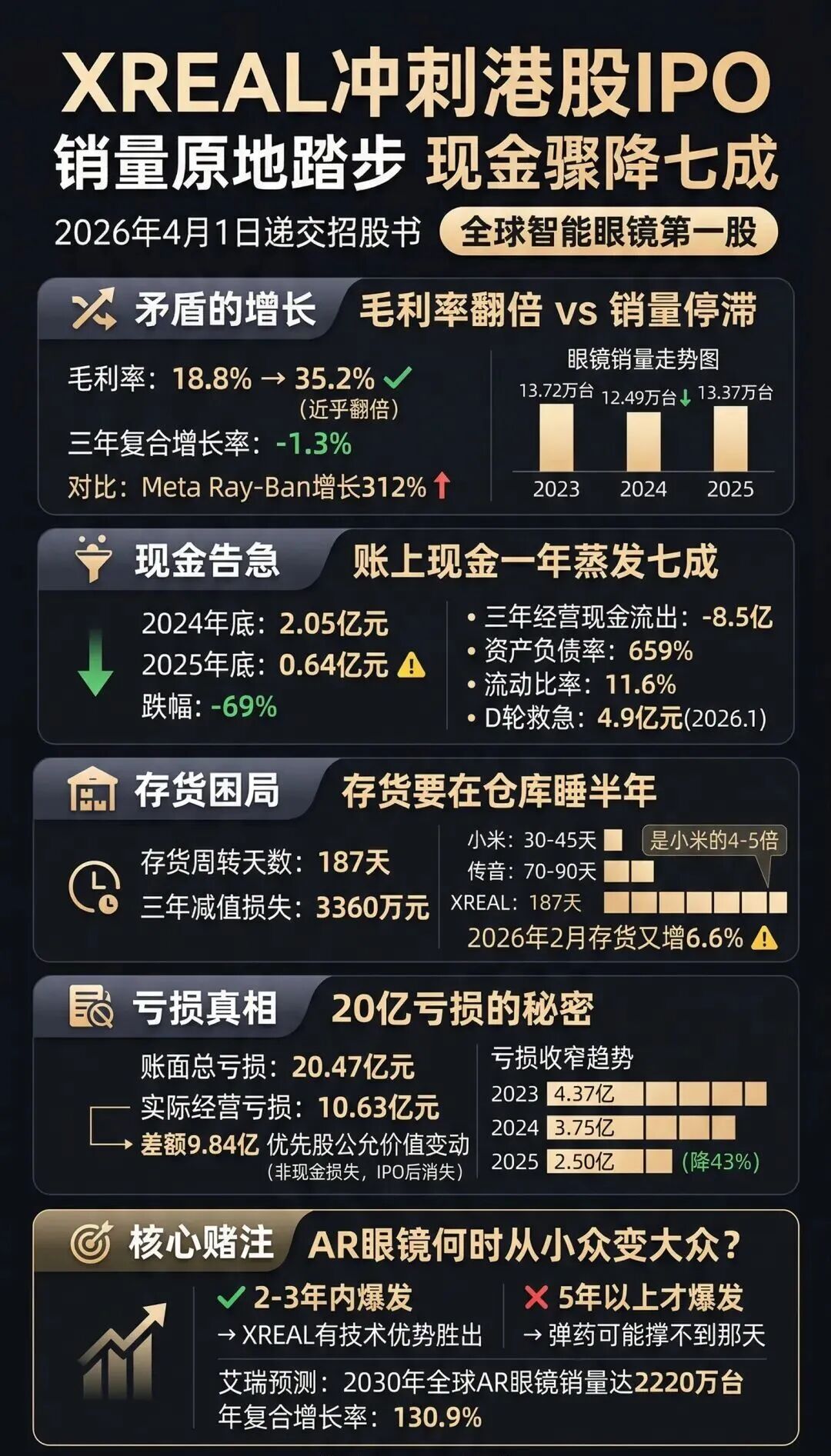

Over the past three years, XREAL has excelled in one key area: it has boosted its gross margin from 18.8% to 35.2%, nearly doubling it, without significant revenue growth. Such an achievement is uncommon in the consumer electronics hardware sector. The underlying logic is clear—the high-priced One series (averaging RMB 3,196) has sold 111,400 units over three years, contributing 69% of total revenue; concurrently, production costs have continued to decline, with the gross margin of AR glasses rising from 19.3% to 30.4%. The high-end strategy has proven financially rewarding.

Image source: XREAL prospectus

Image source: XREAL prospectus

The prospectus reveals: "According to iResearch data, we ranked first globally in the AR glasses market by sales revenue annually from 2022 to 2025; and ranked second globally in the entire smart glasses market (including AR glasses and non-display glasses) by 2025 sales revenue, and first in China."

However, behind these accomplishments lies an undeniable contradiction:

Glasses shipments have actually decreased over three years.

Image source: XREAL prospectus

In 2023, 137,200 units were shipped, dropping to 124,900 units in 2024, and rebounding slightly to 133,700 units in 2025. The two-year compound annual growth rate was -1.3%.

In other words, the gross margin improvement was not driven by increased sales volume but by selling more expensive products—while simultaneously reducing marketing expenses (from RMB 214 million to RMB 131 million) and R&D spending (from RMB 216 million to RMB 183 million). This strategy aims to maximize profit margins within a limited market scale, enhancing financial statements but not necessarily expanding the market.

Meanwhile, the entire smart glasses industry has been evolving. XR Institute data indicates that Meta's Ray-Ban series shipped 1.7 million units in 2024 and exceeded 7 million units in annual sales by 2025, a year-on-year increase of 312%. In contrast, XREAL's growth during the same period was only 7%, a performance hardly indicative of a "growth-stage" company.

02

Where Has the Cash Gone?

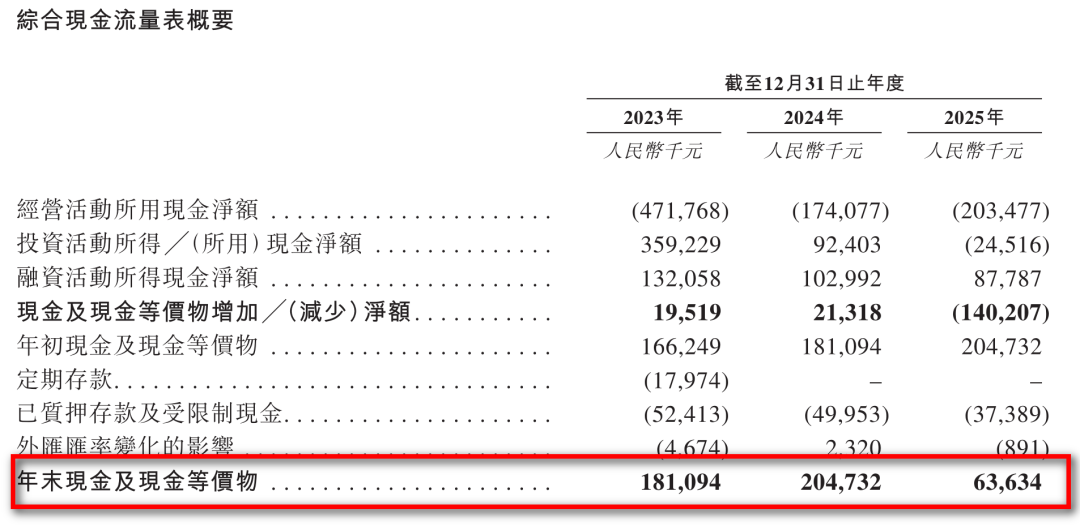

By the end of 2025, XREAL's cash and cash equivalents had dwindled to just RMB 63.63 million.

At the end of 2024, this figure stood at RMB 205 million. Within a year, it had shrunk by nearly 70%.

Image source: XREAL prospectus

Where did the cash disappear? Three factors provide a clear explanation.

Firstly, persistent operational losses. In 2025, the net cash outflow from operating activities was RMB 203 million—not an isolated incident but a three-year trend. In 2023, it was RMB 472 million; in 2024, RMB 174 million; totaling RMB 850 million over three years. The outflow narrowed but did not turn positive.

Secondly, financing activities offered little relief. In 2025, the net cash inflow from financing activities was just RMB 88 million, primarily from rolling over short-term bank loans—borrowing RMB 670 million while repaying RMB 658 million, a net increase of RMB 12 million. No new equity financing materialized in fiscal 2025.

Thirdly, capital expenditures surged at this critical juncture. In 2025, they reached RMB 4.27 million, 2.74 times the RMB 1.56 million in 2024, a 174% year-on-year increase. This investment went towards the Wuxi optical module production base—building in-house production lines is a necessary step to reduce long-term costs, logically sound, but choosing to ramp up spending during the year with the tightest cash flow objectively accelerated depletion.

These three factors combined explain why only RMB 63.63 million remained in the accounts by the end of 2025.

In essence, XREAL experienced an extremely precarious 'asset shift' in 2025: cash (liquid assets) transformed into inventory (warehouse accumulations). This 'anemic' state persisted until the filing, when the RMB 490 million Series D 'lifeline' arrived in January 2026, barely reoxygenating the balance sheet.

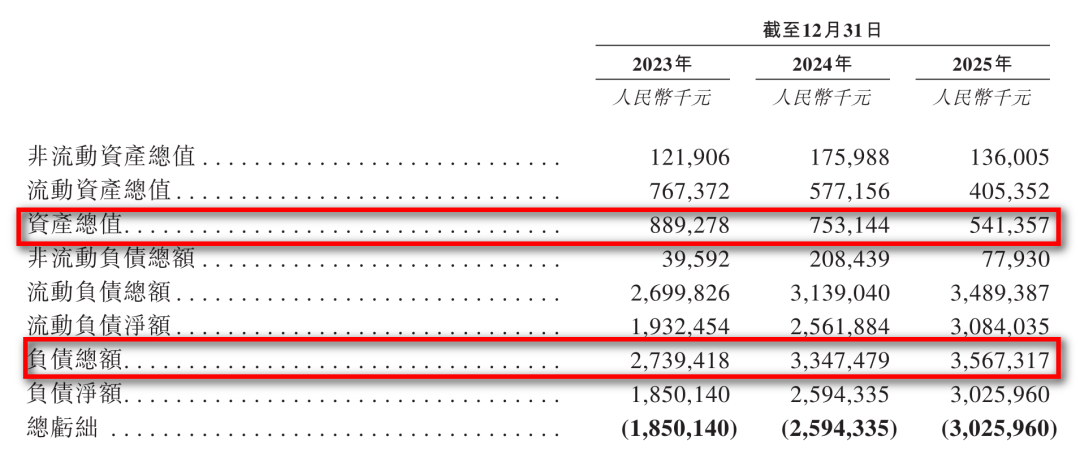

The balance sheet presents an even more alarming picture: total assets of RMB 541 million, total liabilities of RMB 3.567 billion, a debt-to-asset ratio of 659%, and a current ratio of just 11.6%—current assets cover only one-ninth of current liabilities.

Image source: XREAL prospectus

An important clarification is needed here: of the RMB 3.567 billion in total liabilities, RMB 2.924 billion consists of preferred shares, warrants, and convertible notes, which must be recorded on the liability side under IFRS accounting standards but are essentially accumulations from previous financing rounds, not traditional debt requiring principal and interest repayments. Once the IPO is completed, these will convert to ordinary shares, significantly reducing the liability scale. This is a common accounting presentation issue for Pre-IPO startups, not a risk unique to XREAL.

After excluding this accounting treatment, while the company's actual operational liability pressure is not as extreme as 659%, the liquidity crunch is very real. Going public may be the most realistic path to address it.

03

Inventory: Not Soy Sauce—The Longer It 'Ages,' the Worse It Gets

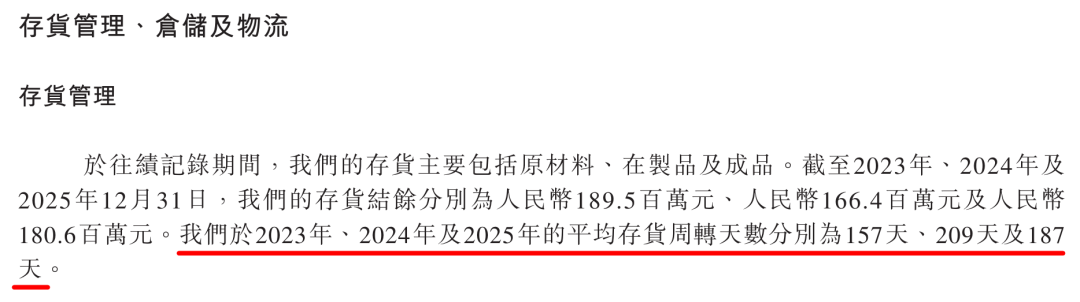

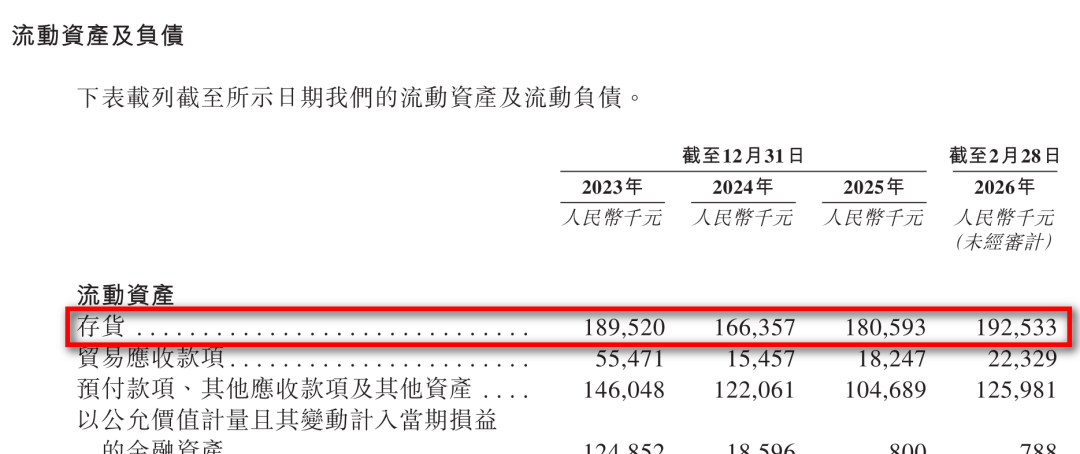

The prospectus discloses that XREAL's average inventory turnover days were 157, 209, and 187 days from 2023 to 2025, respectively.

A soy sauce ad might say, "Just let it age here for 180 days." But inventory is not soy sauce—in the fast-paced consumer electronics industry, the longer inventory 'ages,' the faster its value diminishes.

Image source: XREAL prospectus

A cross-industry comparison in consumer electronics highlights the issue:

Inventory Turnover Days (Recent Years) Apple: ~6–9 days Samsung: ~60–75 days Xiaomi: ~30–45 days Transsion Holdings: ~70–90 days Huawei: ~80–100 days (estimated) XREAL: 187 days

Apple's 6 days represent extreme optimization and are not directly comparable. However, Transsion, a phone maker targeting emerging markets with a less optimized supply chain, still maintains inventory turnover under 90 days. XREAL's 187 days, roughly 4–5 times Xiaomi's, means a batch of goods takes over six months on average to move from warehouse to sale.

Structural reasons exist. AR glasses are not phones; strategic materials like the X1 chip require 3–6 months of inventory, and product warehouses are scattered across eight locations in Japan, Europe, and North America, with cross-border logistics inherently lengthening cycles. The prospectus provides reasonable explanations for this.

But structural reasons do not eliminate risks. A 187-day turnover cycle in an industry where new products iterate annually means sustained impairment pressure—XREAL's inventory write-downs were RMB 12.2 million, RMB 13 million, and RMB 8.4 million over three years. The deeper question is: when the One Pro launches, how long will it take to clear previous-generation products stuck in eight global warehouses?

In consumer electronics, a 187-day turnover means your products spend at least as long in warehouses as they do undergoing technological iteration. While competitors 'blitz' the market at a fast pace, XREAL is 'jogging' with six months of inventory. This is not just a financial risk.

More concerningly: before filing the prospectus in February 2026, its unaudited inventory figure had risen another 6.6%. With sales stagnant for three years, this counter-trend leverage buildup is truly puzzling.

Image source: XREAL prospectus

04

RMB 2 Billion Loss: What's 'Real'?

XREAL's cumulative net loss of RMB 2.047 billion over three years is the most prominent figure in the prospectus and the one most frequently cited in various articles.

But accounting losses and operational losses are not the same. It's necessary to dissect this.

The prospectus also discloses adjusted net losses excluding non-cash items: RMB 437 million in 2023, RMB 375 million in 2024, and RMB 250 million in 2025, totaling RMB 1.063 billion over three years.

The roughly RMB 984 million difference between RMB 2.047 billion and RMB 1.063 billion mainly comes from fair value changes in preferred shares, warrants, and convertible notes—RMB 439 million in 2023, RMB 328 million in 2024, and RMB 203 million in 2025. These are non-cash losses: as the company's valuation rises, the fair value of these preferred shares increases, requiring accounting recognition as losses. A counterintuitive implication: the more optimistic investors are about the company and the higher its valuation, the larger this "loss" becomes. The prospectus explicitly states that this loss "is non-cash in nature and will cease to arise upon completion of the listing."

Thus, both figures have their significance: RMB 2.047 billion represents the GAAP-compliant full picture, while RMB 1.063 billion is a reference closer to operational reality. Both should be presented, not just the one favoring a preferred narrative.

Simply put, this additional RMB 984 million in losses is the company's 'appreciation bonus' to early investors, recorded as the company's debt in accounting terms. This is a 'happy worry': the higher the company's valuation, the more daunting this book loss appears.

05

Conclusion: How Big Is This Gamble?

Considering the four dimensions above, XREAL's situation can be described as: a company technically "charging ahead" but commercially still awaiting its breakthrough, attempting to knock on the Hong Kong Stock Exchange's door at the most capital-hungry moment.

This is not a simple judgment of a good or bad company.

The positives are real: doubled gross margins, a 40% narrowing of losses over three years, and an ongoing flagship collaboration with Google Android XR. iResearch predicts global AR glasses sales will rise from ~800,000 units in 2026 to 22.2 million units by 2030, a CAGR of 130.9%. If this inflection point arrives, XREAL is one of the few players positioned to seize it.

The difficulties are equally real: sales have barely changed in three years, only RMB 63.63 million in cash remains, and inventory lingers in warehouses for over half a year annually.

The core of this gamble is a judgment call on timing: how long will it take for AR display glasses to transition from niche tech products to mass consumer goods?

If it takes two to three years, XREAL has sufficient technical reserves and market position to win this race. Its collaboration with Google's Project Aura, the ASUS ROG co-branding, and the Wuxi in-house production line under construction are all bets on this timeline.

If it takes five years or longer, current resources may not last that long. And going public is, to some extent, about keeping this gamble alive.

The "warning" on the prospectus cover thus reads especially true:

"Whether the Company will proceed with the offering remains uncertain."

Image source: AR Circle

END

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models