Has Beike Been 'Kneeling for Too Long': A Genuine Turnaround or Just a Temporary Rebound?

05/20 2026

05/20 2026

568

568

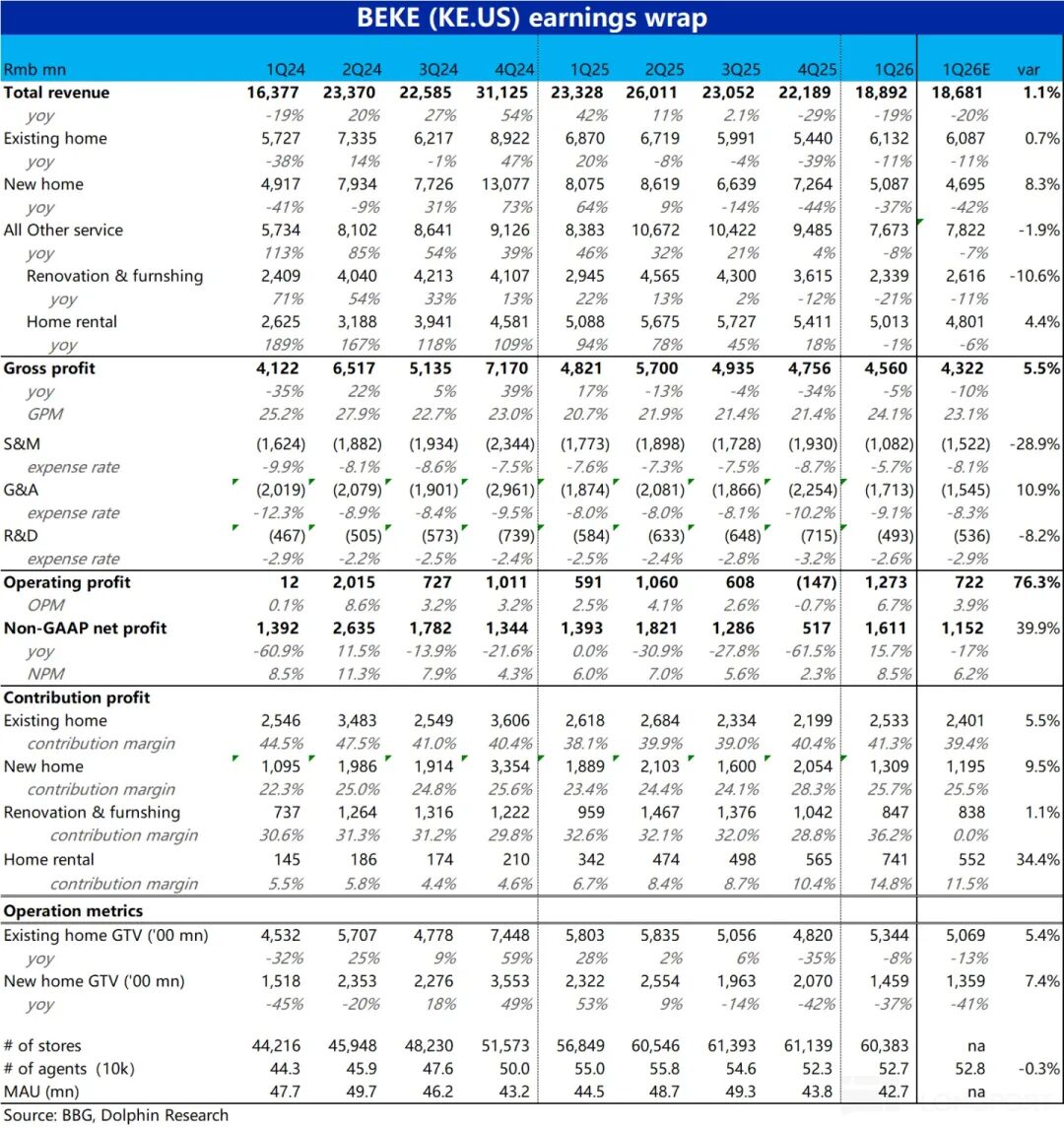

Beike (BEKE.US), a frontrunner among domestic real estate service providers, unveiled its Q1 2026 financial results prior to the U.S. market opening on May 19. Overall, despite signs of stabilization in the property market, it remains in a challenging phase. Adjustments in home renovation and leasing services have notably contributed to a significant drop in revenue. Nevertheless, by proactively streamlining its workforce, enhancing gross margins, and curbing expenses, the company has exceeded profit expectations by a wide margin. Here are the details:

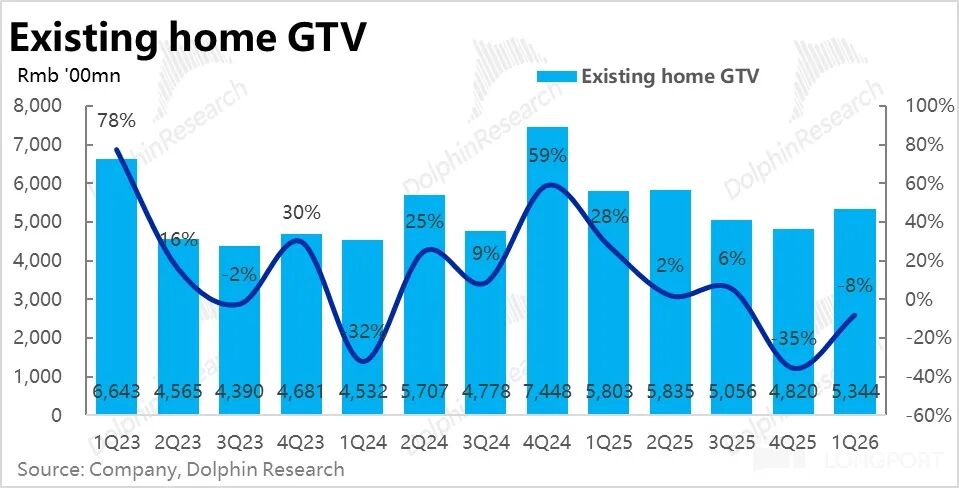

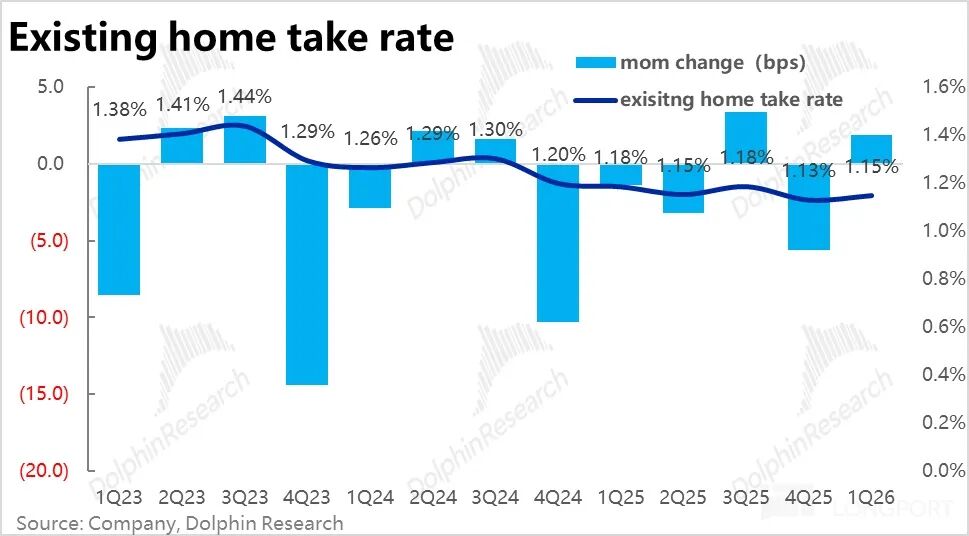

1. Stabilization in the Existing Home Market: A series of policy support measures, including easing purchase restrictions and raising housing provident fund loan limits, were announced in top-tier cities during February and March. Consequently, the core existing home business exhibited signs of recovery and stabilization this quarter. Although the Gross Transaction Value (GTV) still decreased by approximately 8% year-over-year, it surged by about 11% sequentially.

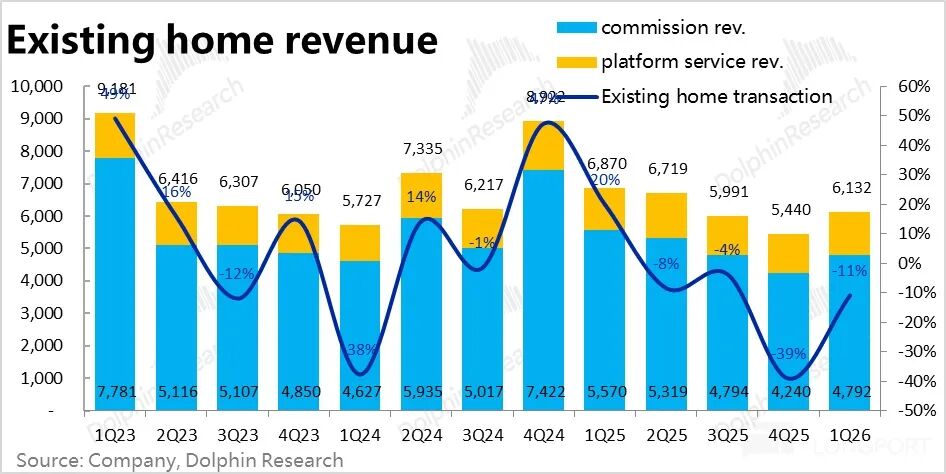

Notably, GTV growth in the franchised channel significantly outpaced that of the self-operated Lianjia channel. With improved platform monetization and a rebound in the second-hand housing market reducing the need for commission discounts to close deals, the overall monetization rate for existing homes rose by 1.9 basis points sequentially, indicating enhanced profitability in this segment.

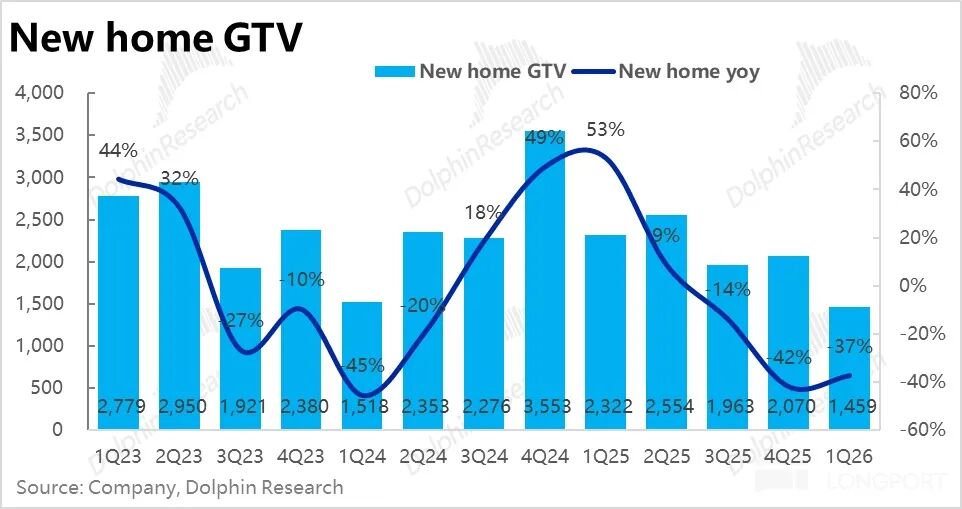

2. Persistent Pressure in the New Home Market: Despite a slight year-over-year improvement in the decline of new home GTV compared to the previous quarter, it still plummeted by 37%, largely mirroring the sluggish sales of high-value new homes in major cities like Beijing and Shanghai following new policies.

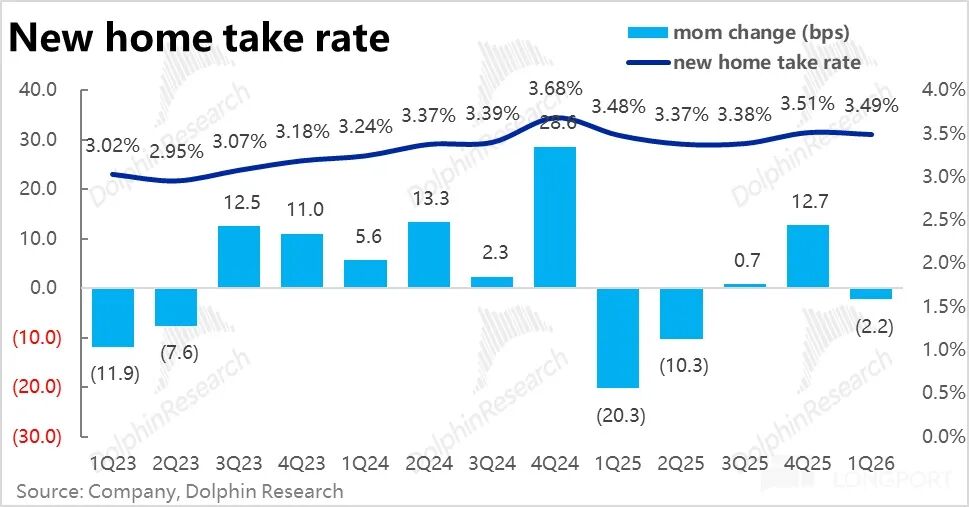

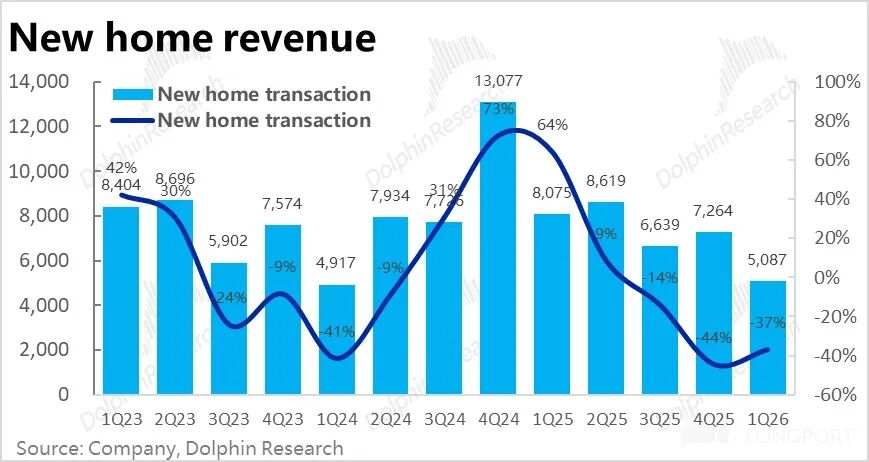

Moreover, the comprehensive monetization rate for the new home business slightly dipped by about 2 basis points from the previous quarter's peak, though this was more of a minor fluctuation than a trend. Consequently, new home revenue also tumbled by approximately 37%.

However, Bloomberg's consensus forecasted a 42% decline in new home revenue, making the actual performance better than anticipated from a variance perspective.

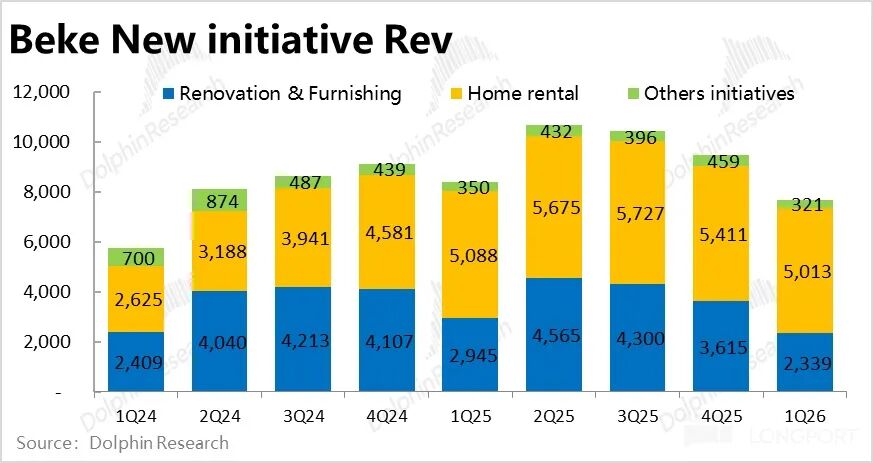

3. Adjustments in Second-Track Businesses: Growth in second-track businesses appeared generally sluggish at first glance, with combined revenue declining by 8% year-over-year. This was primarily due to a 21% year-over-year drop in home renovation revenue, significantly below expectations.

The reasons included not only poor new home sales dampening renovation demand but also the company's strategic shutdown of some low-quality businesses and retraction in certain cities. This marked a temporary setback for the vision of replicating Beike's success through home renovations.

Leasing business revenue also decreased by 1% year-over-year due to a change in the revenue recognition method for "hassle-free rentals" to net revenue. However, the number of properties under management soared by approximately 47% year-over-year, indicating robust actual growth when accounting for the change.

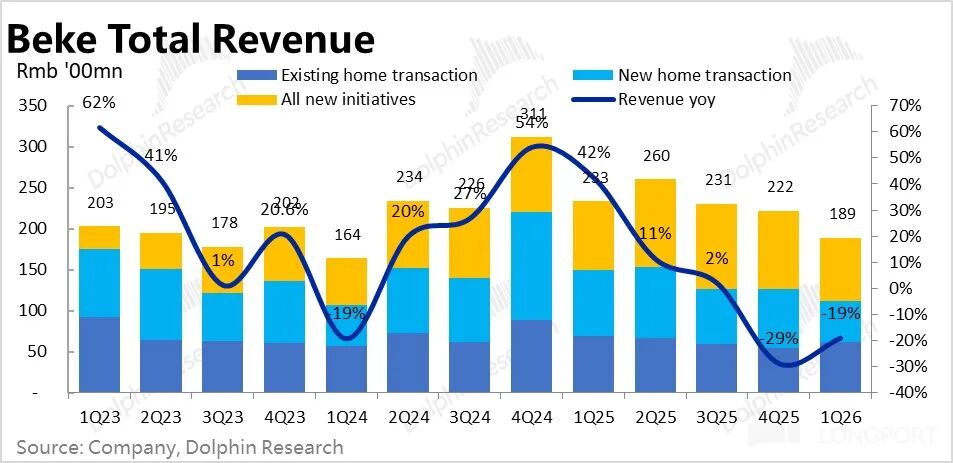

4. Profit as the Highlight: Overall, Beike's total revenue still declined by about 19% year-over-year, largely in line with expectations. However, the highlight of this quarter's performance was not growth but the impressive profit release.

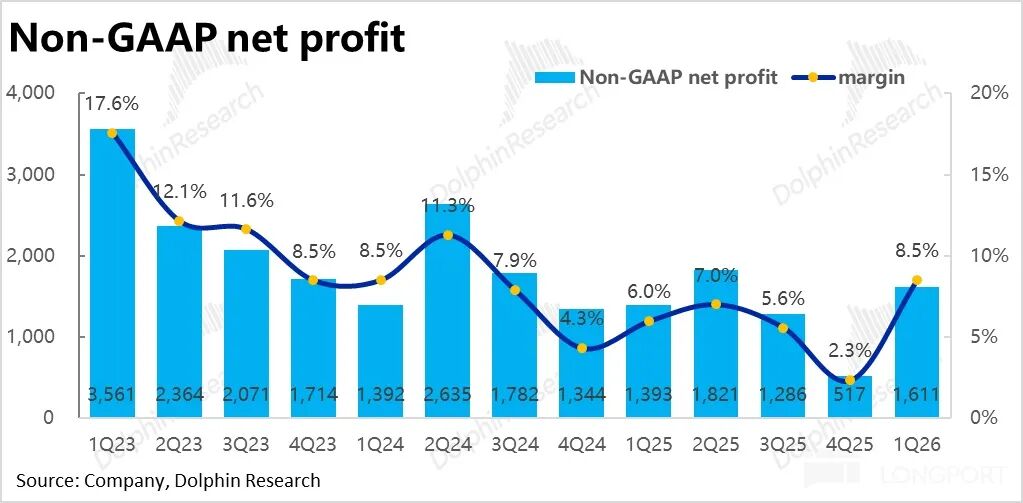

In terms of profit, the adjusted net profit was approximately RMB 1.6 billion, increasing by nearly 16% year-over-year, significantly surpassing the market consensus of around RMB 1.15 billion. This once again showcased the company's ability to deliver profits amid adversity.

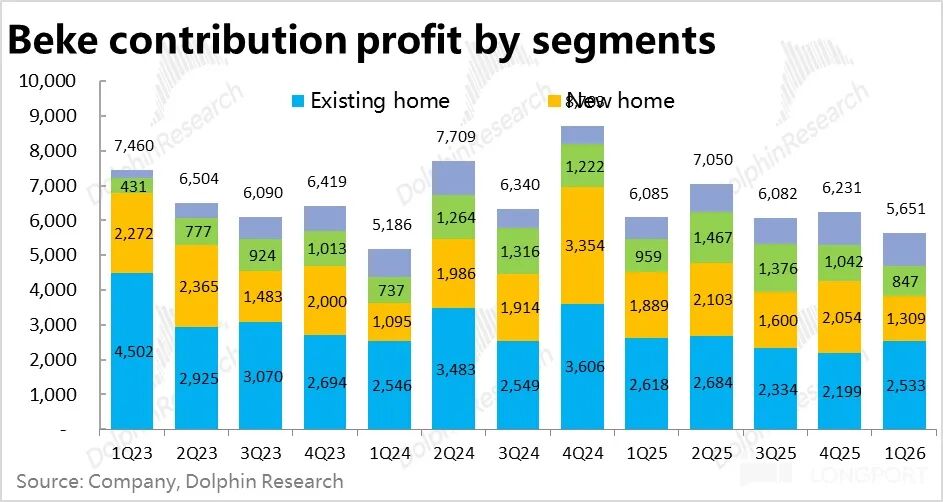

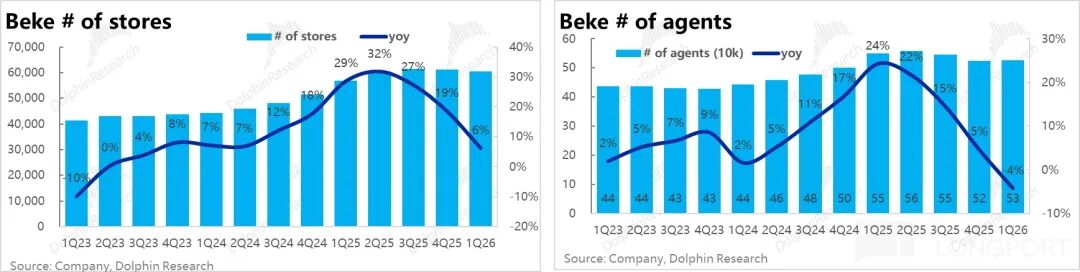

5. Generally Improving Profit Margins Across Segments: Despite shrinking business volumes, which are typically unfavorable for operating leverage and profit release, profit margins generally improved across segments through proactive optimization of store and personnel counts, enhanced personnel efficiency, and strict expense control.

Within the first-track businesses, the contribution margin for existing homes improved by 0.9 percentage points sequentially and over 3 percentage points year-over-year; for new homes, despite a significant GTV decline, the contribution margin still improved by about 2.3 percentage points year-over-year.

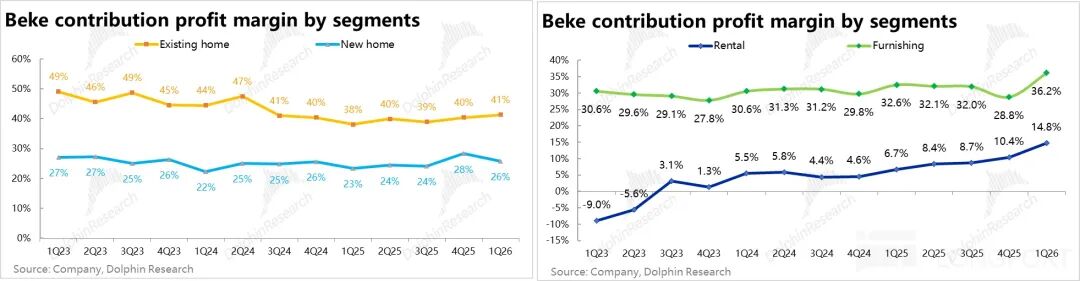

Within the second-track businesses, the home renovation business saw a substantial year-over-year increase of about 5.6 percentage points in its contribution margin due to the divestiture of some low-quality businesses and optimization of the upstream supply chain, reducing procurement costs.

The leasing business also witnessed a significant sequential increase of about 4.4 percentage points in its contribution margin to 14.8%, driven by rapid growth in net revenue from "hassle-free rentals," making it the segment that exceeded expectations the most.

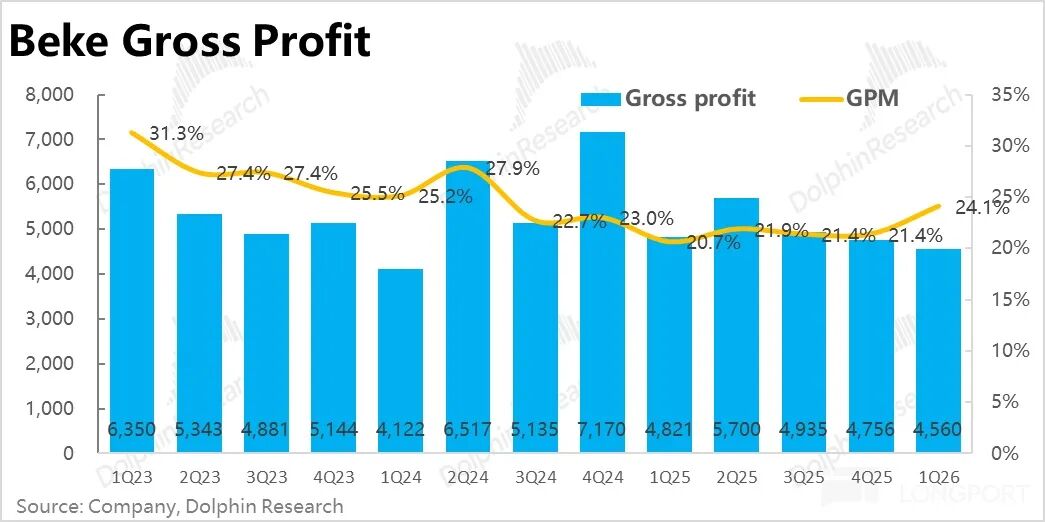

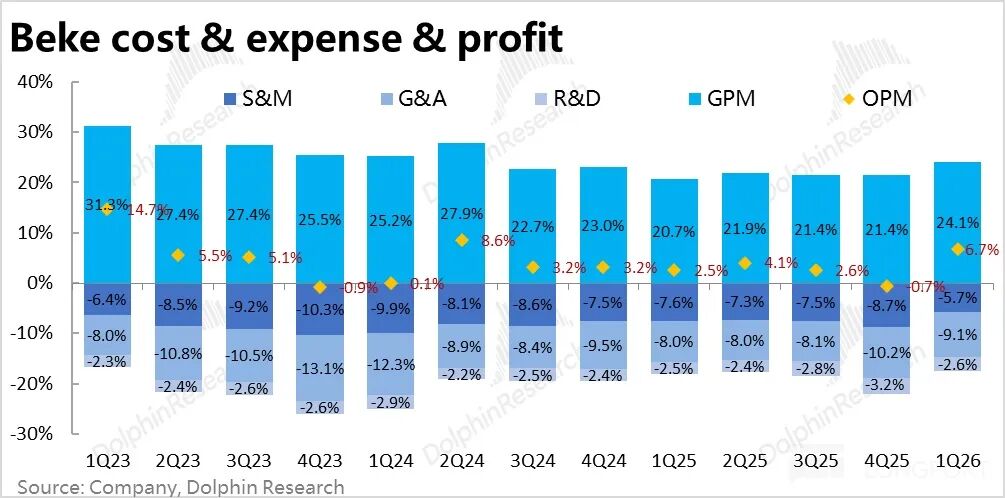

6. Gross Margin & Cost Control Drive Profit Release: From a cost and expense perspective, Beike's overall gross margin reached 24% this quarter, up significantly from 21.4% in the previous quarter, resulting in gross profit only declining by about 5% year-over-year. Besides favorable gross margin improvements in home renovation and leasing businesses, overall commission sharing in the first-track businesses decreased by 29% year-over-year, a larger decline than revenue.

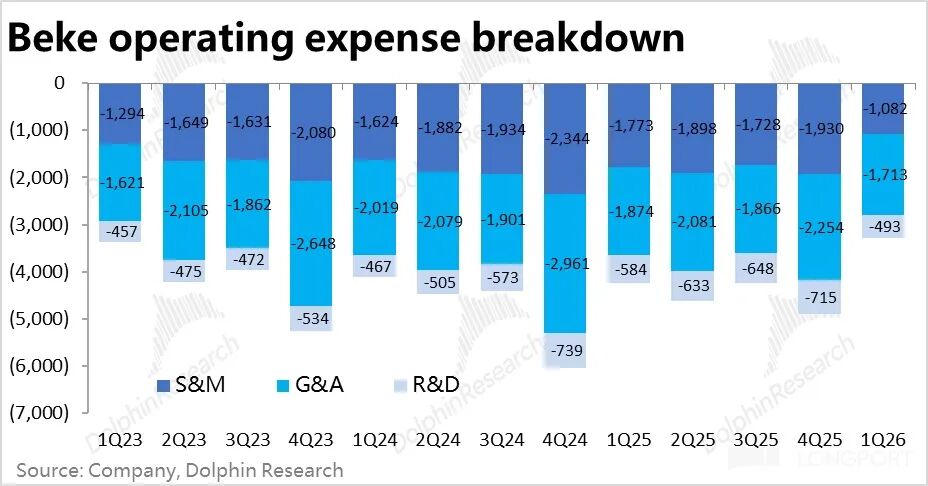

Strict cost control also played a pivotal role, with total operating expenses declining by about 22% year-over-year vs. a 19% year-over-year decline in total revenue. Marketing expenses fell by about 39% year-over-year, as the home renovation business proactively contracted, leading to a significant reduction in marketing and customer acquisition investments.

Administrative and R&D expenses also decreased by about 9% and 16%, respectively. The reduction in administrative expenses mainly reflected decreased stock-based compensation.

With the dual support of an improved business structure and effective cost control, profit release far exceeded expectations.

Dolphin Research View:

As observed, Beike's absolute performance this quarter remains lackluster—despite signs of recovery in second-hand housing transactions in top-tier cities during Q1 under policy support. However, new home transactions remain sluggish, and the home renovation business, which was highly anticipated, has officially declared a temporary "setback." Additionally, a high base from last year contributed to the company's revenue growth remaining deeply negative.

From a variance and dynamic marginal change perspective, declines in the first-track agency businesses did narrow and slightly outperformed more pessimistic market expectations. While revenue declines in second-track businesses, especially home renovations, were indeed more severe than expected, the profit improvement under proactive contraction also far exceeded expectations, largely balancing the pros and cons. The leasing business, meanwhile, has consistently performed well, growing against the trend.

More critically, the company has a history of significantly releasing profits through strict cost control and efficiency improvements during challenging periods, while during macroeconomic improvements, revenue growth may not translate into proportional profit growth due to expansionary investments.

Currently, the company's cost control and efficiency improvement phase coincide with the release of policy dividends. If the company refrains from disruptive actions, a dual-cycle of revenue growth recovery and profit improvement may emerge in the near term.

Of course, besides the company's proactive cost reduction and efficiency improvements, support policies announced by a series of top-tier cities, including Shanghai and Shenzhen, since late February have undoubtedly played a decisive role in the industry's and the company's bottoming out and recovery. The company's stock price has rebounded nearly 30% from its early April low, largely reflecting the aforementioned expected reversal.

Thus, Dolphin Research believes that whether to continue betting on Beike's investment opportunity at present depends largely on whether the recent property market recovery represents a genuine bottoming out and trend reversal or merely another temporary rebound driven by policy stimulus, as seen before.

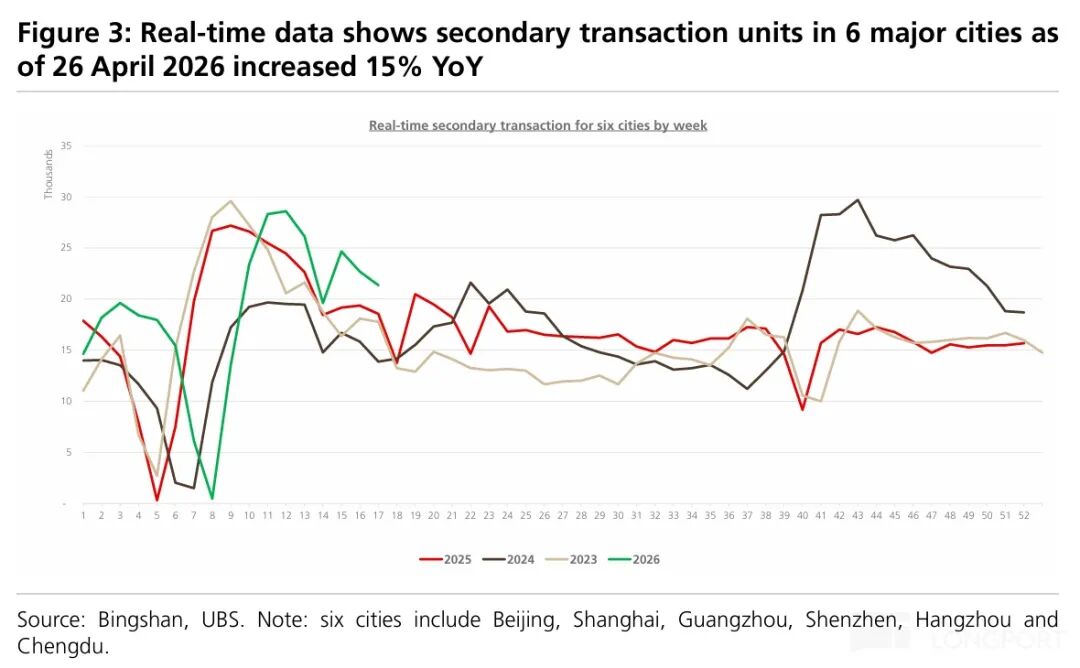

Combining recent research and the company's own disclosures, second-hand housing transactions in major domestic cities, while declining from March levels in April, remained at relatively high levels, with transaction volumes still expected to grow year-over-year. Therefore, performance pressure in Q2 should be limited.

The real question is whether the property market can sustain positive growth in the second half of the year, despite a significantly lower base. The company stated in its earnings call that it believes the previous recovery was not merely temporary but a trend reversal, noting that second-hand housing transactions have expanded from low-value rigid demand to high-value improvement-oriented demand.

However, based on current information, it is insufficient to convince Dolphin Research to agree with the judgment that the real estate market has hit a historical bottom and will trend upward. Therefore, we still view Beike as a trading opportunity within a range, considering buying at policy, sentiment, and stock price lows but taking profits at relative highs in these areas.

A more detailed value analysis has been published in the Changqiao App's "Dynamic - In-Depth" section under the same article title.

Detailed Q1 Financial Report Analysis

I. Existing Homes: GTV Growth and Monetization Rate Bottoming Out

The core existing home business, supported by a series of policy measures during February and March, showed signs of bottoming out and stabilization. Although GTV still declined by about 8% year-over-year due to a high base last year, it increased by about 11% sequentially.

This quarter, the franchised channel continued to outperform the self-operated Lianjia channel. Lianjia-led GTV still declined by nearly 15% year-over-year, while franchisee-led GTV declined by less than 4%.

Combined with previous news reports, Dolphin Research believes this was partly due to the company streamlining some self-operated stores and personnel to reduce costs and shifting its business model toward a more risk-resistant platform model.

Matching the GTV growth trend, self-operated commission revenue for existing homes was approximately RMB 4.8 billion this quarter, declining by about 14% year-over-year. However, platform service revenue increased by about 3% year-over-year vs. a nearly 4% year-over-year decline in GTV. This indicates an increase in the platform business's monetization rate.

Based on calculations, the comprehensive monetization rate for both self-operated and platform businesses was approximately 1.15% this quarter, up by 1.9 basis points sequentially. This may reflect both the favorable impact of higher platform business monetization and reduced necessity and intensity of commission discounts to close deals as existing home transactions bottomed out and rebounded.

II. New Home Business: Weaker Absolute Performance but Better Relative to Expectations

While the existing home market showed signs of stabilization, pressure in the new home sales market remained high, largely consistent with the recovery of low-value second-hand housing transactions and continued sluggish sales of high-value new homes in major cities like Beijing and Shanghai following new policies.

New home GTV declined by 37% year-over-year this quarter, an improvement from the previous quarter's decline and slightly better than market expectations, though not significantly. This compares to a roughly 25% year-over-year decline in sales for the top 100 real estate developers in Q1 this year. The larger-than-expected decline reflects both industry headwinds and Beike's proactive contraction in the new home business.

Additionally, the comprehensive monetization rate for the new home business declined slightly by about 2 basis points from the previous quarter's recent high but remained higher year-over-year. Thus, no significant trend change occurred in the new home business's monetization rate, and revenue similarly declined by about 37% year-over-year, nearly in line with GTV growth.

However, despite weaker absolute performance, Bloomberg's consensus expected a 42% decline in new home revenue, making the actual performance acceptable.

III. Second-Track Businesses Also See Negative Revenue Growth for Various Reasons

Growth in second-track businesses also appeared generally weak this quarter, with combined revenue of approximately RMB 7.67 billion, declining by 8% year-over-year.

Specifically, home renovation revenue continued its declining trend, with the year-over-year decline widening to 21% vs. market expectations of an 11% decline. According to the company, this weak performance resulted not only from poor new home sales dampening renovation demand but also from the proactive shutdown of some low-quality businesses and retraction in certain cities.

Although this was a proactive choice by the company, it essentially means the vision of recreating another Beike through home renovations can be declared a temporary setback.

Leasing business revenue also declined by 1% year-over-year, primarily due to the impact of changing the revenue recognition method for "hassle-free rentals" to net revenue. However, the number of properties under management grew by approximately 47% year-over-year, indicating strong actual growth in the leasing business.

Overall, while the revenue growth of primary businesses exhibited signs of stabilization and quarter-on-quarter recovery, it still experienced a substantial decline year-on-year. Secondary businesses, for various reasons, also witnessed negative revenue growth.

Ultimately, Beike's total revenue for this quarter plummeted by approximately 19% year-on-year, largely in line with market expectations.

IV. Breaking the Trend of Diseconomies of Scale: Profit Margins Surge

Despite lackluster revenue growth across Beike's businesses this quarter, the standout performance was the company's remarkable profit release.

Although shrinking business volumes, which typically hinder operating leverage and profitability, the company managed to improve profit margins across segments. This was achieved through proactive store and personnel reductions (with the total number of stores in the Beike ecosystem declining by nearly 760 quarter-on-quarter), enhanced personnel efficiency (Lianjia's per-capita transaction volume rose by 26% year-on-year, and per-capita commission increased by 20%), and stringent cost control. The details are as follows:

1) Primary Businesses: The profitability trend in the existing home business continued to outperform that of the new home business. Benefiting from higher comprehensive monetization rates (due to an increased proportion of platform business) and improved personnel efficiency, the existing home business's contribution margin reached 41.3% this quarter, up by about 0.9 percentage points quarter-on-quarter and over 3 percentage points year-on-year, showing significant improvement.

Although the GTV (Gross Transaction Value) for the new housing business still declined significantly, and the comprehensive realization rate also decreased slightly month-on-month, the contribution margin still improved by approximately 2.3 percentage points year-on-year (though it decreased month-on-month) due to cost control and efficiency enhancements.

2) Secondary Businesses: Within the secondary business segment, although the home improvement business is undergoing transformation with a declining business scale, the contribution margin significantly improved by approximately 5.6 percentage points year-on-year. This was attributed to the divestiture of some low-quality businesses, optimization of the upstream supply chain, and reduced procurement costs. Despite revenue falling significantly short of expectations, the contribution profit slightly exceeded expectations.

As for the leasing business, the revenue decline was primarily due to an increase in the proportion of high-margin hassle-free rentals, leading to a notable month-on-month improvement in the contribution margin by approximately 4.4 percentage points to 14.8%, reaching a new historical high. Profit exceeded expectations by approximately 34%, making it the segment that most surpassed expectations.

Due to the year-on-year improvement in contribution margins across the aforementioned segments, the company's overall contribution profit only decreased by approximately 7% year-on-year, despite total revenue declining by about 19% year-on-year.

V. Efficiency Enhancements & Stringent Cost Control Drive Profit Growth

Analyzing the reasons for profit exceeding expectations from a cost and expense perspective, we first note that the overall gross margin for Beike this quarter reached 24%, a significant increase from 21.4% in the previous quarter. Consequently, gross profit only decreased by approximately 5% year-on-year.

Specifically, in addition to the favorable impact of notable improvements in gross margins for the home improvement and leasing businesses mentioned earlier, overall commission sharing in the primary business segment decreased by 29% year-on-year, a larger decline than revenue.

Beyond the favorable impacts of business structure and gross margin improvements, Beike's stringent cost control this quarter also played a significant role. Total operating expenses decreased by approximately 22% year-on-year, compared to a 19% year-on-year decline in total revenue.

Specifically, marketing expenses saw the largest reduction, decreasing by approximately 39% year-on-year. The company emphasized that as the home improvement business entered a phase of active contraction, investments in marketing, promotion, and customer acquisition also significantly decreased.

Administrative expenses and research and development expenses also decreased by approximately 9% and 16%, respectively. The reduction in administrative expenses was primarily due to decreased equity incentives.

Therefore, with the dual support of improved business structure and effective cost control, the company's adjusted net profit for the quarter was approximately RMB 1.6 billion, increasing by nearly 16% year-on-year instead of declining, significantly higher than market expectations of approximately RMB 1.15 billion.

This once again demonstrated the company's ability to generate profits amid adversity. Moreover, gross margin improvements contributed more significantly, exceeding expectations by approximately RMB 240 million, while expenses were approximately RMB 160 million less than expected.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reprinting is only allowed with authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, aimed at users of Dolphin Research and its affiliated institutions for general reading and data reference. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report must bear their own risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available materials and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or views expressed in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall it constitute advice, inquiries, or recommendations regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for or proposed for distribution to jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials conflicts with applicable laws or regulations, or to citizens or residents of jurisdictions where Dolphin Research and/or its subsidiaries or affiliated companies are required to comply with any registration or licensing requirements in such jurisdictions.

This report only reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) make, copy, reproduce, duplicate, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models