Global Top 100, China Top 66: The 'Power Ranking' of Humanoid Robots

05/20 2026

05/20 2026

497

497

Author|Maoxinru Limurong

Over the past two days, the entire internet has been abuzz with discussions about an ultra-long live stream.

Figure AI's trio of robots autonomously sorted packages for over 150 hours, without any manual intervention.

Unlike flashy demonstrations, the ability to operate steadily in real-world scenarios over the long term is far more compelling.

This indicates that humanoid robots are transitioning from mere mobility to long-term, stable value creation—a core message of Morgan Stanley's latest humanoid robot report.

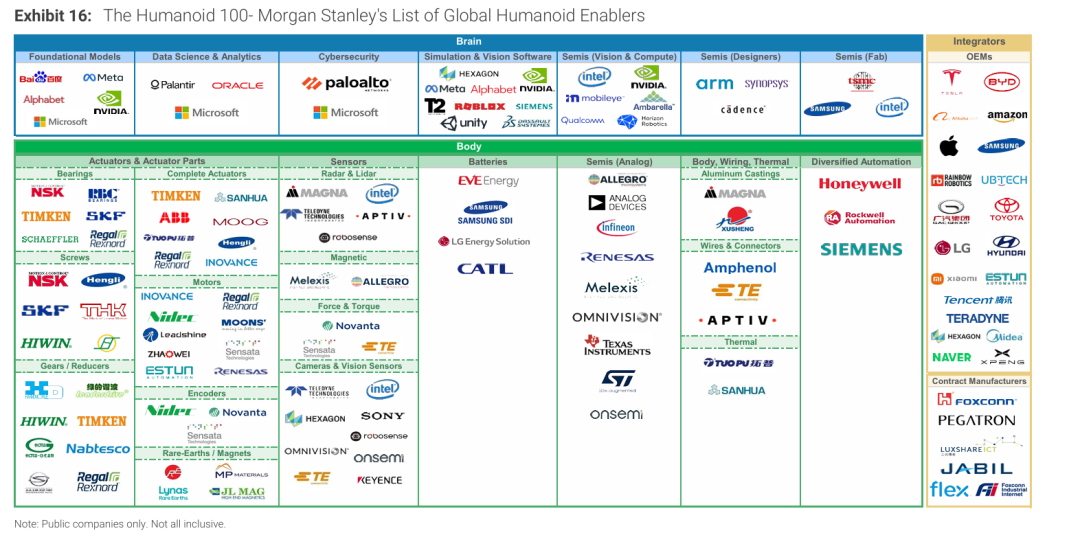

The report, titled Humanoid Horizons: Money Meets Machines, not only updates the list of 100 publicly traded companies in the global humanoid robot industrial chain but also systematically profiles China's key players for the first time.

From the top 100 list, China and the U.S. remain the dominant forces:

- China accounts for 35 companies;

- The U.S. and Canada together account for 39;

- The rest of the Asia-Pacific region accounts for 14 (mainly South Korean and Japanese companies);

- Europe, the Middle East, and Africa account for 12 (primarily European companies).

It should be noted that the list focuses on publicly traded companies, excluding a number of high-growth unlisted stars.

Compared to last year's report, the overall landscape remains stable, with China leading in supply chain and manufacturing capabilities, while the U.S. maintains its edge in AI, software ecosystems, and robot intelligence.

What's new in the latest global top 100 list?

This year's top 100 list reveals the industry's most critical shifts.

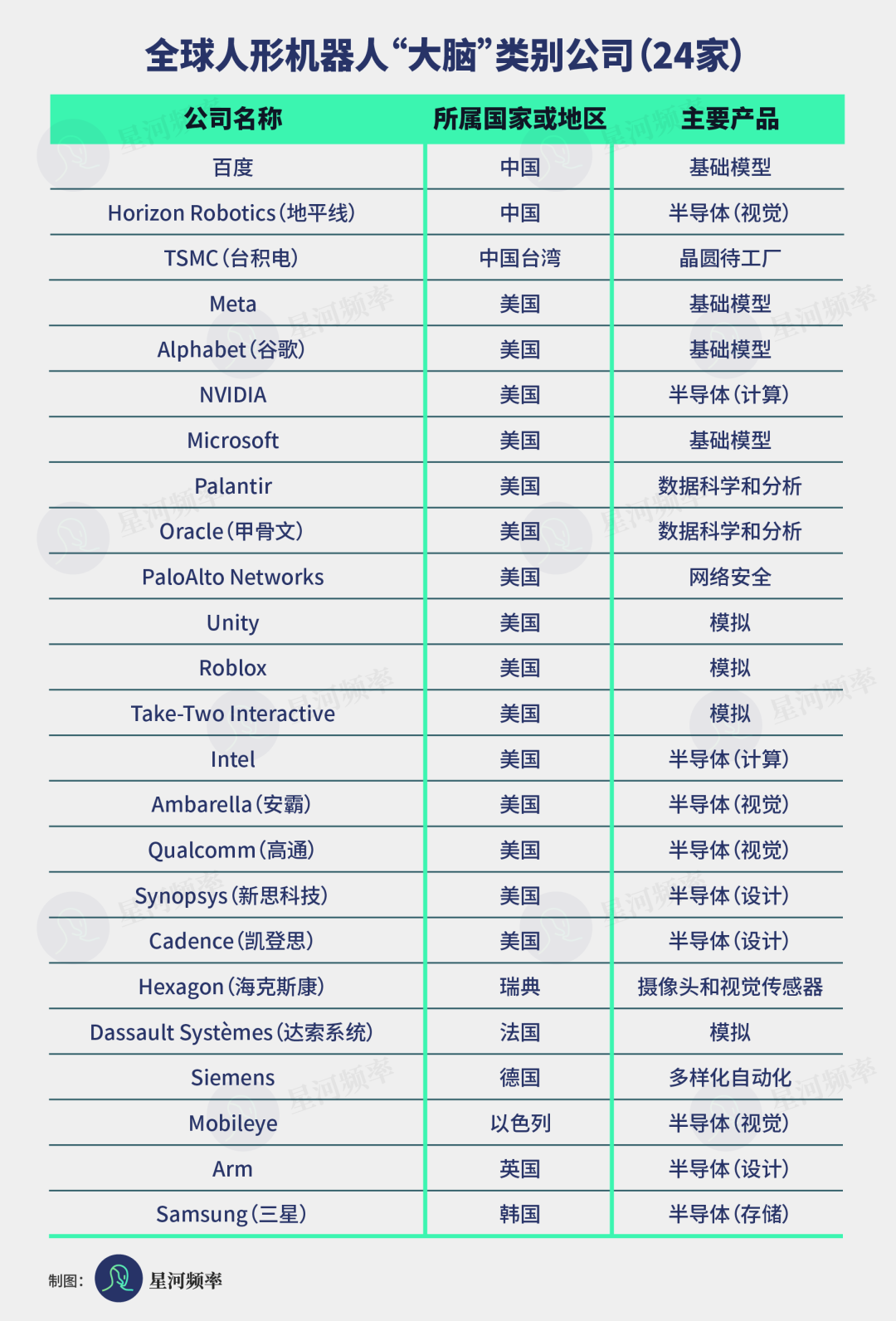

The Brain category includes 24 companies, with the U.S. still holding a dominant position (15 companies), while China maintains three players: Baidu, Horizon Robotics, and TSMC.

Compared to last year, the list now includes gaming companies like Unity, Roblox, and Take-Two Interactive.

At first glance, this seems incongruous—why are gaming companies included in the robot brain category?

The answer lies in the evolving methods of robot data collection and training.

Robot training data has always followed a pyramid structure: internet video data at the base, simulation data in the middle, and real-world data at the top.

Last year, simulation data and real-world teleoperation data were still competing approaches, but this year the industry is leaning toward collecting large volumes of real-world data.

This inevitably means reduced reliance on simulation data in model training, but it doesn't mean simulation training has hit a dead end.

Instead, faced with issues like the lack of real-world complexity in traditional simulations and the gap between simulation and reality, the industry is exploring alternative simulation pathways—and leveraging gaming worlds is a promising approach.

The gaming world is becoming a second training ground for robots.

To understand the world, robots need a 3D or even 4D environment that closely resembles reality, adheres to physical laws, and allows for continuous interaction.

This is precisely what gaming companies excel at. Companies like Roblox and Take-Two have accumulated extensive real-world scene modeling capabilities, essentially possessing the ability to construct digital worlds.

Unlike traditional simulations, gaming environments feature two key characteristics: high fidelity and long-term memory.

Traditional simulations are typically short-term, memoryless physical simulations where each interaction is isolated, and environmental states do not persist across multiple actions.

In gaming worlds, however, every robot action alters the world state and continuously influences subsequent interactions, with these changes being remembered and continuous causal relationships between events.

Here, robot training focuses not just on single-action execution but on long-term decision-making, sustained interaction, and environmental understanding.

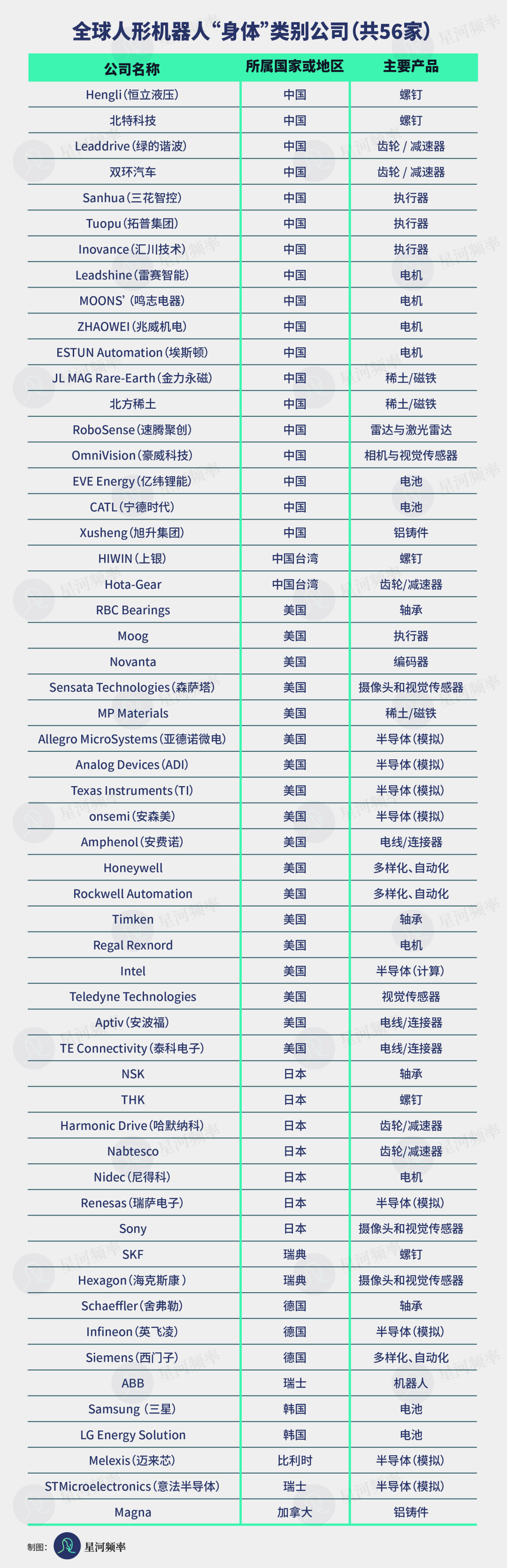

In contrast, the Body category remains relatively stable.

Among the 56 companies, China leads with 20, followed by the U.S. (18), Japan (7), South Korea (3), Europe (8), and Canada (1), with little overall change in the landscape.

China continues to hold the world's most complete supply chain, covering reducers, motors, lead screws, drive controls, and sensors.

A clear trend is the growing presence of companies from the automotive supply chain in core positions. Companies like Sanhua Intelligent Controls, Tuopu Group, Inovance Technology, and Aptiv are essentially leveraging proven industrial capabilities from the automotive industry.

RoboSense is a prime example. As the only Chinese LiDAR company consistently on the list in recent years, it remains an industry leader in LiDAR and visual sensors.

Multiple humanoid robots now use RoboSense's LiDAR, such as the Zhiyuan Lingxi X2 (equipped with E1R LiDAR) and the Zhongqing T800 (equipped with AC1).

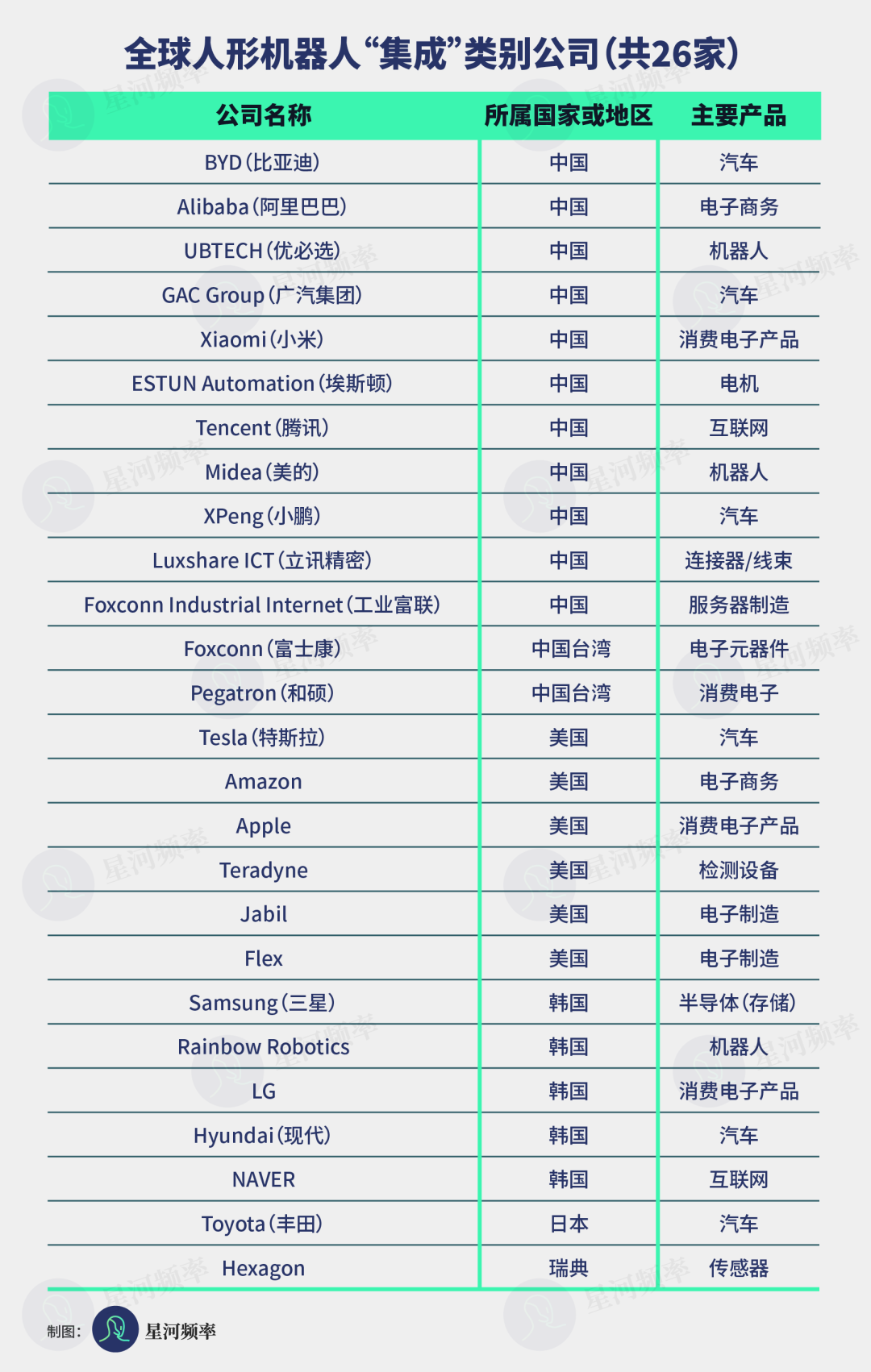

The most significant changes are in the Integrator category. This year, there are 26 companies, with China accounting for 13, the U.S. for 6, South Korea for 5, and Japan and Sweden for 1 each.

Morgan Stanley made an important adjustment by including contract manufacturers as a new subcategory within integrators. Luxshare Precision, Foxconn Industrial Internet, Pegatron, and U.S.-based Jabil and Flex are new additions to this category.

These companies are mostly contract manufacturing giants in consumer electronics and precision manufacturing, possessing one of the robotics industry's most scarce capabilities: scalable delivery.

In the mass production phase of humanoid robots, the ability to manufacture stably, cost-effectively, and at scale has become a new competitive threshold.

These companies' long-established precision manufacturing systems, quality control processes, cost optimization experience, and complex supply chain coordination capabilities give them a natural advantage in large-scale production.

Overall, the industry's competition now hinges on three key factors: more accurate data understanding, more stable hardware systems, and more reliable large-scale manufacturing and delivery capabilities.

While technological breakthroughs remain important, the industry's trajectory is no longer driven by isolated innovations but by a comprehensive set of capabilities spanning data, models, hardware, and manufacturing.

China's Top 66 Humanoid Robot Industrial Chain Players: A Well-Rounded Force

In addition to the global top 100, Morgan Stanley this year also released a dedicated map of China's humanoid robot value chain, including 66 core companies.

This not only provides the global capital market with its first clear view of China's embodied AI capabilities but also reveals a deeper signal: China's industrial chain collaboration speed is upgrading its advantage from traditional low-cost manufacturing to efficient, agile industrial organization.

Behind the map lies the rapid matching of components, complete machines, and system integration with production capacity—a level of organizational efficiency that is China's true moat in the humanoid robot race.

In Morgan Stanley's view, China has built the world's most complete, cost-effective, and fastest-deploying industrial closed loop.

These 66 companies are divided into 12 segments, covering integration, brains, core hardware, perception, and energy.

Leveraging local supply chain advantages, China's humanoid robot industry has formed a unique landscape: complete machine scale-up, hardware foundation-building, brain race leadership, and data positioning.

Morgan Stanley explicitly states that the technology stack for robot brains is still evolving, with world models and VLA models as key exploration directions, but none are yet sufficient for high-precision industrial scenarios.

This means whoever solves the brain problem first will control pricing power across the industrial chain.

Among China's 12 brain-focused players are AI, autonomous driving, chip, and embodied AI startups, with startups accounting for 8 of the 12.

This signals two trends: first, startups are evolving rapidly; second, big players have not yet fully entered the field, leaving a window of opportunity.

Of course, robot brains remain the main battleground between China and the U.S., but robot bodies are China's absolute home turf.

Morgan Stanley's report specifically analyzes Unitree Robotics' IPO prospectus, noting its ASP (average selling price) of approximately $25,000 and a gross margin as high as 60%.

Behind this high margin stand 40 core Chinese suppliers.

Companies like Leader Harmonic Drive (reducers), Inovance Technology (motors), and RoboSense (LiDAR) are mostly veterans from the new energy vehicle and 3C electronics supply chains.

Currently, about 70% of a humanoid robot's cost lies in core components. Under equivalent performance, Chinese-made hardware costs at least 50% less than overseas alternatives—a key foundation for large-scale commercialization.

Meanwhile, humanoid robot hardware design has not yet converged. During this chaotic phase of shifting designs and evolving demands, Chinese suppliers' advantages lie in low costs, rapid response, and scalable manufacturing.

Among the 66, 23 integrators and complete machine manufacturers include both tech giants and specialized vertical players. As the closest to the market, they are already deploying in real-world scenarios.

For example, Zhiyuan completed mass production of 10,000 robots this year, UBTECH shipped over 1,000 full-sized humanoid robots, and Star Move Era partnered with SF Express and China Post to deploy humanoid robots in logistics—one of the earliest PMF (Product-Market Fit) achievements in embodied AI.

These complete machine players are no longer just showcasing capabilities but are actually deploying in B2B and B2C scenarios, performing tasks like factory material handling, logistics sorting, and mall guidance.

From brains to bodies, from execution to perception, China's top 66 have built a globally unique full-stack supply chain—the core reason Morgan Stanley remains bullish on China's humanoid robot industry.

Five Industry Trends: From Capital Singularity to Data Flywheel

Reading through the report, the core message is clear: humanoid robots have definitively moved beyond the hype phase, and the commercialization singularity—where capital, technology, and the physical world fully converge—has arrived.

Specifically, the report highlights five industry-wide trends:

1. Capital Leads, Industry Follows: China as the Global Capital Battleground

Before the halfway point of 2026, global VC investment in humanoid robots has already surpassed the total for all of 2025.

Asia, particularly China, accounts for the majority of this surge, contributing roughly 46% of global VC funding this year.

Following the funding frenzy comes a leap in delivery volumes, with economies of scale gradually emerging.

As more humanoid robot makers find their "sweet spot" in pricing—balancing consumer affordability with corporate profitability—B2B clients and some B2C users are placing orders.

The "sweet spot" refers to the price point where a product or service is widely acceptable to consumers while generating reasonable profits for the company.

Morgan Stanley projects a 5-10x surge in industry-wide deliveries in 2026.

For example, UBTECH targets 5,000 industrial humanoid robot deliveries this year, while component makers like Lingxin Qiaoshou plan to deliver 50,000-100,000 units.

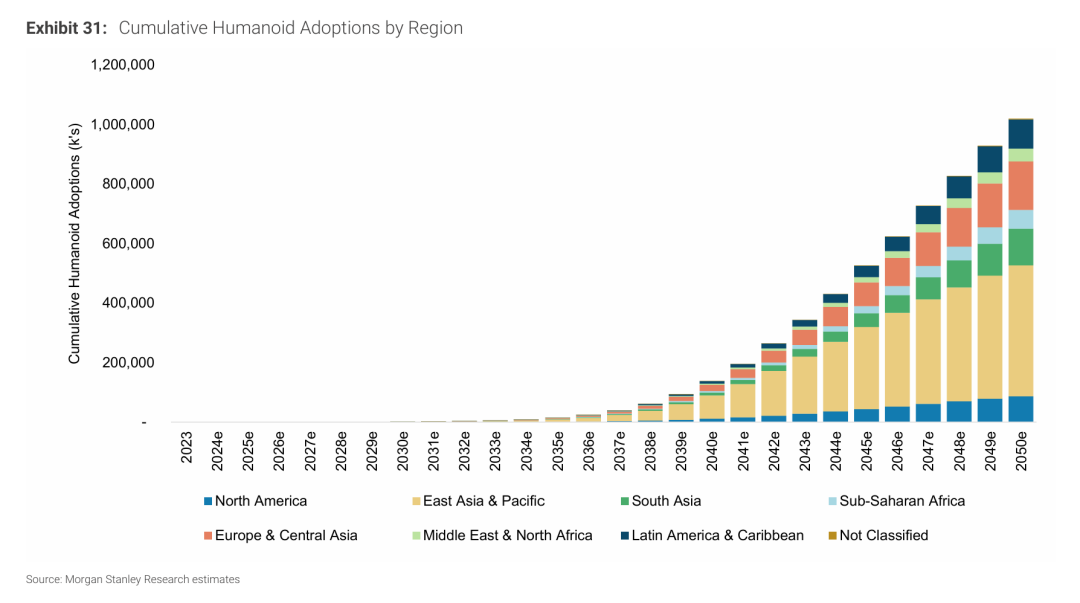

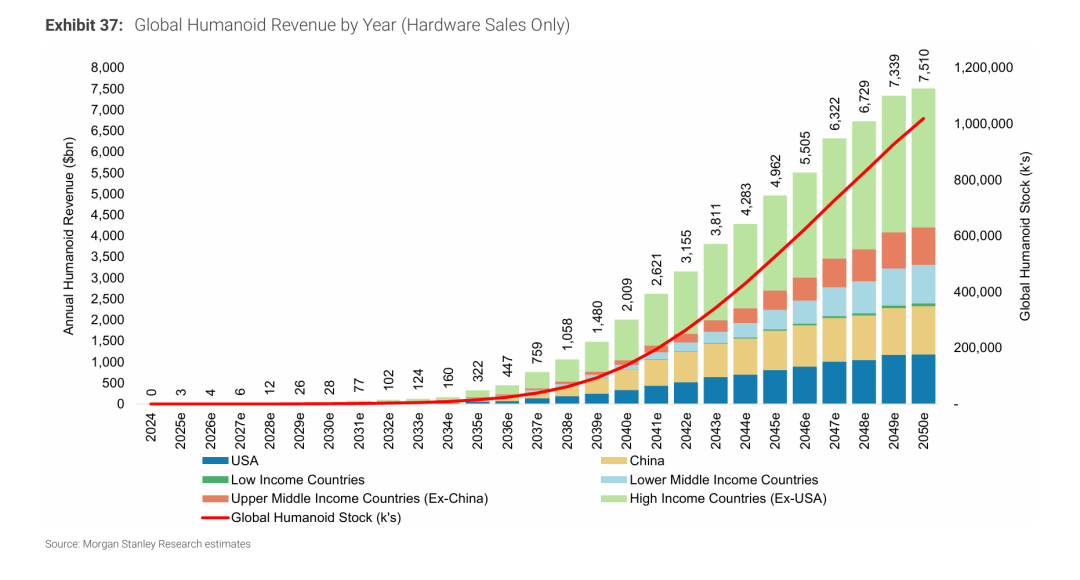

By 2050, China's humanoid robot adoption is expected to reach 302.3 million units, with the global installed base hitting 1 billion robots and annual market revenue reaching $7.5 trillion.

In the technical realm, the focus of competition is shifting. The ultimate barrier in the second half of the humanoid robot race is moving towards the data flywheel.

As algorithmic architectures gradually move towards open-source and hardware designs become modular, the second half of the humanoid robot competition will revolve around high-value physical interaction data in the real world.

Each company has its own take on the algorithmic path, but whoever can first deploy robots into real production lines and acquire real proprietary data flywheels will establish a true technological barrier.

At the same time, the value chain in the industry is set for a major reshuffle, with the complete machine (complete machine), brain (brain), and body (body) not benefiting in sync.

Although complete machine manufacturers have captured the spotlight, in Morgan Stanley's investment valuation model, the order of beneficiaries along the value chain is clear-cut.

In the short term, as the technological stack for robot brains remains uncertain, the iterative risks in complete machine design are extremely high.

Even powerful entities like Tesla Optimus, despite preparing for mass production, have faced setbacks. Musk admitted that the latest Gen 3 tendon-rope hand design revealed shortcomings in actual testing, forcing the team to start over.

This situation underscores that manufacturers of complete machines and companies specializing in brain algorithms are, at present, bearing the brunt of exceptionally high R&D amortization costs and iterative risks.

Conversely, irrespective of fluctuations in upper-layer algorithms and the forms of complete machines, bottom-level precision components—such as harmonic reducers, high-performance sensors, and actuators—exhibit a high degree of certainty and possess universal advantages.

Chinese supply chain companies are leveraging this robust resilience to achieve profitability through large-scale shipments during the challenging phase marked by frequent revisions to complete machines.

Ultimately, the key to commercialization does not lie in the C-end (consumer) home market but rather in B-end (business) productivity scenarios.

Morgan Stanley directly challenges the prevailing expectation that humanoid robots will initially penetrate households. Instead, it posits that true rapid scalability will stem from B-end rigid demand scenarios, including industrial manufacturing, high-precision inspections, warehousing and logistics, and airport ground handling.

These scenarios are replete with repetitive, strenuous, and high-risk tasks, where the value proposition of robot substitution is most evident and the return on investment (ROI) is most readily quantifiable. They represent the most certain opportunities for the industry in the near to medium term.

It can be argued that at this juncture, industry capital is in place, mass production is commencing, and scenarios are beginning to take shape. What truly determines success is no longer concepts and gimmicks but rather the ability to stabilize the supply chain, streamline data, and solidify scenarios.

All of these factors precisely redirect the industry's focus in the next phase towards a more promising long-term landscape.

This year will undoubtedly be the year when embodied intelligence truly demonstrates its value. Technical demonstrations are no longer as compelling; real-world applications carry greater significance.

As robots begin to integrate into the real world, the competition hinges on their capacity to consistently and stably generate value over the long term.

The true barrier has shifted from isolated technological breakthroughs to competition in systemic capabilities, encompassing data, models, hardware, manufacturing, and delivery.

The 66 companies on the list represent not just a ranking but a highly interconnected collaborative network, with China's humanoid robot industry chain showcasing true full-stack capabilities.

The competition in humanoid robots is a marathon—spanning from constructing the physical form and comprehending the world to scaling up and transforming it. With its unique systemic capabilities, China's industry chain is positioned in the leading tier.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry