Changxin Storage Emerges as a Beacon of Hope for Lenovo and Others Amidst Price Hike Challenges

04/10 2026

04/10 2026

432

432

Source | SourceSight

The PC notebook market in 2026 is facing a more severe downturn than anticipated.

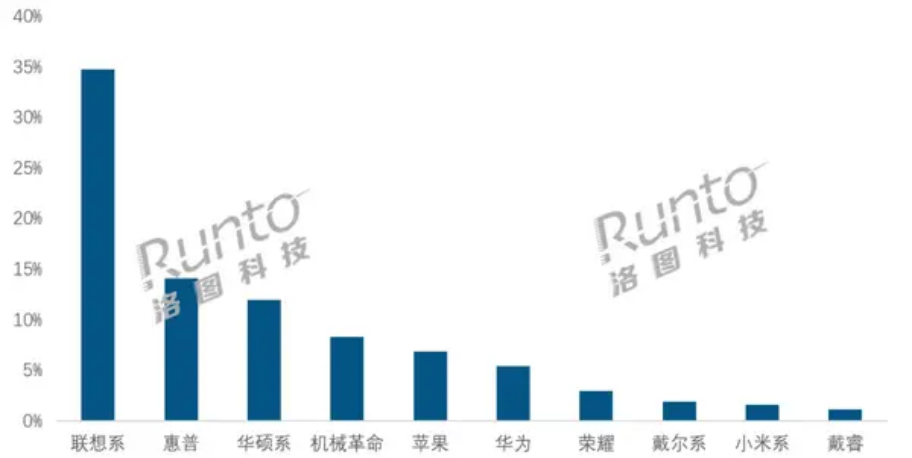

Recent market research data from LuoTu Tech reveals that online notebook sales in China from January to February 2026 plummeted to 947,000 units, a staggering 40.5% year-on-year decrease. Revenues also fell by 40.5%, reaching 5.99 billion yuan. While traditional PC giants like Lenovo, HP, and ASUS maintained robust sales, Huawei and Xiaomi dropped out of the top five.

Source: LuoTu Tech Market Report

Amidst the dual challenges of declining sales volumes and prices, the industry faces yet another setback.

The market downturn is not attributable to a single factor. The high base effect and overextension from the 2025 national subsidy policy, coupled with weaker subsidies at the start of this year, have created initial pressure. Additionally, persistent upstream memory chip prices have forced terminal selling prices to rise, further dampening consumer demand.

The siphoning effect of AI servers on high-bandwidth memory (HBM) and high-performance DDR5 memory production capacity has caused global memory and flash memory prices to surge over the past year. Contract prices for both are estimated to have risen by over 80% and 70%, respectively, in the first quarter, exceeding expectations and driving up overall system costs.

As this memory "super cycle" has yet to peak, the sharp decline in industry sales at the beginning of the year may just be the tip of the iceberg. Multiple institutions, including TrendForce and IDC, consistently predict that the global PC market will enter a new contraction phase, with shipment targets revised downward, expecting declines between 5% and 14%.

In response, leading manufacturers are adopting a two-pronged strategy: raising prices to safeguard profits while betting on AI PCs to reshape demand, aiming to forge new growth paths amidst the industry downturn.

01

Imbalanced Cost Structure

The persistent pressure on upstream supply chain prices is wreaking havoc on the cost structure of the consumer electronics industry.

The shift in memory chip production capacity is the primary culprit behind the sluggish notebook market. Over the past year, AI has consumed nearly the entire industry's memory production capacity, with a single AI server requiring 8-10 times more memory than a standard server. As tech giants like Google and OpenAI ramp up purchases of high-performance memory chips, upstream memory companies such as Samsung and SK Hynix have redirected nearly 90% of their wafer production capacity toward high-margin AI server-specific product lines like HBM and high-performance DDR5. This has drastically reduced the supply of consumer-grade DDR4/DDR5 memory. Combined with price hikes driven by channel partners' collective hoarding, memory prices have skyrocketed.

Take the commonly available DDR5 16GB memory stick as an example: its price soared from around 300 yuan before September 15, 2025, to 1,000 yuan by the end of the same year. Some institutions report that spot prices for memory chips have cumulatively increased by over 300% in 2025.

For notebooks, hard drives and memory account for approximately 15% to 20% of total system costs. Upstream supply and price fluctuations significantly impact manufacturers' profits, a situation that has not improved in 2026. Memory chip prices still rose by over 60% in the first quarter. According to South Korean media, Samsung Electronics recently completed second-quarter DRAM price negotiations with major clients and signed supply contracts, with prices rising about 30% from the first quarter, and further increases are expected for the rest of the year.

Before the pressure from rising memory prices could be absorbed, another cost giant—the CPU—also began to rise.

In March 2026, Intel announced price adjustments for some entry-level and older mobile CPUs, with increases exceeding 15%, further exacerbating overall system cost pressures.

In terms of cost breakdown, CPUs account for about 15% to 30% of a notebook's total bill of materials. Currently, most low-end and mainstream products still primarily use Intel processors. Price hikes have caused tighter supply and unstable allocation for low-end platforms, with small and medium-sized manufacturers generally facing greater cost pressures and shipment risks.

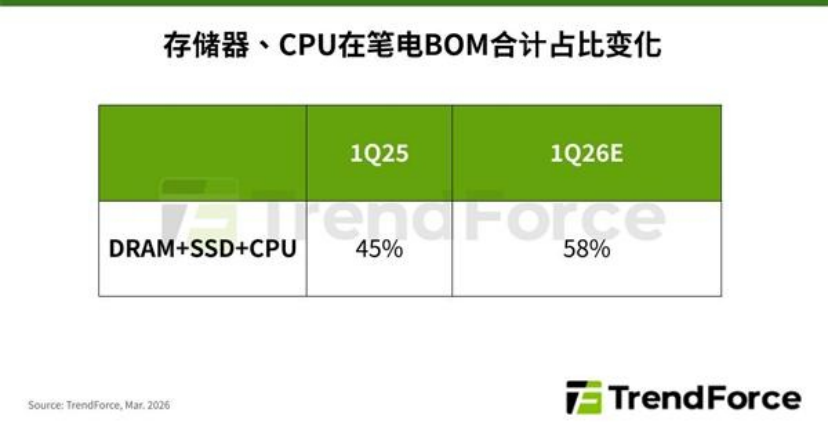

Illustration: TrendForce data indicates that the cost share of DRAM+SSD+CPU will rise to 58% in the first quarter of this year.

The simultaneous price hikes for memory chips and CPUs are merely a snapshot of the deteriorating cost structure in the current industry.

Under the impact of the AI boom, global advanced process and packaging production capacity is being prioritized for high-performance computing products, directly squeezing out production capacity for mainstream and entry-level notebook processors. This structural shift in production capacity not only further drives up procurement costs for core notebook components but also significantly reduces supply chain stability, amplifying uncertainty for major brands in product planning and shipment schedules. This adds even more pressure to an already cost-strained supply side.

TrendForce research reports that, affected by rising memory prices, CPU shortages and price hikes, as well as increased costs for components like PCBs, batteries, and power management ICs, global notebook shipments are expected to decline by 14.8% quarter-on-quarter in the first quarter of this year, far below manufacturers' expectations.

02

Manufacturers Collectively Raise Prices

Under cost pressures, price hikes have become the defining theme of the 2026 notebook market.

According to multiple media reports, a large number of computer manufacturers have begun raising prices one after another since 2026. Lenovo previously issued a price adjustment notice to channel partners, deciding to increase prices for some of its computer products. Prices for some high-end commercial notebooks rose by 20%, with terminal retail price increases for some models exceeding 1,000 yuan. ASUS announced a 15%-25% price hike for all its notebooks; Acer raised prices for some models by 10%-20%; Dell, HP, and other manufacturers are also preparing to follow suit with price increases.

Source: Kechuangban Daily report

Behind these centralized price adjustments lie manufacturers' efforts to pass on cost increase pressures to terminal selling prices in order to maintain their original gross margin structures.

Some institutions suggest that further price increases are likely in the coming quarters. With the long-term expectation of rising terminal prices, consumer purchasing decisions are becoming more conservative, and market wait-and-see sentiment continues to grow. This will further suppress actual shipment momentum, ultimately creating a negative cycle of rising prices and shrinking demand.

In short, an industry-wide shipment downturn is now inevitable.

From a longer-term perspective, the PC market peaked nearly a decade ago. Although demand for remote work and online education during the pandemic temporarily revived the market, subsequent demand overextension combined with global economic adjustments led to a collapse in PC shipments. In 2023, global PC shipments totaled 241.8 million units, down 14.8% from 2022, reaching a near-20-year low. The PC market has now thoroughly returned to competition over existing users in recent years.

Under the impact of the new AI wave, consumer demand recovery has fallen short of expectations. As a result, multiple institutions have further revised downward their shipment targets for this year, building on already low expectations.

TrendForce believes that the global notebook shipment decline this year will be greater than expected. The agency originally forecast a 5.4% year-on-year decrease but has now revised this to a 9.4% drop.

IDC predicts an 11.3% decline in global personal computer shipments this year, a significant downward revision from its November forecast (-2.4%). The agency states that the impact of rising costs will continue until 2027. Although component prices are expected to fall by 2028, they are unlikely to return to pre-2025 levels. The market is expected to enter a "new normal," with structural increases in average selling prices and corresponding long-term slowdowns in demand.

Gartner estimates that by the end of 2026, prices for memory and flash memory chips will rise by 130%, driving PC prices up 17% from last year and smartphone prices up 13%. This will directly cause the largest decline in the personal computer and communications equipment market in nearly a decade, further lengthening device replacement cycles.

Notably, despite significant downward revisions in shipment expectations, rising terminal PC prices have boosted sales revenue, causing the total market value to increase instead of decline. IDC predicts that personal computer revenue will grow by 1.6% to reach $274 billion.

03

Accelerating Transformation to Save Themselves

Beyond price increases as a buffer, seeking domestic alternatives and developing native AI PCs have become new long-term strategic goals for major manufacturers.

Earlier this year, industry sources reported that HP, Dell, Acer, and other PC manufacturers are in talks with Changxin Storage, planning to certify its DDR5 memory modules to address global memory supply shortages and price hikes.

According to Changxin Storage's prospectus, its current direct customers are primarily well-known distributors in the semiconductor industry, while its end customers are concentrated among large manufacturers in downstream applications such as servers, mobile devices, and personal computers, mainly domestic Chinese companies, including leading consumer electronics firms like Lenovo, Honor, and Xiaomi.

From a product perspective, Changxin Storage released its new generation of high-speed DDR5 products at the end of last year, which already meet the performance levels of mainstream high-end PCs. Currently, its overall production capacity and yield rates are still ramping up.

The process of domestic substitution is further accelerating, and another growth engine for manufacturers is the native AI PC market.

In October last year, Microsoft further integrated native AI capabilities into Windows 11 by updating Copilot and the Agentic platform, while defining hardware requirements for the new generation of Windows AI PCs through the Copilot+ PC standard. With AI PCs, users will be able to directly schedule various AI functions locally.

Source: Microsoft Store

IDC predicts that native AI PCs will become the main driver of shipment growth in the domestic market this year, with AI PC penetration in China expected to exceed 52% by the end of the year.

To this end, mainstream manufacturers like ASUS, Acer, and Mechanical Revolution have accelerated their "premium + AI PC" dual-wheel drive strategy, attempting to offset the negative impact of price increases through product premiums.

Facing the AI wave, Lenovo has taken an even more aggressive approach. On April 1, Yang Yuanqing officially announced at the fiscal year pledge meeting that the company is fully launching its strategic transformation into an AI-native enterprise, making clear that AI is not an add-on project but a core gene. Subsequently, the company will design and reconstruct everything from product end, solutions, to business processes with AI at its core from the source, and is officially sprinting toward the goal of "achieving $100 billion in revenue within two years."

In addition, cross-border PC brands like Huawei and Xiaomi are leveraging their system ecosystem advantages to accelerate seamless collaboration between PCs and devices like smartphones and tablets, seeking breakthroughs through a full-scenario smart experience.

The era of native AI PCs has opened a new battlefield, with different manufacturers further diversifying their strategies. However, whether this new growth engine can continuously stimulate market demand hinges on whether it can provide unique value beyond traditional PCs. For consumers, 2026 may not be the best time to upgrade devices, but it will be an important year to witness transformation in the PC industry.

Some images sourced from the internet. Please notify us for removal if there is any infringement.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models