Memory Prices Skyrocket, Becoming ‘Digital Black Gold’ as Shenzhen’s Huaqiangbei Spawns a Wave of Billionaires

07/10 2026

07/10 2026

530

530

Source | Yuan Media

Memory prices, which had previously been in decline, have recently seen a dramatic rebound.

After surging since the end of 2025, memory prices began to plateau in March 2026, entering a phase of extreme volatility. However, Apple’s late-June announcement of global price hikes for its iPhone, MacBook, and iPad products caused the declining memory prices to reverse course and surge once again.

Previously, a group of merchants in Shenzhen’s Huaqiangbei had aggressively stockpiled memory, and now they finally have an opportunity to cash in. Yet, the real winners are the memory manufacturers and distributors.

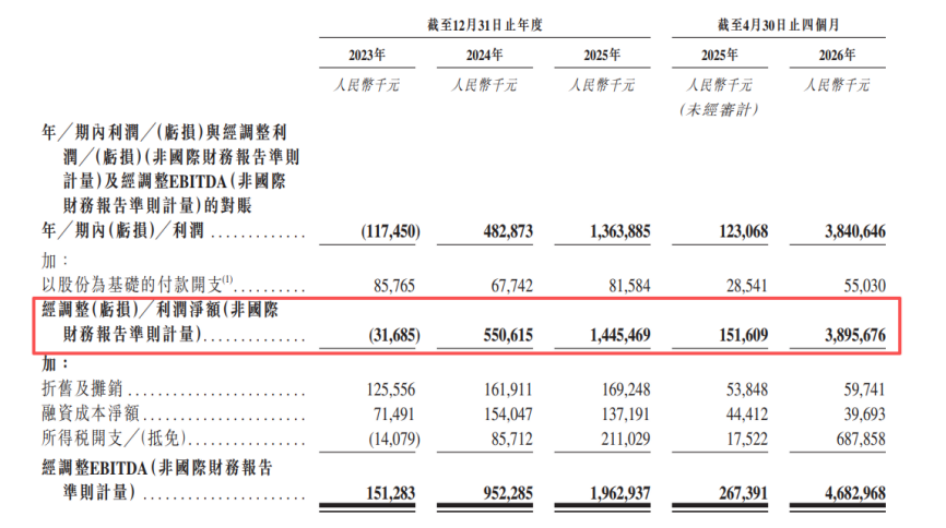

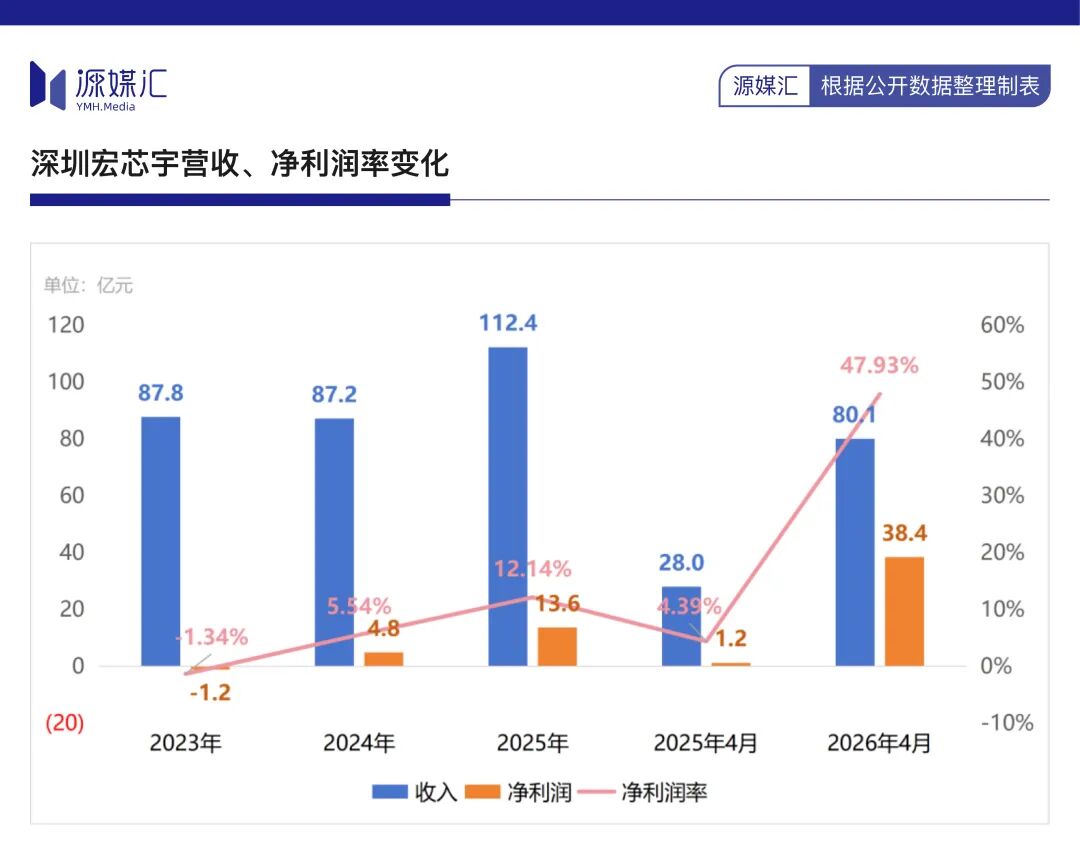

Recently, independent storage manufacturer Shenzhen Hongxinyu made its second attempt to list on the Hong Kong Stock Exchange. Its disclosed prospectus contains a string of impressive figures: a net profit of 3.84 billion yuan in the first four months of 2026, marking a year-on-year increase of 3020.8%. In just four months, the company earned nearly 2.22 times the profit it made in the previous three years.

Screenshot from Hongxinyu's prospectus

Hongxinyu claims in its prospectus that, based on 2025 revenue, it is the fifth-largest global and second-largest Chinese independent memory manufacturer. Its consumer-grade enterprise clients include Xiaomi, Transsion, OPPO, Vivo, TCL, and XiaoDu.

Not just Hongxinyu, but companies like Biwin Storage, Demingli, Jingcun Technology, and Jiangbo Long have also seen their performance soar amid the storage chip and memory price surge.

Shenzhen’s Huaqiangbei is producing billionaires in bulk.

01. Memory Modules Soar to ‘Digital Black Gold’

Throughout 2025, gold rose by 44%, silver by over 120%, and LME copper futures by approximately 29.2%. Entering 2026, the precious metals market shifted from a risk-averse frenzy to market demand, with prices falling sharply.

Wind data shows that since 2026, gold prices have fallen by 28.9%, silver by 51.7%, and copper has risen by 2.6%.

But memory modules are an exception—they began rising in the second half of 2025 and continued to surge in 2026, effectively becoming ‘digital black gold.’

At the beginning of 2025, the price of DDR4 16GB was $2, and DDR5 16GB was $4, with year-end increases of 1800% and 500%, respectively. In the first and second quarters of 2026, DDR4 16GB prices rose by over 90% and 45%, while DDR5 16GB prices increased by over 55% and 50%.

In the plans of the three major storage giants—Samsung, SK Hynix, and Micron—DDR4 products have entered the phase-out stage, with production scheduled to cease gradually in June 2025, shifting to DDR5 and HBM products. Simply put, the giants are chasing higher profits.

DDR5 outperforms DDR4 in terms of performance, capacity, and energy efficiency, better meeting the high-load demands of current AI training and 4K video editing. However, the downstream market's demand for DDR5's performance is not that strong, with many server manufacturers preferring the more cost-effective DDR4.

This has led to a severe market mismatch.

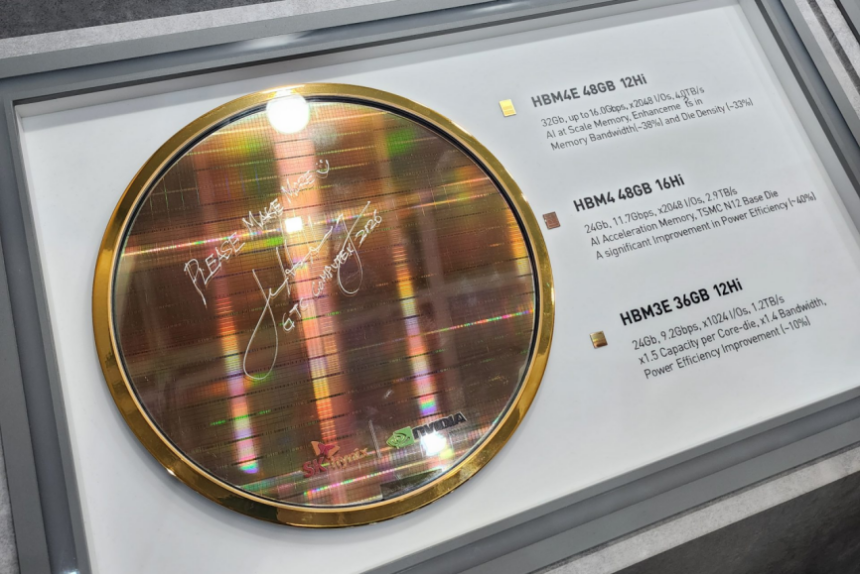

On one side, the explosion in demand for AI large models and inference computing power, along with large-scale expansions of global data center servers, has prompted storage giants to shift production to DDR5 and HBM. SK Hynix and Micron's HBM production capacity for 2026 has already been fully booked.

Even Jensen Huang had to plead with SK Hynix, saying, ‘Please Make More.’

The actions of the three major storage giants have led to a lawsuit by U.S. consumers, who accuse them of intentionally restricting supply since 2022 and manipulating prices, resulting in a 700% increase in DRAM storage chip prices over the past four years.

On the other side, cost-conscious general-purpose server manufacturers and the mainstream consumer market have begun to revert to DDR4 products. Combined with production capacity being locked in by long-term agreements, DDR4 inventory has become even tighter, leading to a price inversion with DDR5.

A group of merchants in Shenzhen’s Huaqiangbei have treated memory modules as financial products, hoarding them on a large scale.

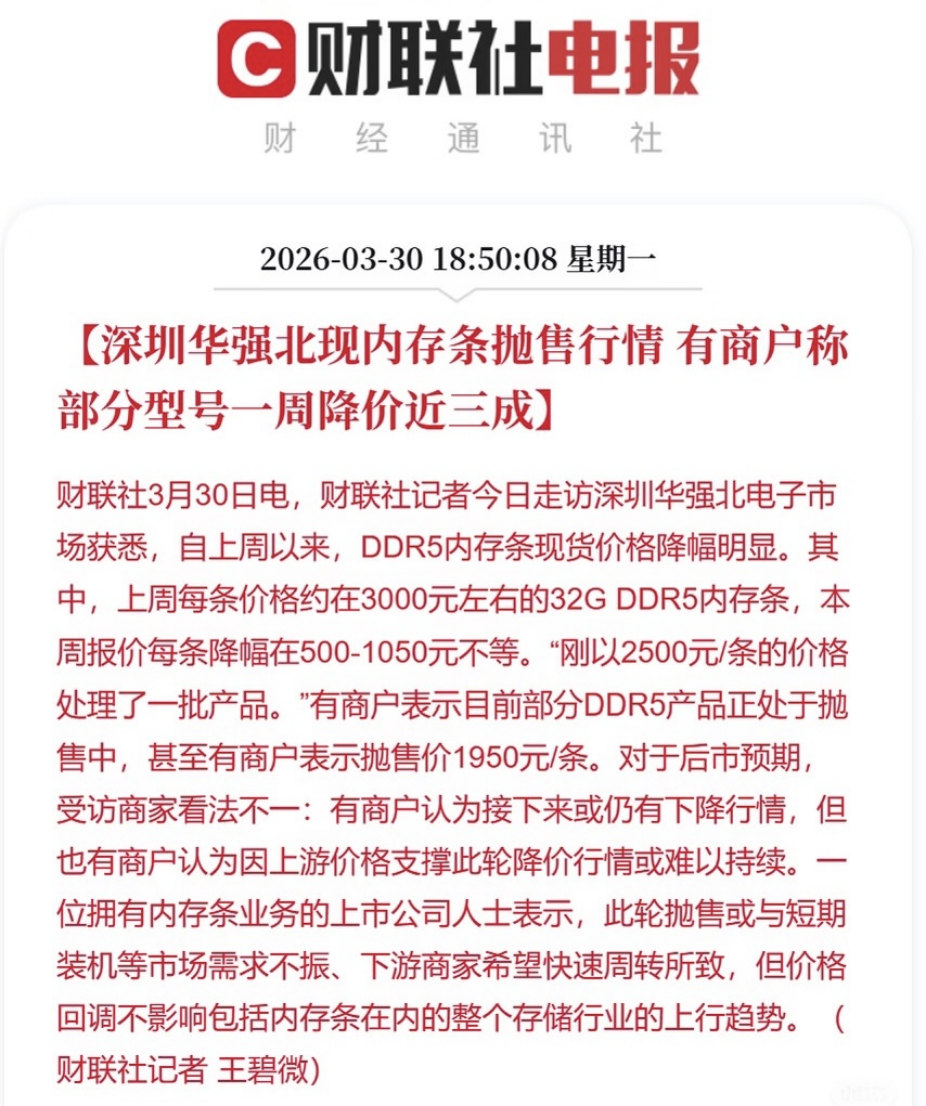

However, in March 2026, memory prices began to stagnate and entered a period of extreme volatility, fluctuating wildly like a rollercoaster, with prices changing daily.

Screenshot from related reports

Many merchants who hoarded memory didn't fully understand the situation. When the trend reached retail customers, they weren't sure whether they were reaping the benefits or catching a falling knife.

In reality, throughout the memory price surge, it was mainly enterprise-grade server memory that was rising, with consumer-grade memory accounting for only 1%-5% of manufacturers' shares, experiencing a passive price increase.

Many ‘wait-and-see’ consumers are waiting for the ‘AI bubble to burst’—hoping prices will fall before upgrading their computer configurations. Many Huaqiangbei bosses have found that while unit prices have gone up, sales volumes have declined, leaving overall profits almost unchanged.

02. A New Generation of Billionaires

In this memory price surge, the real money-makers are the domestic memory alternative manufacturers and distributors in the supply chain.

Recently, storage module manufacturers have one after another disclosed their 2026 first-half performance forecasts, with figures that are staggering.

Among them, Changxin Storage, in the first tier, expects first-half revenue of 110-120 billion yuan, a year-on-year increase of approximately 613%-677%. Net profit is expected to be 50-57 billion yuan, a year-on-year increase of 2244%-2544%.

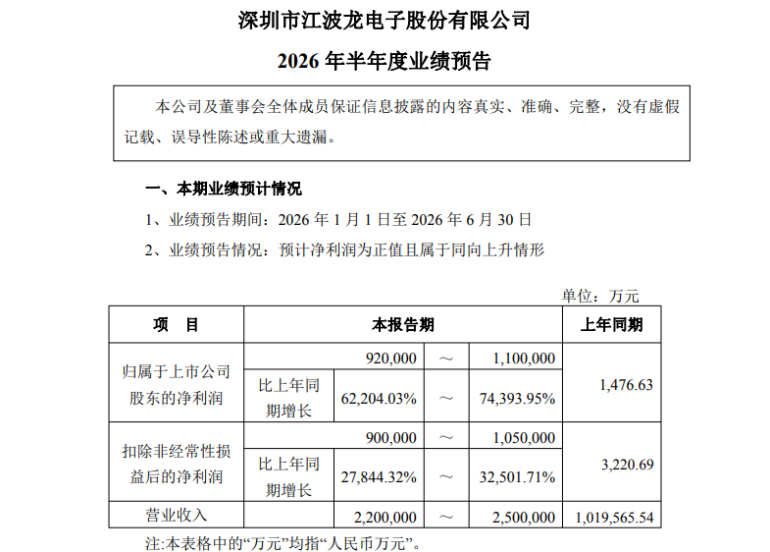

Jiangbo Long, in the second tier, expects revenue of 22-25 billion yuan, a year-on-year increase of 115.78%-145.2%. Net profit is expected to be 9.2-11 billion yuan, an astonishing increase of 622.9-744.8 times.

Image from Jiangbo Long's announcement

Jiangbo Long's ‘fellow Huaqiangbei resident’ Biwin Storage, while not disclosing a performance forecast, has secured a $1.5 billion long-term procurement order extending to June 2028. In the first quarter of 2026, its AI emerging edge storage product revenue was approximately 1.175 billion yuan, a year-on-year increase of 496.45%. Net profit surged from a loss of 200 million yuan in the same period last year to approximately 2.9 billion yuan.

Even the storage chip ‘middleman’ Demingli has made a fortune. In the first quarter of 2026, the company's revenue surged by 502% year-on-year to 7.54 billion yuan. Net profit was 3.346 billion yuan, an increase of 4943.4%.

From the 2026 first-quarter reports, it is evident that during the storage chip price surge, these companies were consistently hoarding inventory. Jiangbo Long's inventory balance increased by 53.8% year-on-year to 17.96 billion yuan. Biwin Storage's inventory balance was 12.07 billion yuan, and Demingli's was 12.19 billion yuan, up 53.4% and 72.7%, respectively.

Smart money in the capital markets knows how to choose.

On July 7, Jiangbo Long's closing price was 627.9 yuan, Biwin Storage's was 425 yuan, and Demingli's was 851 yuan. Compared to their closing prices on June 30, 2026, their stock prices have increased six to sevenfold.

In just one year, the storage chip industry has seen the emergence of trillion-yuan-level listed companies. Jiangbo Long's market value soared from 36 billion yuan to 260 billion yuan, Biwin Storage's from 31 billion yuan to 200 billion yuan, and Demingli's from 19 billion yuan to 193 billion yuan.

Additionally, GigaDevice's market value once reached 550 billion yuan, and Montage Technology's surpassed 340 billion yuan.

This has also spawned a group of billionaires and multi-billionaires.

That year, among the ‘Three Tigers of Storage’ in Shenzhen’s Huaqiangbei, Jiangbo Long's controlling shareholder Cai Huabo saw his net worth surge by 118.7 billion yuan, Biwin Storage's controlling shareholder Sun Chengsi's by 29.92 billion yuan, and Demingli's controlling shareholder Li Hu's by 22.17 billion yuan.

GigaDevice's controlling shareholder Zhu Yiming also saw his holding value increase fourfold.

Many major shareholders also understand the principle of ‘taking profits.’ Wind data shows that in the first half of 2026, among the top 20 A-share major shareholders reducing their stakes, storage companies like GigaDevice, Biwin Storage, Junzheng, and Jiangbo Long were all on the list, with reduction intervals ranging from 2.775 billion to 4.473 billion yuan.

Screenshot from Wind

However, the current hype around storage chips has begun to fade. Shenzhen Hongxinyu, which is making a second attempt to enter the capital markets, seems to be arriving late.

03. ‘Middlemen’ Can Also Make a Fortune

The ‘Three Tigers of Storage’ in Shenzhen’s Huaqiangbei—Jiangbo Long, Biwin Storage, and Demingli—entered the storage field around 2000. Shenzhen Hongxinyu's founder Wu Yisheng, while long involved in electronic components and chip sales in Shenzhen, only founded the company in 2018.

At the time, Wu Yisheng partnered with Phison Electronics, a long-term collaborating Taiwanese controller chip manufacturer, to establish Hongxinyu, primarily engaging in the distribution and simple module packaging of DRAM and NAND storage chips.

Simply put, Hongxinyu is a ‘middleman’ in the storage chip industry, without a wafer fab or chip design operations.

Screenshot from Hongxinyu's prospectus

In the storage chip circle, technology reigns supreme—no technology means no bargaining power.

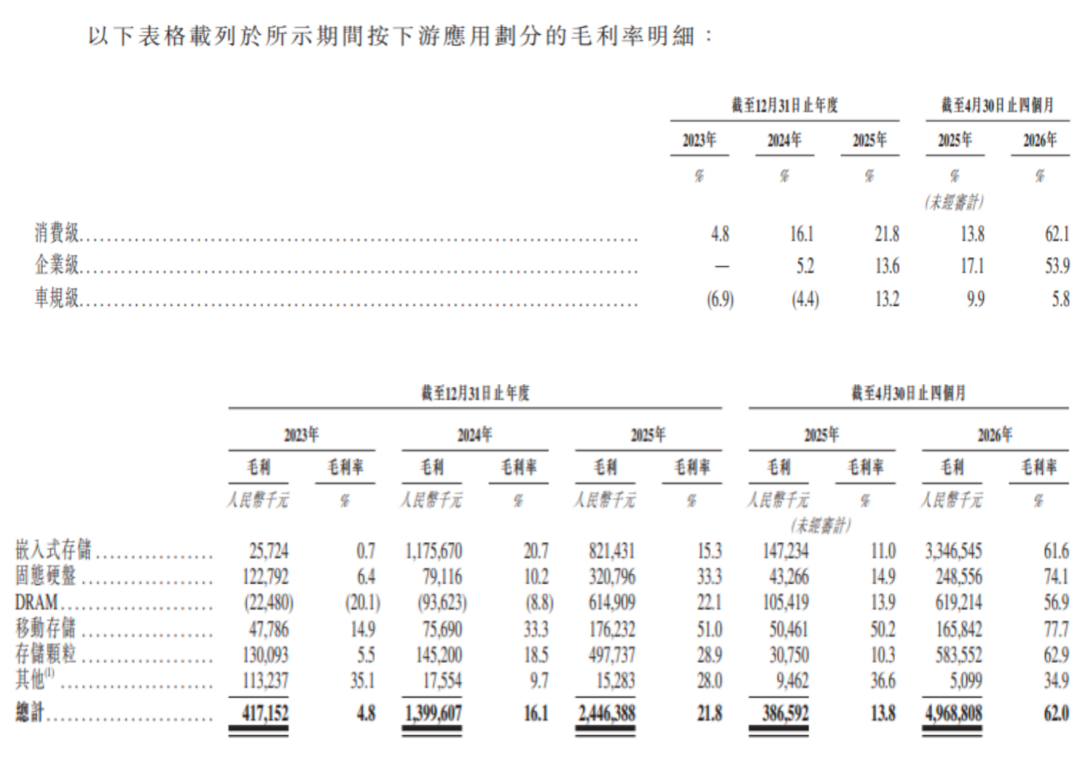

Therefore, before the AI large models drove up storage chip prices, Hongxinyu was engaged in a low-margin business. In 2023, its consumer-grade product gross margin was only 4.8%, and its automotive-grade was -6.9%. After 2024, the gross margins for consumer-grade, enterprise-grade, and automotive-grade products gradually increased.

Screenshot from Hongxinyu's prospectus

Many domestic storage chip listed companies have achieved a turnaround from losses to profits thanks to this storage chip boom.

Hongxinyu is one of them—it turned a net profit loss into a gain in 2024, earned 1.36 billion yuan in 2025, and made 3.84 billion yuan in just four months of 2026.

However, over the past three years, while Hongxinyu's revenue and net profit have been rising, its operating cash flow has not kept pace. From 2023 to April 2026, its net operating cash flow was -1.05 billion yuan, -1.12 billion yuan, 720 million yuan, and -2.69 billion yuan, respectively.

This data generally indicates that while products are being sold, the money hasn't been collected yet. However, the specific nature of the situation must also be considered—this is a company in the storage chip field.

Hongxinyu is actually hoarding inventory aggressively. From 2024 to April 2026, the company's total inventory and prepayments were 4.35 billion yuan, 8 billion yuan, and 14.84 billion yuan, respectively, a 3.4-fold increase over the interval.

Hongxinyu has also taken out significant bank loans, betting big on storage chips. In April 2026, its bank loan amount alone accounted for 58% of its total liabilities.

Based on April's net profit, Hongxinyu's bet paid off.

But Hongxinyu's other major gamble has yet to succeed.

As of now, Hongxinyu has completed six rounds of financing, raising approximately 1.666 billion yuan. In March 2025, it completed its Series D financing, with a post-money valuation of 10.76 billion yuan.

During the financing process, Hongxinyu's controlling shareholder Wu Yisheng signed listing agreements with over 10 investment institutions, including Shenzhen High-Tech Investment, Juyuan Xinchuang, Hefei Industrial Investment, Hefei Guoyao, Rongchuang Lingyue, and Guangzhou Zhiwei. If the listing attempt fails or is terminated, the agreements will be reinstated.

Compared to the merchants in Shenzhen’s Huaqiangbei who take out mortgages or sell property to hoard memory modules, Hongxinyu's gamble is essentially no different, just on a larger scale.

Note: The article's material is sourced from official reports and

-

![]()

Li Bin Claims, 'Denying the Pure EV Trend is Like Ostrichism.' What's Li Xiang's Take?

-

Lenovo: Liu Jun Turns Left, Yang Yuanqing Turns Right

-

Lenovo: Liu Jun Goes Left, Yang Yuanqing Goes Right

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech