Can Bezos and Chinese Enterprises Keep Pace with SpaceX's Rivals?

04/09 2026

04/09 2026

612

612

In our previous report, we primarily explored the core themes of the current wave of commercial spaceflight opportunities, focusing on the potential Initial Public Offering (IPO) of SpaceX. In this installment, we shift our attention to the key players in the reusable rocket launch and satellite operation sectors, delving into the industrial chain links to uncover potential investment opportunities from the perspectives of the competitive landscape and industrial chain segments.

Body:

I. Competitive Landscape of Reusable Rockets

We have reviewed the main participants in the reusable rocket sector, with the aim of answering two primary questions: First, what is the competitive landscape of the industry? Second, by comparing the different technical routes and models adopted by various participants, we analyze the main competitive elements of the industry and the industrial chain links they may involve.

(I) Bezos's Strategic Layout

In the realm of reusable rockets, SpaceX's most formidable competitor is Amazon founder Bezos.

Bezos's Blue Origin, established earlier than SpaceX, shares a similar technical vision of reducing the cost of space access. It has now partially mastered rocket reusability technology. The New Glenn rocket successfully completed its maiden flight and first-stage recovery in 2025 and is set to commence commercial missions in April 2026.

Here, we draw a comparison between the two:

1. Philosophical Differences

SpaceX envisions enabling humanity to become a multi-planetary species, exemplified by its ambition to colonize Mars. In contrast, Blue Origin aims to alleviate Earth's burden by relocating heavy industry to space, thereby creating a more habitable environment on Earth. Despite their differing narratives, the essence of both visions is rooted in the fragility of Earth and the finiteness of its resources. These are, undoubtedly, monumental undertakings that do not promise short-term profits.

Therefore, although Bezos has been selling $1 billion worth of Amazon stock annually to provide Blue Origin with patient capital, the company still needs to explore sustainable and profitable business models. This necessity has led Blue Origin to undertake government and military projects, commercial ventures, and the development of its own 'Starlink' equivalent (Project Kuiper, etc.). Consequently, direct competition between Blue Origin and SpaceX across all fronts is inevitable.

2. Model Differences

Despite having similar business objectives and layouts, SpaceX and Blue Origin differ significantly in their operational approaches. SpaceX adheres to a typical 'fast trial and error' and 'agile development' model, while Blue Origin adopts a more traditional, long-termist, and gradual approach. Despite its slower pace, Blue Origin has also made commendable progress:

The New Glenn rocket successfully achieved first-stage booster recovery in 2025, becoming the world's second orbit-class rocket to achieve vertical recovery and direct landing on an unmanned sea barge. The New Glenn rocket's low-Earth orbit payload capacity reaches 45 tons, significantly higher than that of Falcon 9 and close to that of Falcon Heavy.

Figure: New Glenn achieves first-stage in-air reignition and recovery

Source: Blue Origin, Dolphin Research

3. Technical Route Differences Based on Philosophy and Models

(1) Engine Technology: Directly Determines Rocket Recoverability and Low-Cost Reusability

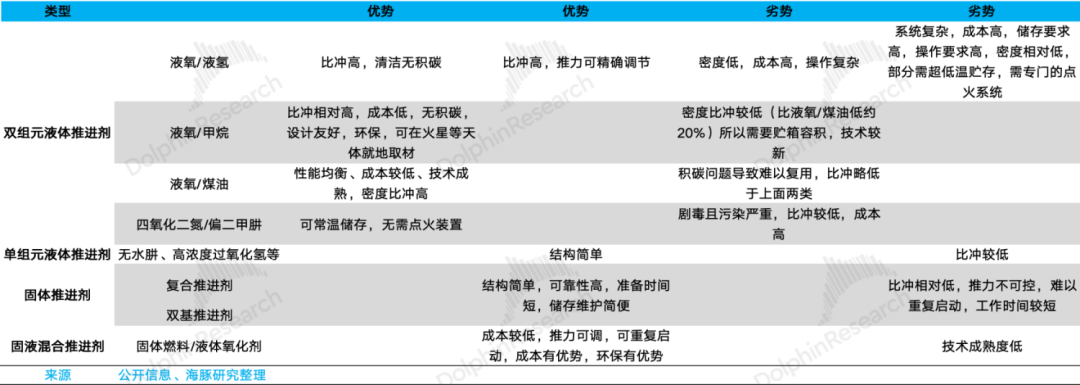

1) Fuel

Fuel, or propellant, currently predominantly employs bipropellant liquid propulsion, meaning the fuel is liquid and divided into two parts: one serving as the combustant and the other as the oxidizer (since space lacks oxygen, an oxidizer is necessary).

Blue Origin's conservative R&D approach is reflected in its fuel choice. SpaceX utilizes liquid oxygen/kerosene in its Falcon series and liquid oxygen/methane in its Starship series. Liquid oxygen/kerosene is technically mature, relatively reliable, and cost-effective. Liquid oxygen/methane, on the other hand, does not produce carbon deposits (which can clog pipelines), offers higher reusability efficiency, and can theoretically utilize in-situ resources on Mars, making it more suitable for deep-space exploration, although the technology is still in its infancy. Blue Origin directly adopts liquid oxygen/methane, the same as Starship.

2) Cycle Method

Blue Origin employs an oxygen-rich staged combustion cycle, while SpaceX's Merlin engine (used in Falcon) utilizes a gas-generator cycle, and its Raptor engine (used in Starship) adopts a full-flow staged combustion cycle.

The engine cycle method refers to the entire workflow of delivering propellant to the combustion chamber for thrust generation, with different methods primarily differing in how they drive the turbopump. The turbopump pumps propellant into the combustion chamber and is equivalent to the rocket's heart.

Without delving into specific principles, Blue Origin's oxygen-rich staged combustion cycle offers high efficiency and no carbon deposit issues, with a certain level of maturity in design and manufacturing, representing a balanced solution.

The Merlin's gas-generator cycle is simple in structure and cost-effective, with relatively mature technology, although it offers lower efficiency and is less conducive to reuse. The full-flow staged combustion cycle offers ideal efficiency, safety, and service life but is extremely challenging to design and manufacture. This also reflects the model differences between the two companies.

3) Application of 3D Printing Technology

Rocket engines have complex structures, with rapidly evolving technology and relatively low production volumes, making 3D printing technology well-suited to these demands. However, the technology is still in its infancy, with many limitations in reliability and performance.

SpaceX aggressively applies 3D printing technology, especially extensively in its Raptor engines. Blue Origin currently focuses on using 3D printing for certain key components in its engines.

In summary, Blue Origin initially aimed for advanced yet conservative solutions, investing more time and upfront R&D costs but achieving phased success, which indeed poses competitive pressure on SpaceX.

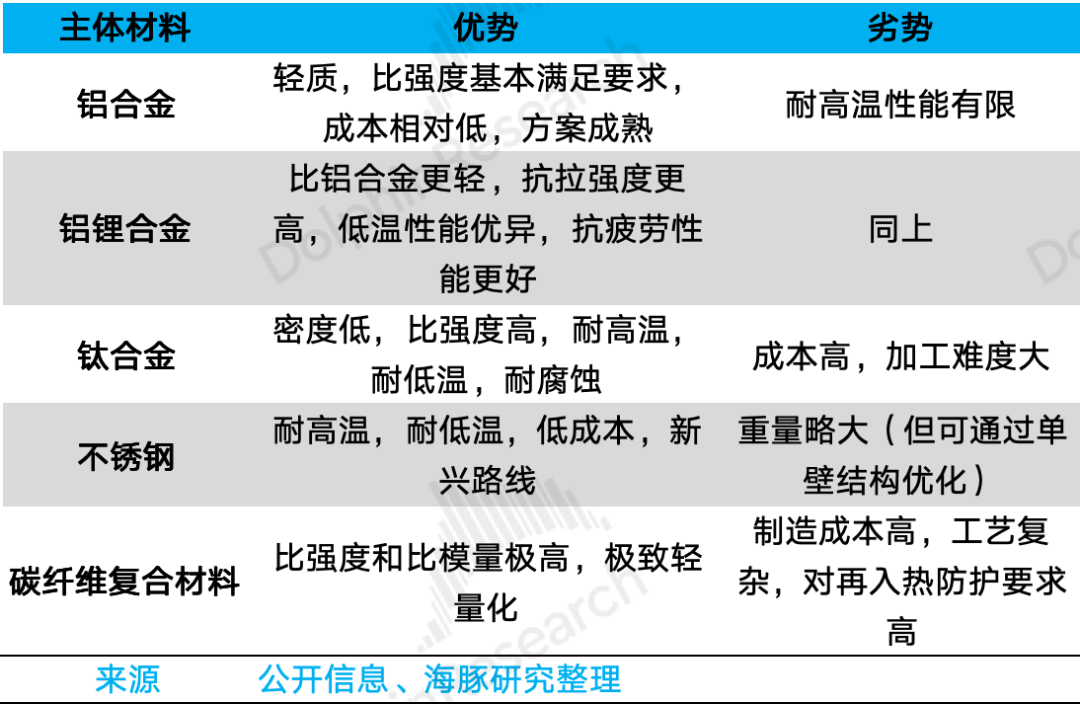

(2) The rocket body ranks second in cost within a rocket, with material selection being a key consideration.

Excluding R&D and ground facility amortization, engine costs account for the highest proportion of rocket costs, reaching 40-50%, followed by the rocket body at around 25%, then the GNC system at about 15%, with fuel accounting for less than 3%.

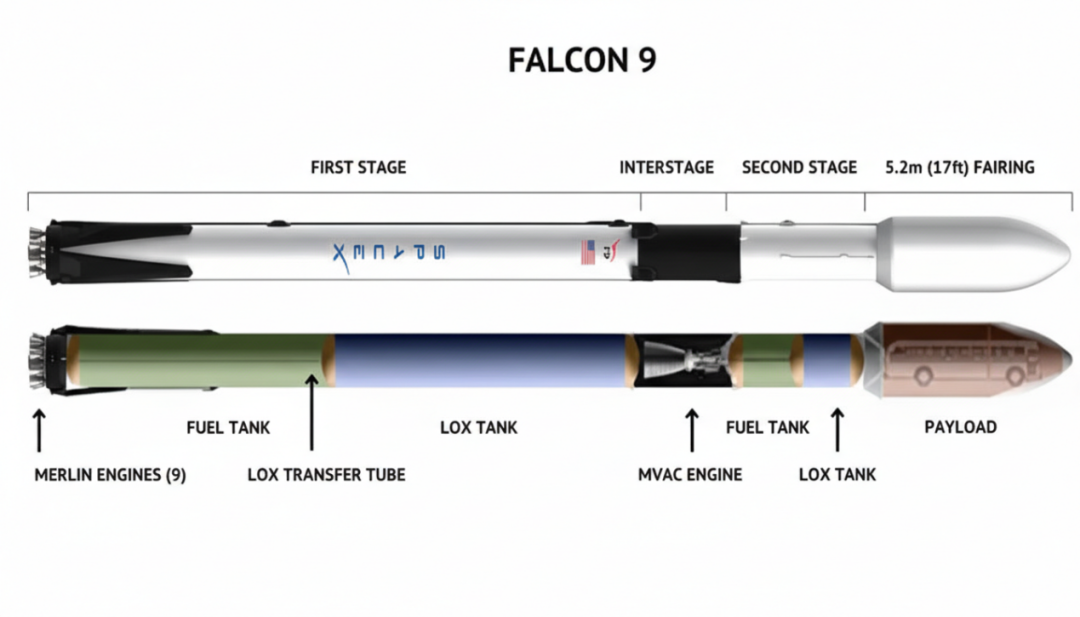

Figure: Falcon 9 Rocket Structure

Source: Orbital Today, Dolphin Research

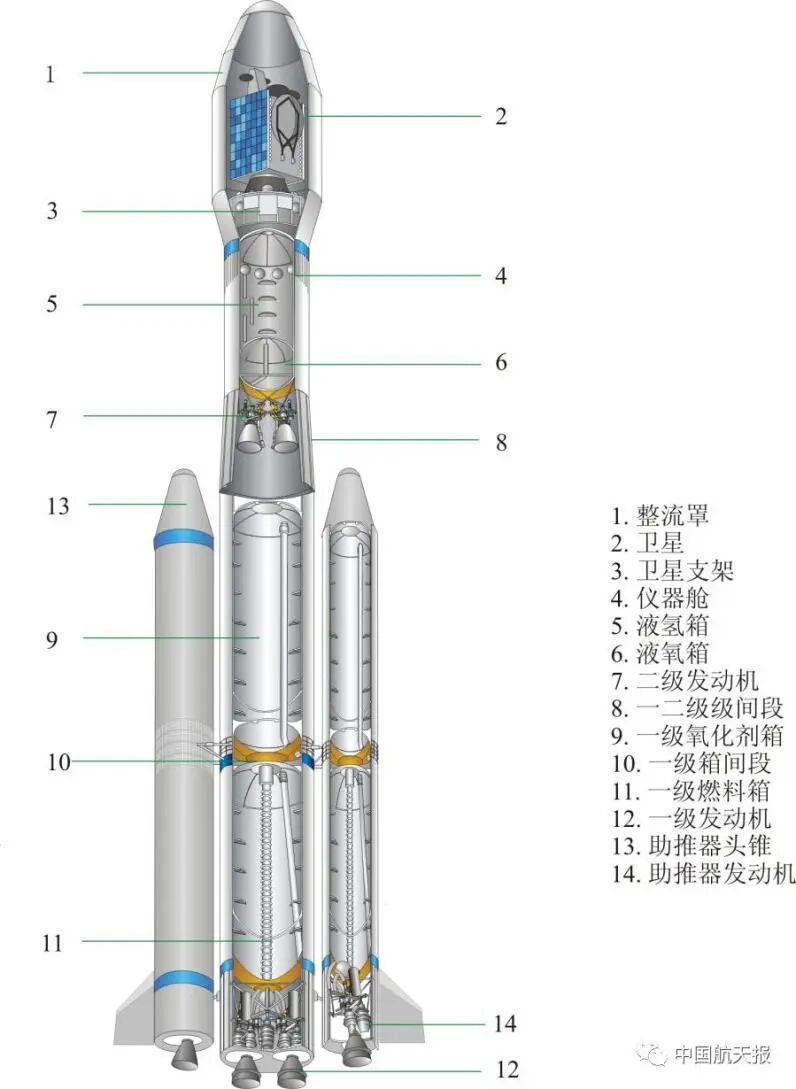

Figure: Basic Structure of a Rocket

Source: China Aerospace News, Dolphin Research

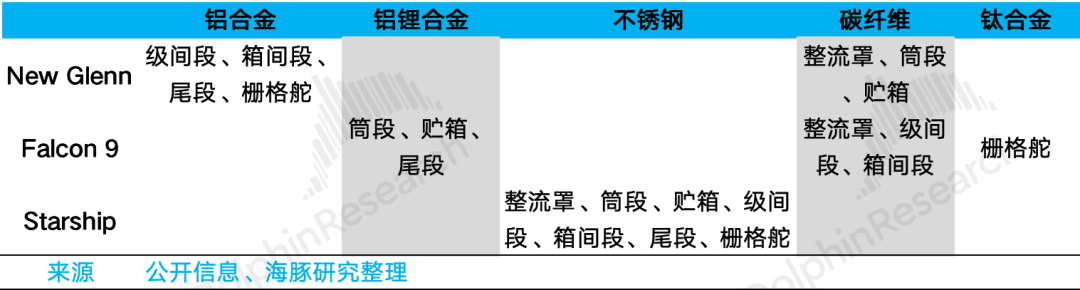

The rocket body includes the fairing, cylinder sections, tanks (for storing propellant), interstage sections, intertank sections, and tail sections. Material choices also differ for the body.

Blue Origin's Glenn primarily uses aluminum alloys and carbon fiber, while Falcon 9 extensively uses aluminum-lithium alloys, and Starship almost entirely uses stainless steel.

Here, Blue Origin's design approach still leans toward balancing performance and cost while optimizing based on mature solutions, whereas Starship attempts extreme cost reduction.

(3) GNC System

The GNC system refers to the rocket's guidance, navigation, and control systems.

The landing method is noteworthy: SpaceX's landing method is 'hover-and-stop,' where the rocket directly targets the landing point during descent, making minor adjustments to angle and position along the way, offering the highest efficiency and fuel savings. Blue Origin uses a 'drift method,' initially targeting a safe point outside the platform and then laterally translating to the platform center after confirming normalcy, ensuring maximum safety redundancy.

(II) Progress of Chinese Companies

Currently, industry participants are mainly concentrated in the United States and China, with a few participants in Europe and other regions, although progress is slower there and not discussed here.

In the first article, we briefly compared different rocket launch costs, showing that although China has not achieved reusability, its rocket launch costs do not differ significantly in magnitude from SpaceX's Falcon 9. Thus, if China achieves reusability, it may gain a cost advantage:

Based on China's manufacturing capabilities and cost advantages, Musk has experienced this with Tesla cars and Optimus humanoid robots: attempting complete vertical integration, independent R&D and production, then abandoning it, ultimately having to entrust manufacturing to the Chinese supply chain.

SpaceX is one of Musk's few industries capable of local manufacturing in the United States, relying on the disruption of rocket launch models. However, if China masters reusability, the impact on SpaceX could be significant.

Currently, China is still in a follower position regarding rocket reusability technology. Although this imitative approach may not be eye-catching, it aligns with China's engineering capabilities and scalability advantages.

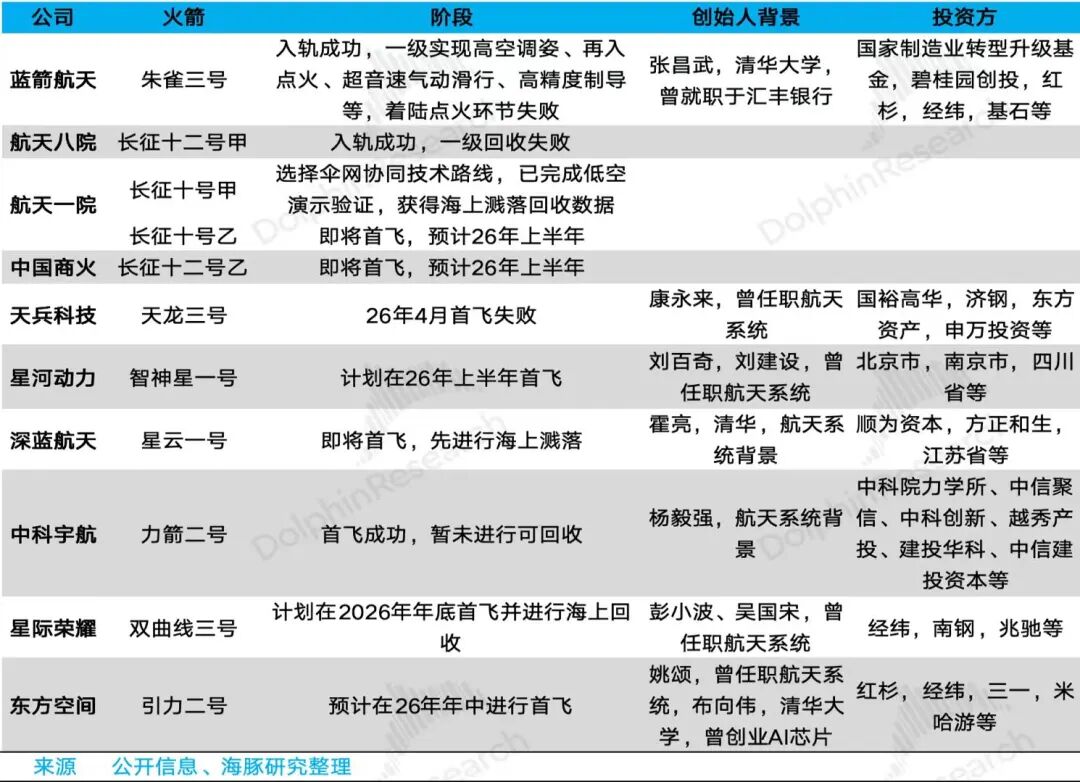

Here, we briefly review several Chinese companies making rapid progress:

1. LandSpace

Founded in 2015, LandSpace's founder, Zhang Changwu, has a financial background and previously worked at HSBC, while co-founder Wang Jianmeng has an aerospace system background, previously working at the China Satellite Launch and Tracking Control System Department and is also Zhang Changwu's father-in-law.

From a rocket R&D cycle perspective, LandSpace's progress is relatively fast compared to SpaceX.

LandSpace's reusable rocket, Zhuque-3, was initiated in 2023 and successfully launched into orbit in December 2025, taking just over two years. In contrast, SpaceX's Falcon 9 took five years from initiation (2005) to successful first flight (2010).

Figure: Zhuque-3

Source: LandSpace, Dolphin Research

Additionally, Zhuque-3 successfully achieved high-altitude attitude adjustment, re-entry ignition, supersonic aerodynamic gliding, and high-precision guidance during its December 2025 launch recovery process, although it failed to brake in the final stage and crashed, with a landing deviation of only about 40 meters. Falcon 9 achieved similar progress mainly between 2012-2014, 7-9 years after its initiation.

2. Aerospace Academy 8

Aerospace Academy 8's Long March 12A rocket was initiated in 2021, also using a liquid oxygen/methane route. Slightly later than Zhuque-3, it successfully launched into orbit in December 2025 but failed during the recovery process, appearing slower in progress than Zhuque-3 based on the recovery process.

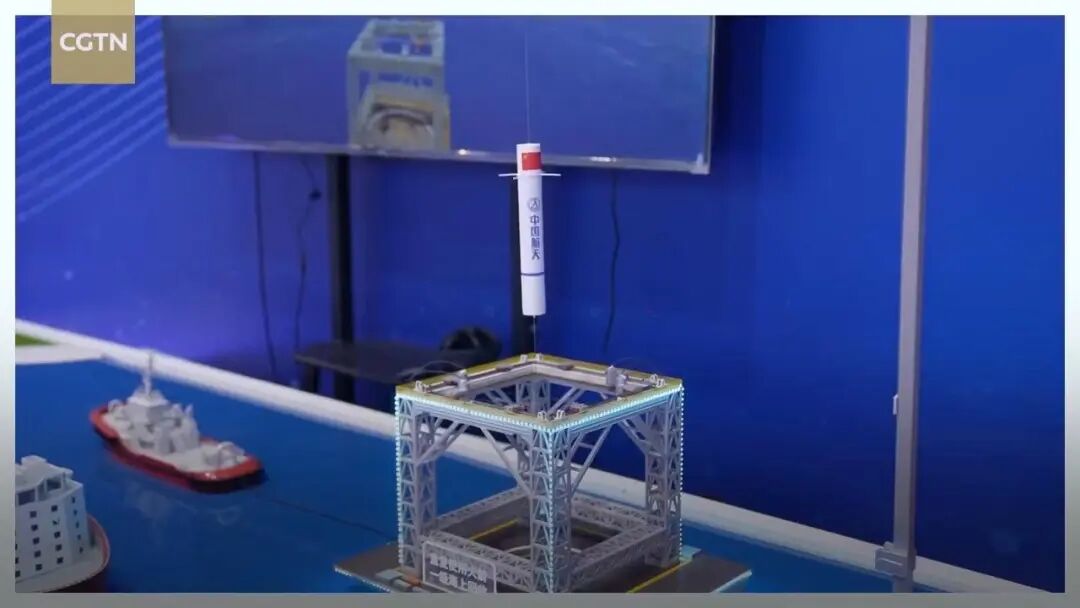

3. Aerospace Academy 1

Aerospace Academy 1's Long March 10A project was first disclosed to the public in 2024. In February 2026, Long March 10A successfully conducted a 'dual-payload test,' with the rocket's first stage successfully returning and achieving controlled sea splashdown.

Aerospace Academy 1's recovery method differs slightly from SpaceX's, using net-based recovery. In addition to relying on grid fins for attitude adjustment and short-term ignition reverse thrust to reduce descent speed near the end, it ultimately captures the rocket body using a net, a solution that may offer advantages in engineering reliability and cost.

Figure: Long March 10A Sea Splashdown

Source: China Aerospace Science and Technology Corporation, Dolphin Research

Figure: Models of Long March 10A and the offshore network recovery platform

Source: CGTN, Dolphin Research

(III) Rocket Lab

If China's reusable rocket technology matures, it could first compete for SpaceX's commercial orders, although these represent a relatively minor portion of SpaceX's business. However, for SpaceX's government and military contracts, besides Blue Origin, other strong competitors will also vie for a share.

This section focuses on Rocket Lab.

Rocket Lab has taken a

Rocket Lab's Electron rocket is uniquely positioned to offer dedicated orbital deployment services for small satellites, establishing a distinct competitive edge over SpaceX's Falcon 9 and addressing a critical market gap. To draw a vivid analogy, if Falcon 9 represents a bus, then Electron embodies a taxi, catering to specific needs with precision.

2. U.S. Government and Military Security Requirements

On one front, the U.S. government and military exhibit a clear demand for rocket launches, particularly those characterized by high frequency and reliability. On the other hand, from the perspective of government and military procurement, allowing a single supplier to dominate and form a monopoly is untenable. Consequently, fostering secondary and tertiary suppliers becomes imperative, which is precisely why Rocket Lab swiftly secured cooperation with the U.S. Department of Defense shortly after its inception.

3. Unique Engineering Culture, Highly Vertical Integration, and Unparalleled Cost-Reduction Capabilities

Rocket Lab's founder, Peter Beck, lacks a university degree but has harbored a lifelong passion for manufacturing. His formative years were spent in yacht and appliance manufacturing, where he amassed a wealth of engineering experience.

Peter Beck embodies a highly pragmatic approach. Recognizing the innovation deficit and exorbitant costs plaguing the U.S. aerospace industry, he resolved to develop cost-effective rockets. Upon founding the company, he maintained a hands-on technical involvement, enabling prompt error correction. For instance, he initially declared his intention not to pursue recovery but swiftly pivoted after witnessing SpaceX's success.

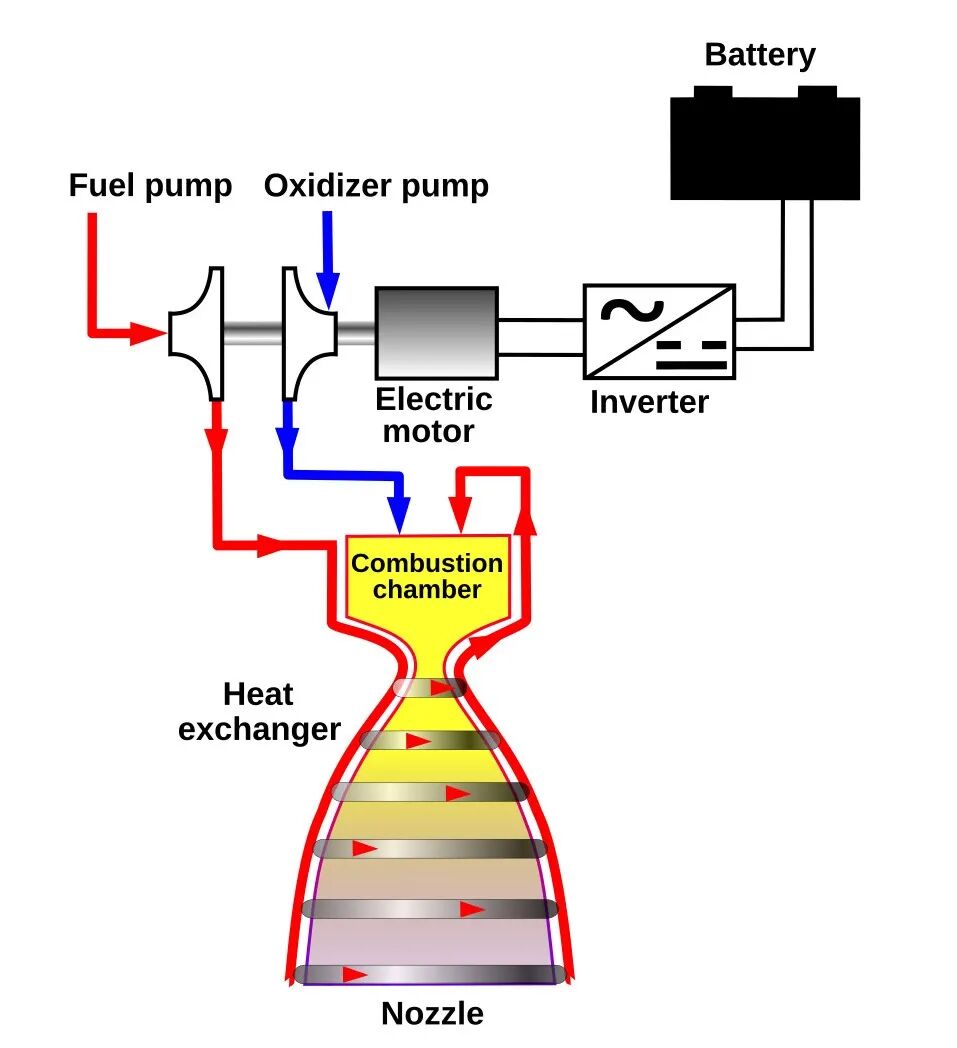

This pragmatism permeates the rocket's design philosophy. Electron, with its differentiated positioning, adopts a technical route vastly distinct from SpaceX's. For example, its Rutherford engine employs an Electric Pump-Fed Cycle, utilizing lithium batteries to power a motor that drives the turbopump, meeting the demands of a small rocket. Furthermore, the main components of the Rutherford engine are entirely produced using 3D printing, showcasing a more thorough application of this technology than SpaceX.

Figure: Electric Pump-Fed Cycle

Source: Wikipedia, Dolphin Research

Figure: Rocket Lab's Carbon Fiber 3D Printer

Source: Rocket Lab, Dolphin Research

Rocket Lab exemplifies exceptional execution, having successfully developed Electron with a mere $100 million investment and rapidly establishing cross-hemisphere launch centers, manufacturing facilities, and R&D bases while cultivating vertically integrated capabilities.

Figure: Rocket Lab's Launch Bases in New Zealand and Virginia, USA

Source: Rocket Lab, Dolphin Research

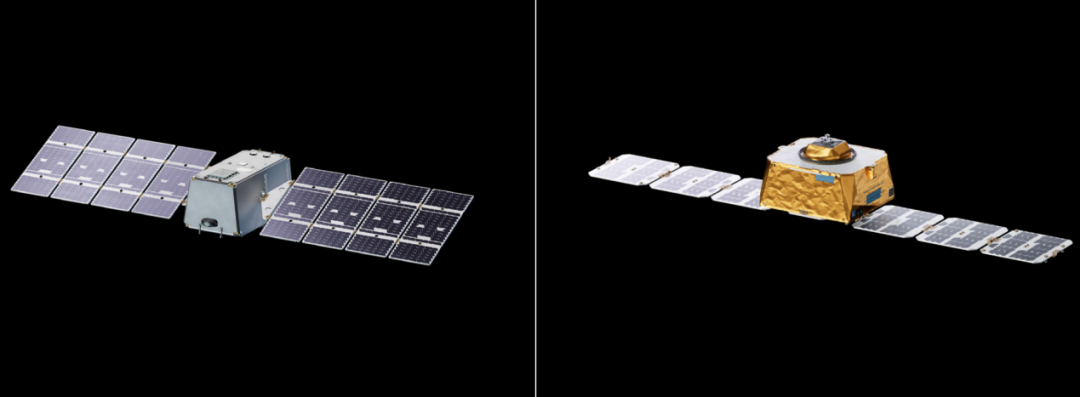

Rocket Lab not only manufactures rockets but also produces satellites and constructs satellite platforms, offering customers turnkey satellite solutions.

Moreover, Rocket Lab has achieved self-reliance in researching and producing core satellite subsystems and their components, selling them directly to customers. These encompass, but are not limited to, GNC system core components such as star trackers and reaction wheels, as well as communication systems, separation systems, photovoltaic systems, and even space software.

Figure: Star Tracker & Reaction Wheels Produced by Rocket Lab

Source: Rocket Lab, Dolphin Research

Figure: Photovoltaic Array System Produced by Rocket Lab

Source: Rocket Lab, Dolphin Research

Much of Rocket Lab's vertically integrated capabilities have been realized through strategic acquisitions, underscoring its business integration prowess. For instance, it acquired Geost to gain electro-optical and infrared system capabilities and SolAero to acquire radiation-resistant photovoltaic cell and module array manufacturing capabilities.

Looking ahead, Rocket Lab's competition with SpaceX will transcend mere differentiated positioning.

In the realm of rockets, Rocket Lab's next-generation rocket, Neutron, directly competes with Falcon 9, primarily targeting large constellation deployments and deep space exploration. Neutron's maiden flight is anticipated in the first quarter of 2026.

Neutron's design approach also diverges significantly from mainstream solutions. For example, its fairing, dubbed Hungry Hippo, is integrated with the first stage and releases the second stage like a hippo's mouth post-launch, then returns to the ground with the first stage, enhancing fairing recovery efficiency and reducing costs. The second stage is housed within the fairing, eliminating the need for a robust rocket structure like other rockets, thus reducing size and allocating more weight and cost to the first stage, amplifying the cost-dilution effect of first-stage recovery.

Figure: Neutron Fairing Opens and Releases Second Stage

Source: Rocket Lab, Dolphin Research

In the satellite domain, Rocket Lab has unveiled the Flatellite satellite platform, focusing on augmenting the number of satellites deployed per launch. Combined with its satellite manufacturing platform, it harbors the potential to transition into a "service provider," constructing its own satellite constellation to rival Starlink.

II. Competitive Landscape in Constellation Operations

Not only in reusable rockets but also in constellation operations, SpaceX faces escalating competition.

SpaceX's Starlink offers a multitude of services, primarily global internet connectivity, akin to the broadband we utilize daily. To access this service, users must procure a dedicated ground terminal: the Starlink Terminal, whose main component is a phased array antenna, functioning similarly to an optical modem.

Figure: Starlink Terminal

Source: SpaceX, Dolphin Research

Source: SpaceX, Dolphin Research

Another service under development is D2D (Direct to Device), also referred to as D2C (Direct to Cell) by SpaceX, comparable to the cellular networks we utilize daily. Through this service, mobile phones can directly connect to satellites.

1. Global Internet Connectivity: Facing Challenges from Bezos

(1) Blue Origin's Strategic Layout

Bezos' Blue Origin's Project Kuiper is advancing rapidly, directly competing with Starlink, and has already launched over 100 satellites into space. Additionally, Amazon plans to launch the TeraWave project, offering higher bandwidth and faster services, specifically targeting high-end commercial clients.

(2) Chinese Companies' Strategic Layouts

China has initiated constellation projects such as GW (China Starnet), Qianfan (Shanghai GX), and Honghu, with Qianfan positioned as a commercial project serving individual and enterprise clients.

From a regulatory standpoint, China Starnet and Shanghai GX have both secured satellite internet licenses in mainland China. By the end of 2025, China submitted frequency and orbital resource applications for 14 constellations, including GW and Qianfan, to the ITU (International Telecommunication Union, the sole global authority responsible for managing satellite radio frequencies, orbital resources, and setting international standards for satellite communications), totaling 203,000 satellites, far surpassing Starlink's current in-orbit numbers.

2. D2D, or Direct-to-Device, Also Faces Competitors

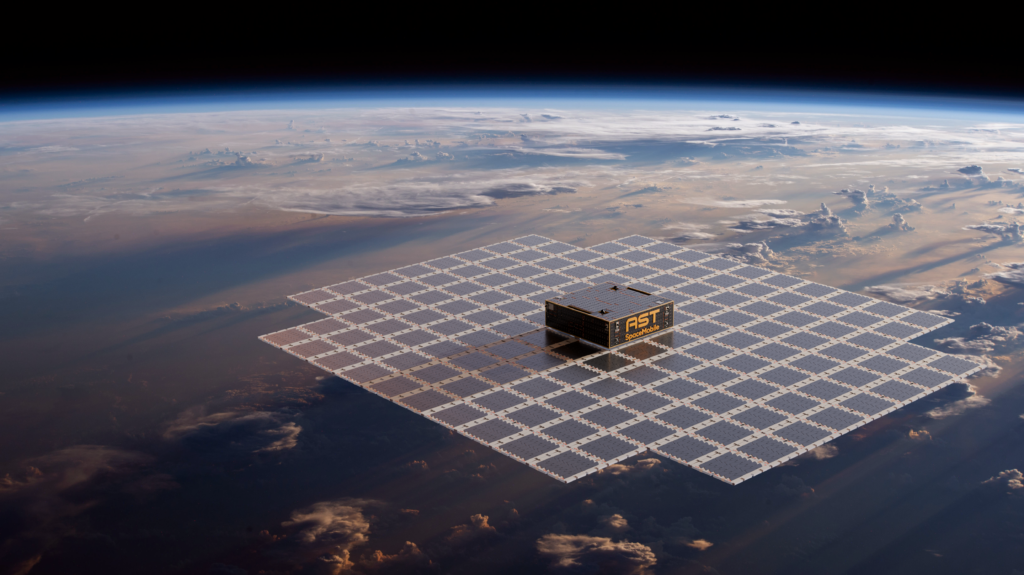

U.S. startup AST SpaceMobile is advancing its direct-to-device satellite service.

In terms of constellation size, AST pales in comparison to Starlink, utilizing only a few dozen satellites. Although it claims to employ giant phased array antennas to compensate for the limited number of satellites, there likely remains a gap compared to Starlink's tens of thousands of satellites. Otherwise, Starlink could have considered a similar or hybrid solution.

However, considering that AST is backed by industry giants like Google, it could exert certain pressure on SpaceX. Additionally, several other D2D projects are also progressing in the U.S.

Figure: AST SpaceMobile Satellite Provides D2D Service via Giant Phased Array Antenna

Source: AST SpaceMobile, Dolphin Research

However, the crux lies in the fact that while satellite and communication technologies face competition in terms of technical prowess and manufacturing capabilities, there are no disruptive barriers. Therefore, constellation operators pose a relatively limited direct threat to SpaceX. Nonetheless, as Blue Origin's rocket technology matures, satellite operators will have more cost-effective options, which is the core competitive factor. Thus, the crux still lies in the competition within the reusable rocket sector.

3. There Exists an Urgency in the Current Competition for Spectrum and Orbital Resources.

(1) Limited Resources

Both spectrum and orbital resources are finite and adhere to the first-come, first-served principle.

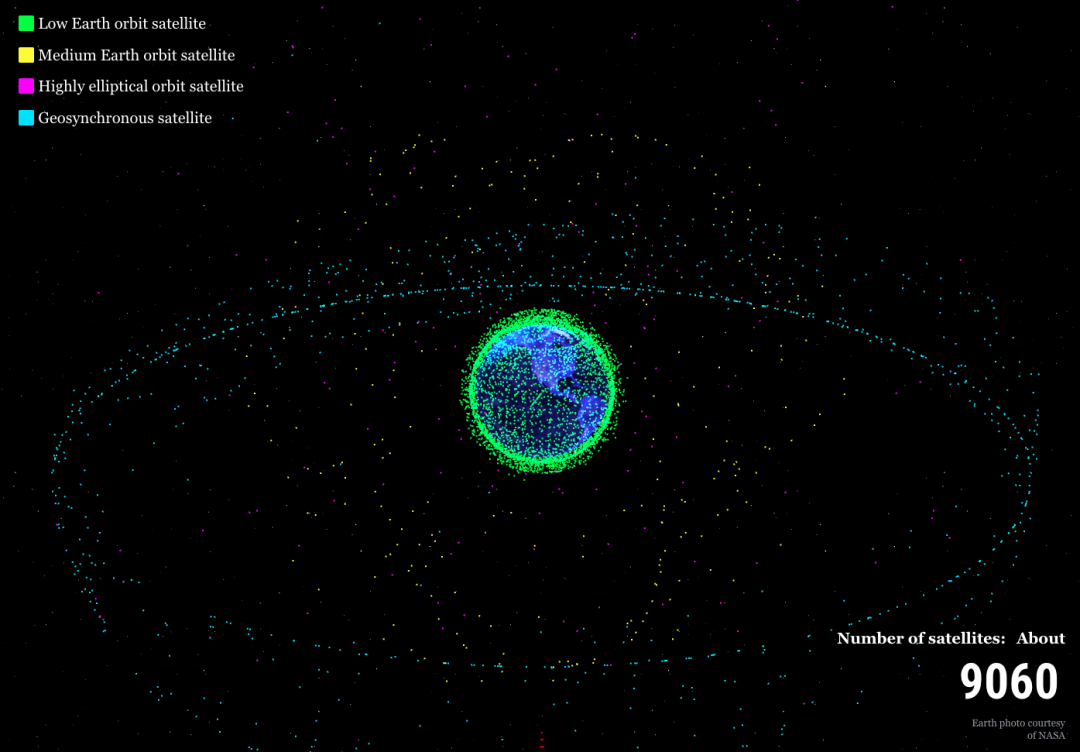

Particularly for orbital resources: Theoretically, the upper limit for the capacity of low-Earth orbit satellites is only about 60,000. Starlink already has nearly 10,000 satellites in orbit, yet currently, countries have submitted applications to the ITU for several hundred thousand satellites.

Figure: Illustration of Satellites in Orbit

Source: NikkiAsia, Dolphin Research

According to ITU regulations, by the 7th year from the date of application, the first satellite must be launched and successfully placed into orbit, operating normally for 90 days. By the 9th year, 10% of the total applied satellites must be deployed, 50% by the 12th year, and 100% by the 14th year.

(2) National Security Imperatives

From a national strategic and military perspective, during the earlier Russia-Ukraine conflict, Starlink demonstrated significant military value: Despite the near-total destruction of Ukraine's traditional communication infrastructure, Starlink ensured that Ukraine could maintain nationwide network connectivity. Simultaneously, Starlink assisted Ukraine in conducting reconnaissance and communication tasks via drones, coordinating remote collaborative operations of heavy weaponry units, and enabling the Ukrainian military to maintain constant contact and exchange information with NATO.

Thus, the competition for orbital and spectrum resources is not solely about commercial value but, more crucially, relates to each country's communication rights and national security.

Currently, there exists a critical window of opportunity. Whoever can launch more satellites to occupy positions swiftly will secure an advantageous position in future competition. Whether it is the United States or China, 2026 will witness an increasing number of reusable rockets entering practical launch testing phases, reflecting the current competitive stage of the industry.

3. How to Interpret the Opportunities?

1. Rocket Launch Companies

Firstly, SpaceX has pioneered commercial spaceflight towards reusable technology, significantly reducing launch costs and objectively accelerating explosive growth in commercial spaceflight demand. Considering the accelerated promotion and phased successes by numerous participants, we have reason to believe that rocket reusability technology will continue to rapidly iterate towards full reusability—it is only a matter of time.

Simultaneously, the industry is challenging to monopolize exclusively. SpaceX has blazed a viable path, providing a reference model for latecomers and thereby shortening their research and development cycles. Meanwhile, Bezos has adopted a relatively conservative approach, achieving phased success despite a slower pace. Additionally, from the demand side's perspective, it is challenging to accept a single dominant supplier, necessitating efforts to support competitors and further enhance the catch-up capabilities of latecomers.

However, looking back, SpaceX still maintains a clear lead in rocket technology. Especially if Starship successfully achieves full reusability, it could once again lead in a discontinuous manner in terms of launch costs. From the Starlink perspective, the network effects formed by its early deployment also help maintain its first-mover advantage.

In summary, as a blue ocean industry, we believe that on the one hand, attention should be paid to SpaceX's opportunities, and on the other hand, opportunities for challengers should also be considered.

Among the challengers, Rocket Lab is noteworthy due to its technological leadership, rapid iteration capabilities, and core positioning in government and military service sectors. However, close attention should be paid to the progress of the maiden launch of its Neutron rocket.

2. Constellation Operation Companies

We tend to prioritize rocket launch companies over satellite operation companies. Firstly, for LEO (low-Earth orbit) constellation operation companies, under the competitive landscape dominated by giants like SpaceX and Blue Origin, the core observation point is whether they can find their differentiated competitive advantages in terms of price, performance, and service. For traditional GEO communication satellite operation companies, they face comprehensive challenges from LEO constellations like Starlink, and their transformation progress is worth monitoring.

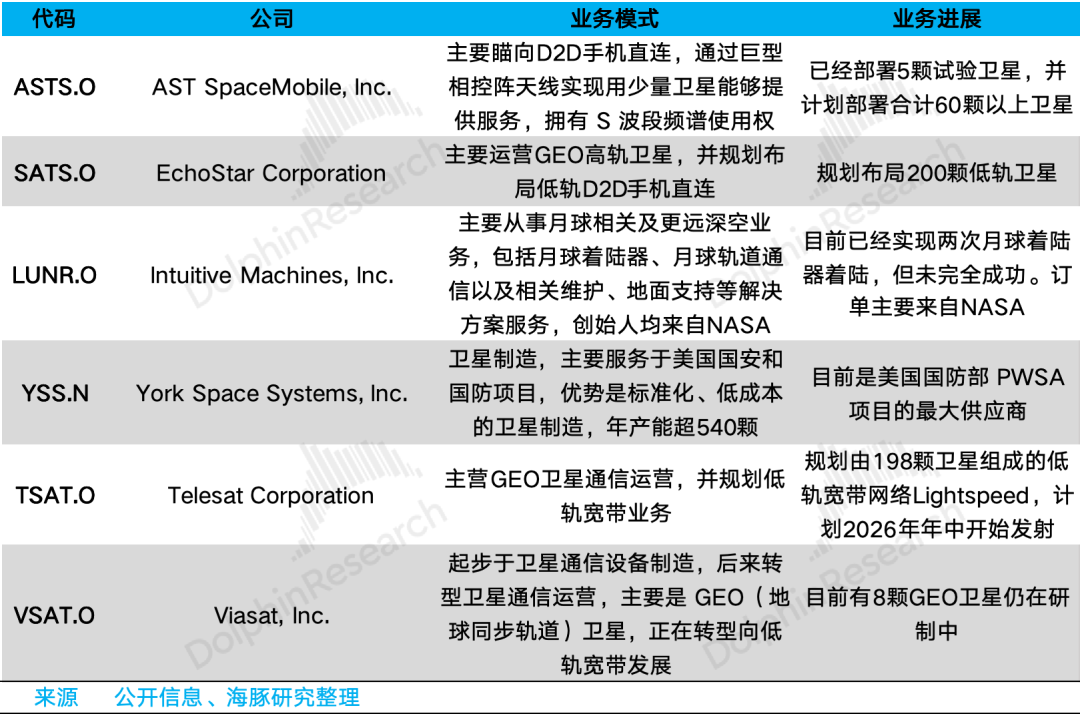

Below are the main satellite operation companies listed in the US stock market:

3. Upstream Supply Chain Dynamics

The burgeoning demand within the industry naturally heralds opportunities for the upstream industrial chain, with particular emphasis on the following sectors:

(1) Core Components for Reusable Rockets and Cost Optimization

Driven by the imperative for rocket reusability and drastic cost reductions, key components such as engines, rocket body materials, Guidance, Navigation, and Control (GNC) systems, along with manufacturing technologies like 3D printing, are in the spotlight.

SpaceX exemplifies a high degree of vertical integration, while Blue Origin undertakes in-house R&D and production of engines and rocket body structures. Similarly, Rocket Lab internalizes the development of engines, rocket body structures, GNC systems, and even certain composite materials. For these entities, external procurement predominantly encompasses bulk materials and select electronic components, such as chips.

(2) Satellite Proliferation and Performance Enhancement

The exponential growth in satellite numbers and performance enhancements, particularly the anticipated surge in demand from future computing satellites, will fuel demand in upstream component sectors. Furthermore, given the pressing need for cost reductions in rockets and the cost dilution per launch facilitated by reusable models, the demand growth rate for satellite components may outpace that of rocket components. This trend is illustrated by:

1) Solar Arrays: Computing satellites are projected to consume significantly more power than communication satellites. Assuming a single-satellite power consumption of 100kW, this would represent approximately four times the current power consumption of Starlink communication satellites.

2) Thermal Management Systems: Elevated power consumption necessitates enhanced heat dissipation capabilities, while system complexity escalates sharply. Consequently, the value of thermal management components for computing satellites is expected to surge.

3) Laser Communication Equipment: Inter-satellite communication bandwidth is experiencing rapid expansion. Starlink satellites currently achieve 100Gbps, roughly five times that of GEO high-throughput satellites. However, computing satellites may demand bandwidth up to 10Tbps, marking a hundredfold increase.

Regarding solar arrays, both SpaceX and Rocket Lab engage in in-house R&D and production. Nonetheless, future technological shifts may necessitate external procurement, particularly if silicon-based photovoltaic cells are adopted. For thermal management-related components, SpaceX relies on external suppliers for materials and components. In the realm of laser communication equipment, SpaceX develops terminals internally but depends on external suppliers for related chips, sensors, and modules.

The relevant US and European companies involved in these supply chains are often subsidiaries of major corporations or privatized entities yet to go public. Independent publicly traded companies are relatively scarce, primarily due to the consolidation of the manufacturing industry in the US and Europe over the past few decades. This consolidation has led to a decline in professional manufacturing companies, with the landscape now dominated by giant multinational corporations.

Some pertinent US stock market companies within the industrial chain are depicted in the figure below:

In the Chinese market, several listed companies are involved in the production of relevant upstream components and parts. Their potential listings on the Hong Kong stock exchange warrant subsequent monitoring.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models