Soaring Oil Prices Propel March NEV Market: Leapmotor Leads, NIO Surges, XPENG Falters

04/10 2026

04/10 2026

489

489

Author | Guanchejun

The recently concluded month of March witnessed China's new energy vehicle (NEV) market shedding its "sluggish" tag from January and February, marking the year's first true, uninterrupted full sales month.

However, the outcomes triggered a mix of jubilation and anxiety: Leapmotor surpassed the 50,000-unit sales milestone for the first time, NIO witnessed a 136% year-on-year surge, while former NEV star XPENG experienced three consecutive months of decline, and Xiaomi tumbled from a high position to the 16th spot.

Market differentiation has intensified beyond expectations.

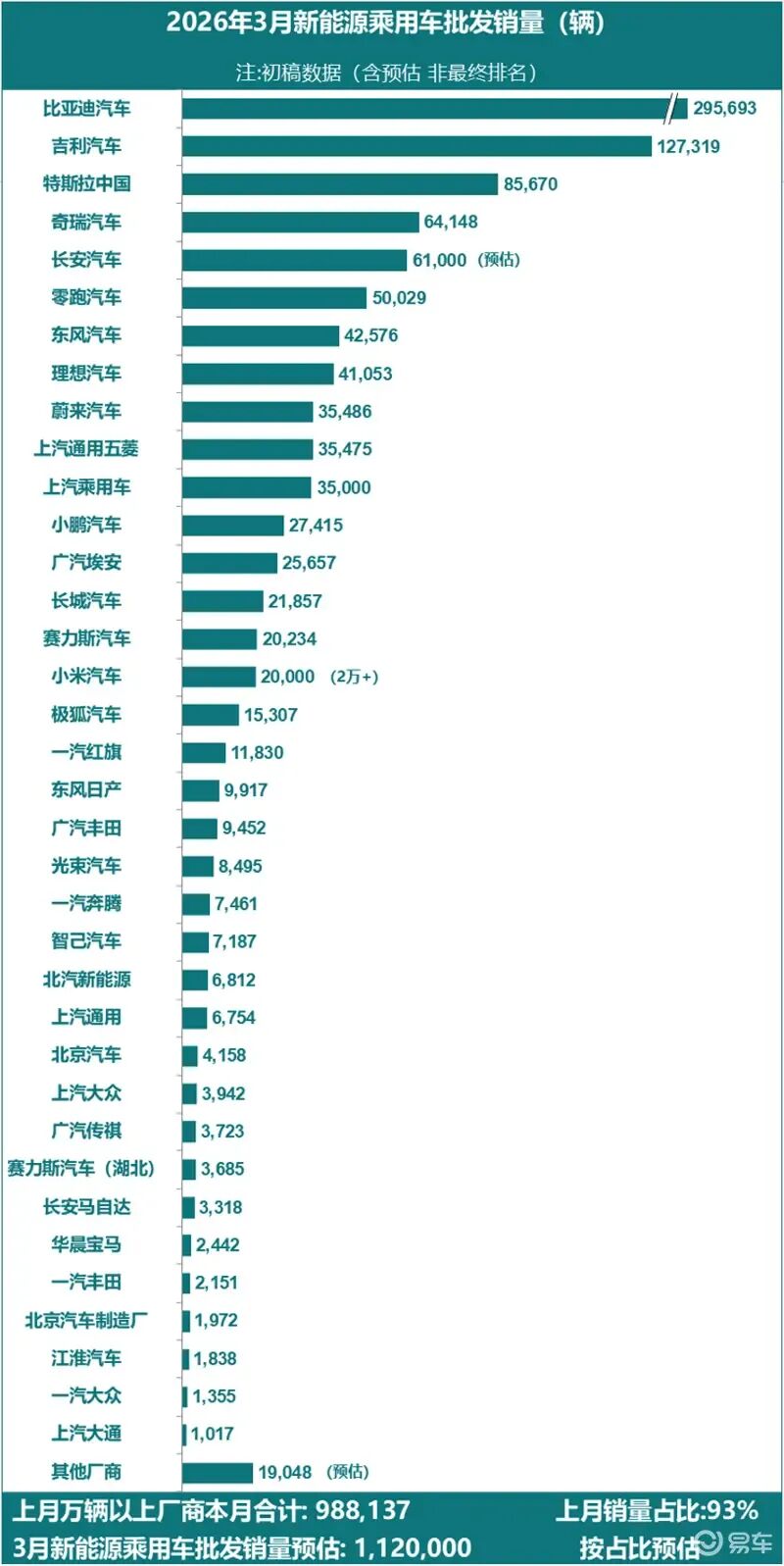

As depicted in the table, traditional independent automakers dominated March's NEV market. BYD maintained its top spot with 295,693 monthly sales, despite a 30.13% year-on-year decline. However, it achieved a remarkable 57.85% month-on-month surge, with exports nearing 120,000 units (+65% YoY).

Geely's NEV sales exceeded 127,300 units, with new energy vehicles accounting for 55% of its total sales, securing the second position.

Chery's overall sales reached 240,700 units (+12.1% YoY), with exports hitting a record 149,000 units for a Chinese brand in a single month.

In general, leading domestic automakers are leveraging domestic recovery and overseas expansion to capture market share.

The new energy startup sector remained fiercely competitive.

Leapmotor led the startup rankings with 50,029 deliveries in March (+35% YoY, +78% MoM), maintaining its lead for three consecutive months.

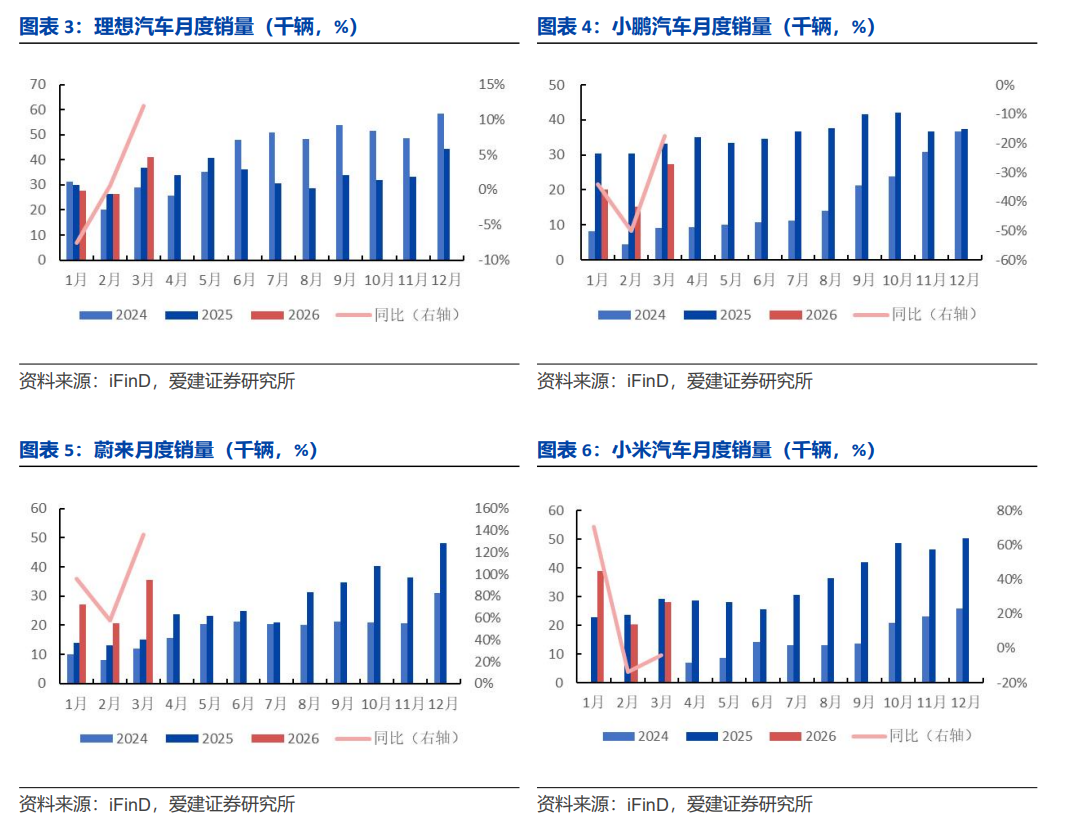

Li Auto followed closely with 41,053 units (+12% YoY), with its Li L6 model contributing approximately 24,000 units as a key growth driver for pure electric SUVs.

NIO emerged as the dark horse with 35,486 units (+136% YoY), with its new ES8 winning the large SUV sales crown for three consecutive months. Meanwhile, its Lexee and Firefly brands both exceeded 130% month-on-month growth, showcasing its full matrix strength.

While some brands surged ahead, others faced challenges. This time, XPENG fell behind.

In March, XPENG delivered 27,415 units (-17.4% YoY), marking its third consecutive month of decline. Its MONA M03 model neared the end of its lifecycle, with no successor yet launched, creating a product gap.

Xiaomi slid to the 16th position from its previous high, with sales plunging to approximately 28,000 units.

Data reveals three distinct tiers among new energy startups in 2026, strictly divided by the 30,000-unit threshold.

The first tier (30,000+ units/month 'safe zone') comprises Leapmotor, Li Auto, NIO, and Seres. These brands share clear strategies and stable economies of scale.

The second tier (20,000-30,000 units/month 'survival breakthrough zone') features Zeekr, XPENG, and Xiaomi. This is the most competitive segment, where brands either ascend to mainstream status or face marginalization. Zeekr boasts strong product competitiveness and stable pricing but lacks a true 20,000-unit/month blockbuster. XPENG excels technically but lags in product rhythm, pricing strategy, and iteration speed. Xiaomi faces production and delivery cycle constraints.

The third tier (below 20,000 units/month 'niche struggle zone') includes brands like IM Motors and VOYAH. These rely on niche markets without a national-scale presence or brand barriers, facing immense growth pressures.

Overall, the NEV market is witnessing rising concentration, with the Matthew effect reaching extremes. Tail-end brands delivered fewer than 2,000 units monthly, including SAIC Maxus, FAW-Volkswagen, and JAC Motors.

This elimination race has proven far crueler than imagined.

Notably, exports surged in March, with 349,000 new energy passenger vehicles shipped (+139.9% YoY, +29.6% MoM), accounting for over 50% of passenger vehicle exports for the first time. Global high oil prices played a significant supporting role.

Overseas expansion has become the primary variable for leading automakers to offset domestic pressures. Those expanding overseas markets most effectively will gain a competitive edge in profits and valuations.

Looking ahead, three trends will shape China's NEV market in 2026 amid intensifying competition:

First, electrification is irreversible. March saw NEV retail penetration reach 47.3%, firmly establishing an "electric-dominated" era while systematically eroding fuel vehicle market share.

Second, centralization is inevitable. Leading automakers' dominance solidifies, with second-tier and tail-end players' survival space shrinking. The 30,000-unit/month threshold marks entry, while 50,000 units/month ensures safety. Brands below this line face limited time.

Third, technological advancement is unstoppable. Amid cost pressures, only those achieving genuine technical breakthroughs will survive value competition.

All charts without specific attribution originate from publicly disclosed sources across various channels. The views expressed herein are for reference only and do not constitute investment advice. This article is original content from Leverage Auto Insights and prohibited from reproduction without authorization. For reuse, please obtain permission.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry