1.2 Billion Loss + Prospectus to Expire: Carlink's Darkest Hour Outweighs Its Glory

05/22 2026

05/22 2026

448

448

This article is the 1039th original work by DeepDive Atom.

Leading in Technology and Market,

Yet Trapped in Profitability Dilemma

Meng Fanle 丨 Author

DeepDive Atom Studio 丨 Editor

The rise of the new energy vehicle industry has spurred significant demand in the smart cockpit sector. Consumers' needs for vehicles have transcended mere transportation, shifting towards smarter cockpit experiences. This has driven cockpit functions to evolve from basic audio-visual entertainment to diversified scenarios such as multi-screen interconnection, voice interaction, and cockpit-driving collaboration. However, with increased functional integration, there is an urgent need for reliable control systems to coordinate and avoid safety hazards, which is the core background for the rise of the smart cockpit control system sector.

As such, Carlink, focusing on smart cockpit domain controllers and full-stack telematics solutions, has precisely tapped into the industry trend. Leveraging its leading technology implementation capabilities and mass production advantages, it has become an industry favorite, gaining favor from automakers and capital. It has secured design wins for over 100 vehicle models and completed nearly 2 billion yuan in financing.

On November 28, 2025, Carlink submitted its prospectus to the Hong Kong Stock Exchange (HKEX). Despite seemingly bright prospects, Carlink's prospectus submitted to the HKEX may expire due to failing to pass the hearing within six months. If it fails to complete the listing as scheduled, Carlink will face a more passive capital dilemma.

Leading in Technology but Trapped in Profitability Dilemma

Founded in 2014, Carlink focuses on core components for smart vehicles and has grown into a domestic provider of smart cockpit domain controllers and full-stack telematics solutions, positioning itself as a core supplier for automotive electronic and electrical architecture upgrades. Unlike some companies that focus on laboratory R&D, Carlink adheres to the philosophy of "technology-based, application-oriented" and focuses on technology mass production. Its products include smart cockpits and cockpit-driving fusion domain controllers.

In terms of technological layout, Carlink closely follows industry trends, deploying intelligent agents and AI large model in-vehicle applications. Relying on its self-developed Autosee OS in-vehicle operating system, it achieves multi-chip adaptation and multi-domain fusion, supporting complex tasks such as end-side AI large models and visual recognition. It has launched the AI Box product to upgrade the intelligent functions of existing vehicles.

At the same time, Carlink has deep cooperation with Qualcomm, taking the lead in mass-producing domain control products for high-end chips such as Snapdragon SA8155P and SA8775P. Among them, the AL-A1 cockpit-driving fusion domain controller based on SA8775P was the world's first, applied to two models of BAIC Arcfox, driving the fusion technology from concept to implementation.

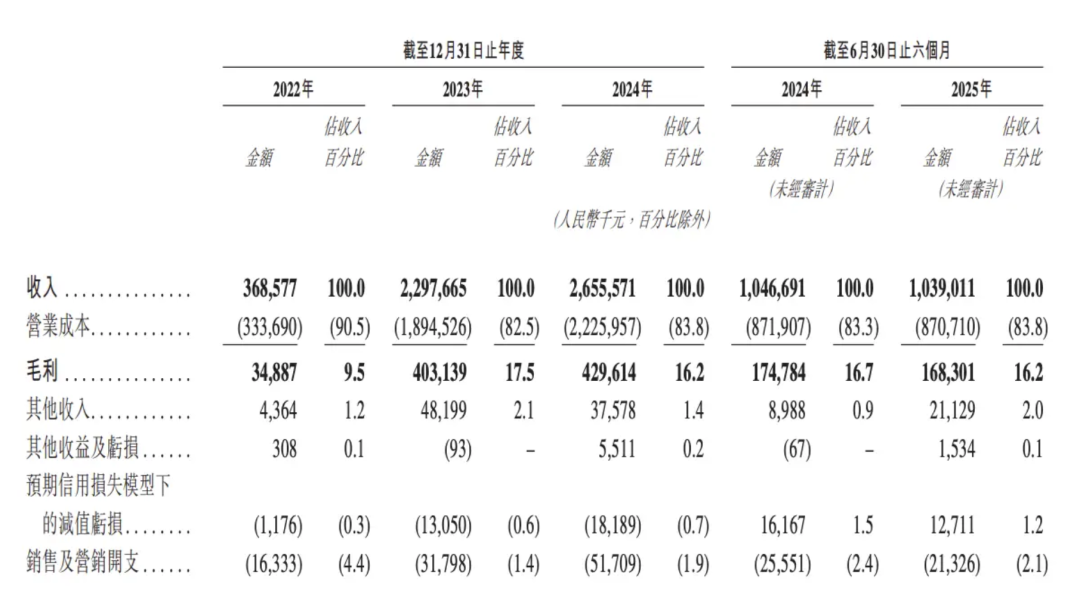

Meeting market demand, Carlink has demonstrated strong revenue growth. Revenue surged from 369 million yuan in 2022 to 2.298 billion yuan in 2023, a year-on-year increase of 522.76%; it reached 2.656 billion yuan in 2024, a year-on-year increase of 15.58%; in the first half of 2025, revenue declined by 0.76% year-on-year. Although growth momentum has slowed, overall revenue still reached 1.039 billion yuan, and Carlink's market position has been initially confirmed.

According to Frost & Sullivan reports, as of June 30, 2025, Carlink ranked first globally in shipments of smart cockpit domain controllers on the Qualcomm Snapdragon SA8155P platform.

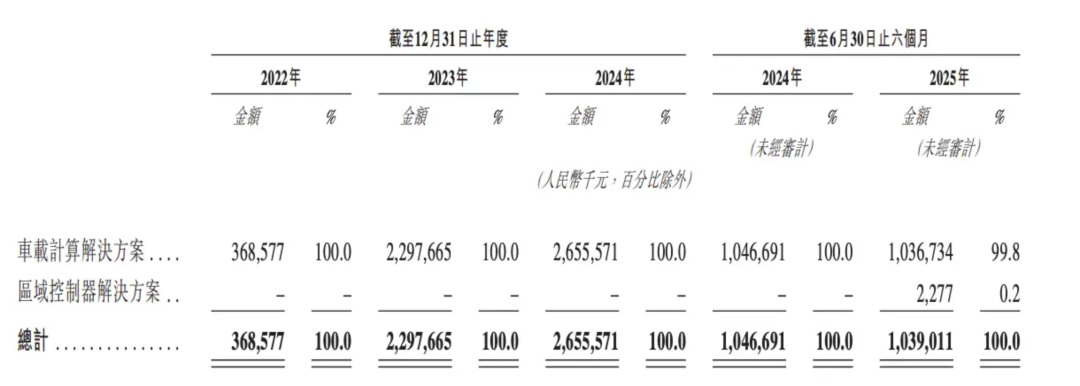

Its business structure is highly concentrated, with in-vehicle computing solutions being the absolute core, accounting for 100% of revenue in 2024. Among them, the cumulative shipments of smart cockpit domain controllers based on SA8155P rank first globally; Autosee OS software is only matching (peitao, meaning "bundled with") hardware and has not been commercialized separately. The regional controller business has not yet been scaled, with revenue of 2.277 million yuan in the first half of 2025, accounting for only 0.2%.

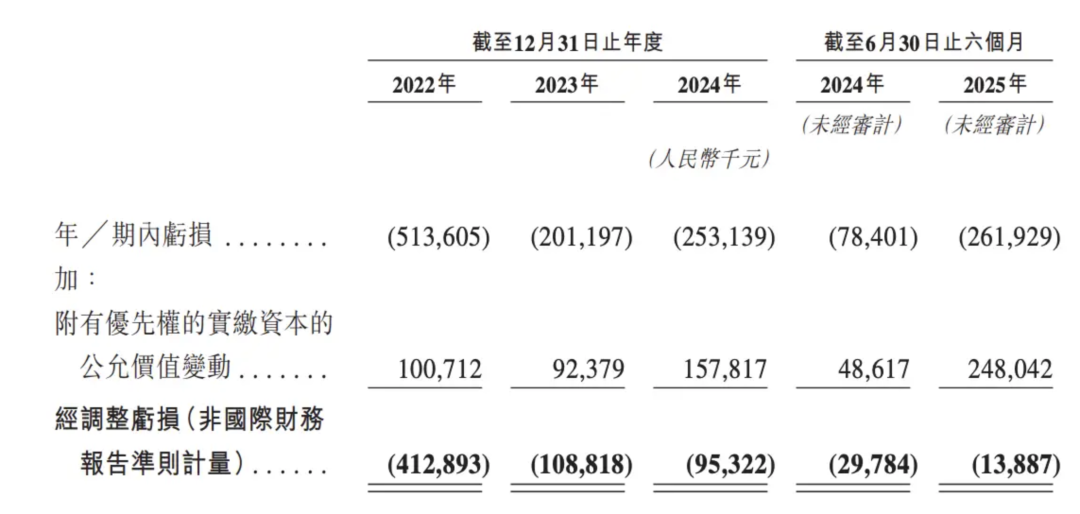

Behind the impressive revenue figures lie continuous substantial losses. From 2022 to the first half of 2025, Carlink accumulated losses exceeding 1.2 billion yuan; net losses were 514 million yuan in 2022, narrowed to 201 million yuan in 2023, expanded to 253 million yuan in 2024, and surged to 262 million yuan in the first half of 2025, a year-on-year increase of 235.36%.

From 2022 to the first half of 2025, Carlink's gross margins were 9.5%, 17.5%, 16.2%, and 16.3%, respectively. Such low gross margins naturally make it difficult for Carlink to generate profits, reflecting its insufficient supply chain control.

At the supply chain level, Carlink is highly dependent on Bosch, with procurement of PCBAs and related services accounting for 79.1%, 82.9%, 80.3%, and 75.4% of total procurement during the prospectus period. This single-supplier dependency leaves Carlink passive in pricing negotiations. In 2024, Bosch's price hikes increased raw material costs, and Carlink lacked alternative suppliers, highlighting the fragility of its supply chain.

Simultaneously, Carlink's extremely high customer concentration poses another major risk. During the prospectus period, the top five customers contributed 95.3%, 99.5%, 98.7%, and 99.2% of revenue, respectively; among them, the largest customer accounted for approximately 40.1%, 59.0%, 58.7%, and 42.7%.

High R&D investment supports technological leadership but is also a significant cause of losses. R&D investment was 368 million yuan in 2024 and 142 million yuan in the first half of 2025, focusing on smart cockpits and cockpit-driving fusion to ensure product competitiveness. Thanks to continuous investment, Carlink ranked second in the domestic cockpit domain control industry by revenue in 2024, with cumulative SA8155P shipments ranking first globally. However, persistent high R&D spending, coupled with supply chain constraints, warrants close attention.

Carlink's long-term goal is cockpit-driving fusion, which is also an industry trend. According to Frost & Sullivan, in China, passenger vehicle installations are expected to increase from 200,000 units in 2024 to 500,000 units in 2025 and reach approximately 7.6 million units by 2029, with a compound annual growth rate of 107.0% during the period. However, this does not resolve Carlink's immediate issues. Additionally, the current standalone chip intelligent driving route is still being explored, with slow commercialization and immature intelligent driving technology. Cockpit-driving fusion needs to address complex issues such as computing power allocation and functional safety, and technological integration risks may impact development.

Overall, while Carlink has tapped into the industry trend, continuous losses, dual concentration risks, and a single profit model remain core risks. Short-term profitability is challenging, and long-term success depends on the implementation of fusion technology and software commercialization.

Prospectus About to Expire, Capital Gambling Crisis Looms

The smart cockpit sector is fiercely competitive, with Carlink facing pressure from both domestic and international players. Domestically, Desay SV leads, while Foryou Corporation and Joyson Electronics compete in the mid-to-low-end market and penetrate the high-end segment. Overseas, giants like Bosch and Continental have significant advantages in high-end cockpit-driving fusion and central computing, making Carlink's high-end breakthrough extremely difficult.

Leveraging its first-mover advantage, Carlink remains the global leader in cockpit domain controller shipments and the second-largest domestic player in terms of revenue. Its core competitiveness lies in its technology implementation capabilities and customer resources. It was the first to mass-produce domain control products for multiple high-end Qualcomm chips, possesses its self-developed Autosee OS, and collaborates deeply with Qualcomm and Bosch, integrating the entire chain of R&D, adaptation, and mass production. Its customers include mainstream automakers such as Geely and Chery, with design wins for over 100 vehicle models supporting revenue growth.

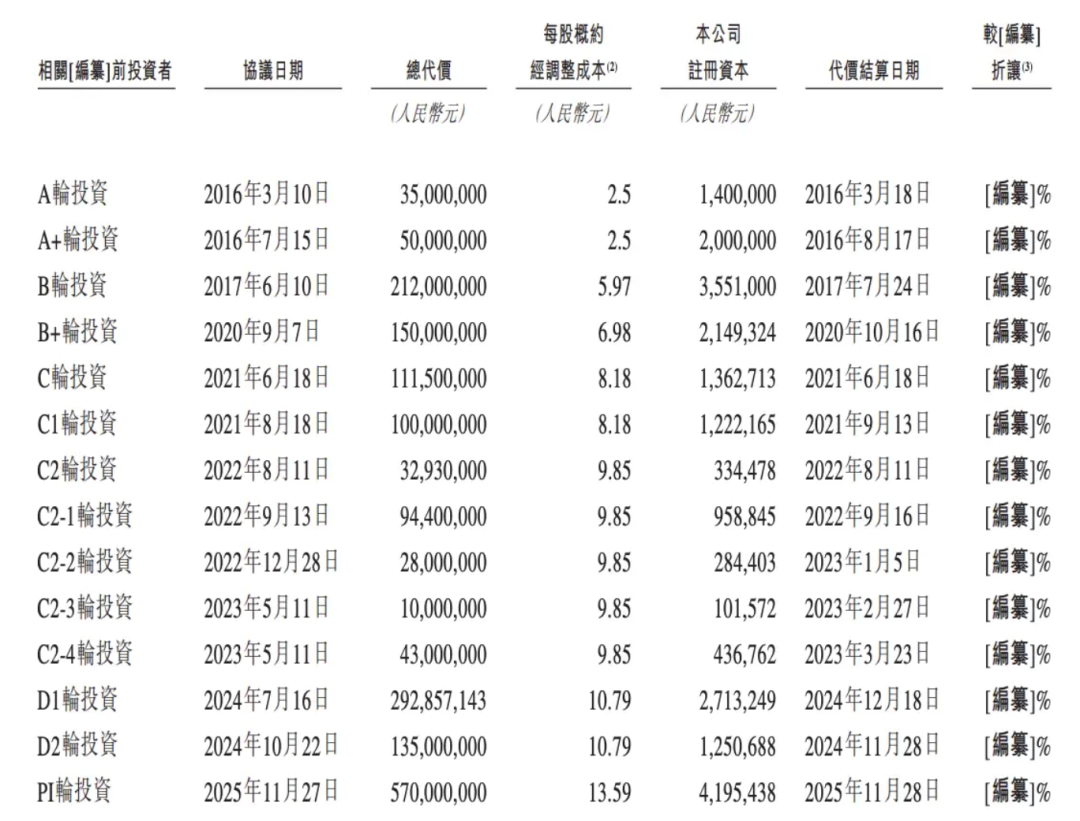

As such, Carlink has attracted significant attention in the primary capital market. According to its prospectus, since completing a 35 million yuan Series A financing in 2016, Carlink has rapidly advanced in the capital market, completing 14 rounds of financing totaling nearly 2 billion yuan as of November 27, 2025. It has attracted industrial giants such as NIO Capital and NavInfo, listed companies like Weifu High-Tech and Wenta Technology, as well as multiple investment platforms under the Wuxi State-Owned Assets Supervision and Administration Commission and renowned institutions such as Guoshou Chengda. After multiple rounds of financing and equity adjustments, Yang Hongze and the entities he controls, along with other concerted action persons, collectively hold 30.76% of the shares, forming the single largest shareholder group.

In particular, industrial investments from companies like Bosch have not only provided Carlink with capital but also given it a supply chain first-mover advantage. However, Carlink's over-reliance on Bosch has also trapped it in a single-supply chain dilemma.

In the first half of 2025, Carlink's net cash flow from operating activities was -335 million yuan, net cash flow from investing activities was 36.444 million yuan, and net cash flow from financing activities was 263 million yuan. Despite infusions from the primary capital market, Carlink's cash and equivalents still decreased by 35.836 million yuan, with ending cash and equivalents sliding to 150 million yuan.

For the years ending 2022, 2023, and 2024, and the six months ending June 30, 2025, the total remuneration for Carlink's directors was approximately 2.3 million yuan, 4.1 million yuan, 3.7 million yuan, and 1.1 million yuan, respectively. For the year ending December 31, 2025, the total expected remuneration for directors is approximately 3.9 million yuan. Despite continuous losses, Carlink's remuneration remains relatively stable.

Meanwhile, from 2022 to 2024, among Carlink's five highest-paid employees, four, three, and three were non-director employees, respectively. This means that during the reporting period, one to two directors consistently ranked among the highest-paid at Carlink, with their remuneration not adjusted according to company performance.

Deeply mired in losses and cash flow constraints, Carlink urgently needs capital inflows but faces the dilemma of its prospectus about to expire. Its HKEX listing application submitted in November 2025 is valid for six months. If it fails to complete the listing process as scheduled, the prospectus will expire, interrupting the listing process. Data from Tianyancha shows that since submitting its prospectus, Carlink has been unable to secure new financing. This exacerbates the situation for Carlink, which is eager to raise funds to alleviate cash flow issues and achieve shareholder exits. Reapplying will consume significant time and effort, potentially missing the best opportunity.

More critically, in its multiple rounds of financing, Carlink signed performance and listing gambling clauses with investors. The performance gambling requires cumulative net profits from 2023 to 2025 to exceed 210 million yuan, but the actual cumulative losses over the three years are certain to be negative, potentially triggering compensation.

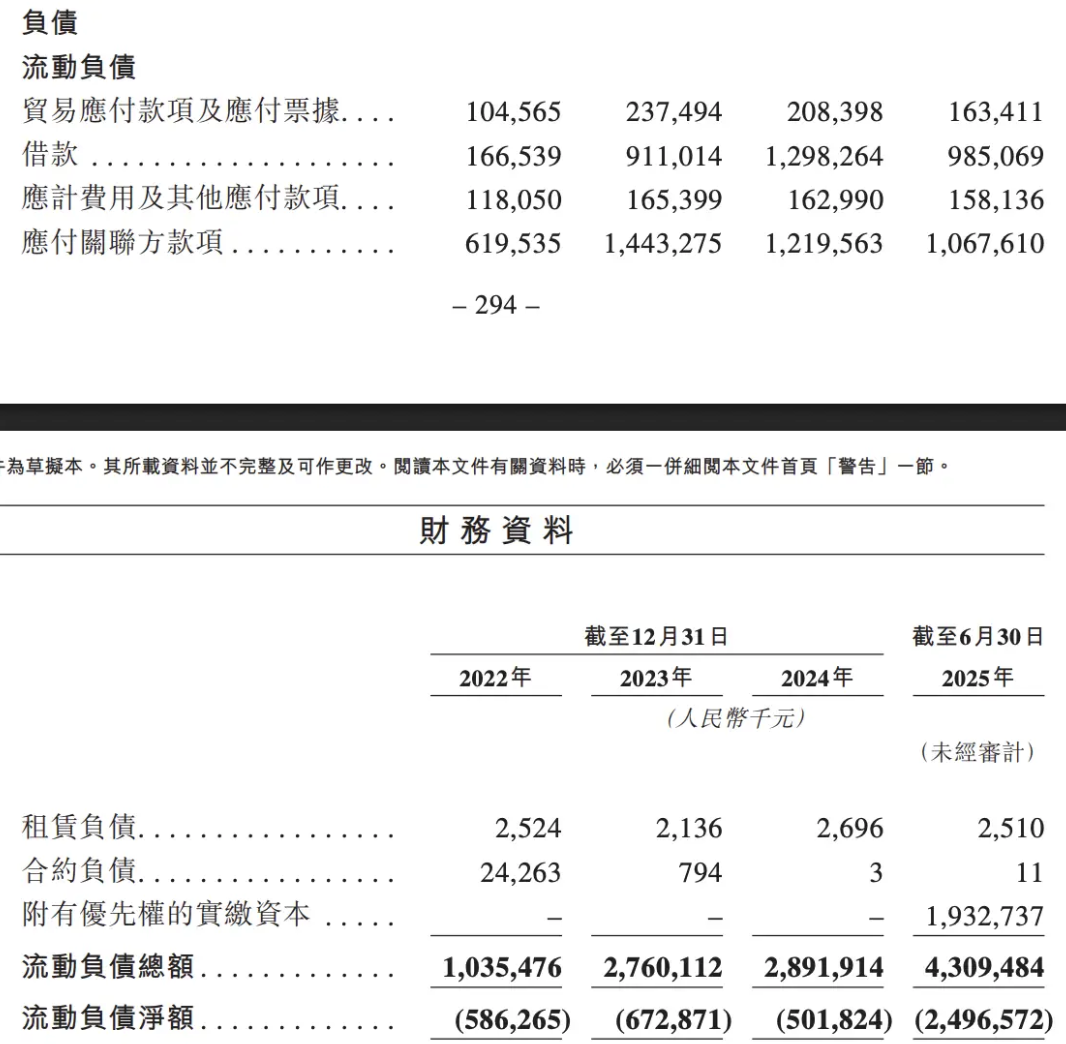

The listing gambling requires completing an HKEX IPO by December 31, 2026; otherwise, it must repurchase preferred shares at an 8% annualized return on the principal. As of 2025, Carlink's total current liabilities have soared to 4.309 billion yuan, a 49.00% increase from the end of 2024. Among them, paid-in capital with preferred rights amounts to 1.933 billion yuan. If it fails to list successfully, current liabilities will far exceed its current cash flow capacity, potentially crushing Carlink and damaging shareholder equity.

The key to safeguarding shareholder equity lies in Carlink's ability to list as scheduled, mitigate gambling risks, and improve operations. However, Carlink faces multiple dilemmas, making short-term listing and profitability difficult and introducing significant uncertainty in safeguarding shareholder equity.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry