Is a Price Collapse Imminent for Fuel Vehicles?

07/07 2026

07/07 2026

524

524

The Prelude to Their Decline?

With prices slashed to RMB 50,000 for a Sylphy, RMB 90,000 for a Civic, RMB 79,800 for a Sagitar, RMB 110,000 for an Accord, and even RMB 190,000 for a Range Rover Evoque, the past month has witnessed unprecedented price reductions in the fuel vehicle market. These once highly sought-after 'iconic models' have collectively triggered a historic price storm.

In May 2026, the domestic passenger vehicle market reached a significant milestone: not a single fuel-powered vehicle made it to the top ten best-sellers in retail sales. According to data from the China Passenger Car Association (CPCA), the retail penetration rate of New Energy Vehicles (NEVs) soared to a record 62.9% in May.

Fuel vehicles, impacted by factors such as rising fuel costs, saw their retail sales plummet in May, with monthly sales reaching just 560,000 units, a 39% year-on-year decline. Specifically, sales of Chinese brand fuel vehicles dropped by 39%, mainstream joint-venture brand fuel vehicles by 41%, and luxury brand fuel vehicles by 31%.

In the May sales rankings for fuel vehicles, the Geely Boyue L took the lead with 13,400 units sold. The previously dominant Nissan Sylphy fell to third place with 12,900 units sold. This classic model, which once boasted monthly sales exceeding 65,000 units, is now struggling to maintain its market position amidst the electrification wave.

The significant price reductions across several fuel vehicle models underscore this trend. After several rounds of price wars in recent years, has the pricing system for fuel vehicles truly collapsed?

Collective Price Plummet

In reality, these so-called 'plummeting prices' are often just marketing tactics employed by dealers. The actual 'net prices' are only achievable through a combination of discounts, including trade-in subsidies, national and local subsidies, and financing offers. Few buyers can qualify for all these discounts to secure the lowest price. Nevertheless, this pricing disorder has persisted for years, making it a harsh reality for fuel vehicles.

Latest data from Cui Dongshu, Secretary-General of the CPCA, reveals that from January to May 2026, 77 passenger vehicle models saw price reductions, including 32 conventional fuel vehicle models, an increase of 13 compared to the same period last year. The sales pressure on fuel vehicles is palpable.

In terms of price reduction intensity, fuel vehicles are also leading the pack. In May, the average price of newly reduced conventional fuel vehicle models was RMB 166,000, with an average price cut of RMB 25,000, representing a 14.9% decrease. In contrast, the average price of newly reduced models in the overall passenger vehicle market was RMB 202,000, with an average price reduction of RMB 22,000, a 10.8% decrease. Thus, fuel vehicle models have lower average prices but higher reduction rates.

In May, the comprehensive terminal promotion intensity for luxury fuel vehicles soared to 25.2%. Models and brands with traditionally stable pricing systems, such as the BMW X2 and Aston Martin, also offered discounts exceeding 20%. The price floor for high-end fuel vehicles has clearly been lowered.

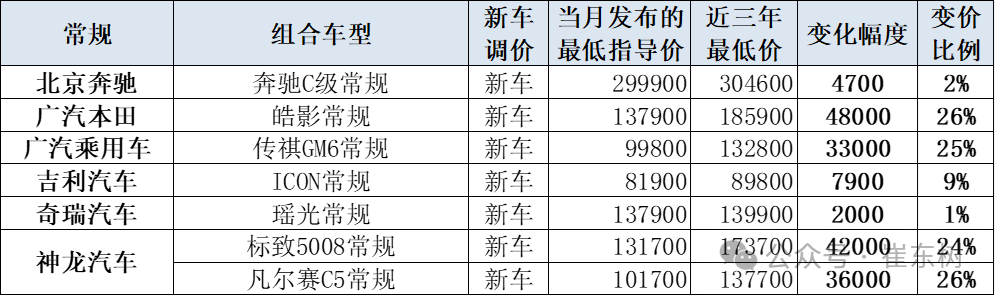

Additionally, Cui Dongshu noted that in May, no fuel vehicle models announced price reductions, but many new models directly undercut their original manufacturer's suggested retail prices (MSRPs). For example, the Breeze Shadow (Hao Ying), Trumpchi GM6, and Citroën C5 X all saw maximum MSRP reductions exceeding 25%.

Image Source: Cui Dongshu

The recently launched classic version of the Changan Eado slashed its price, offering a limited-time deal of just RMB 64,900. The limited-time starting price of the Cadillac CT5 plummeted to RMB 199,900.

Despite the pricing disorder in the fuel vehicle market, it seems premature to declare a price collapse. Data analysis indicates that the promotional trend for fuel vehicles remains within a controllable range.

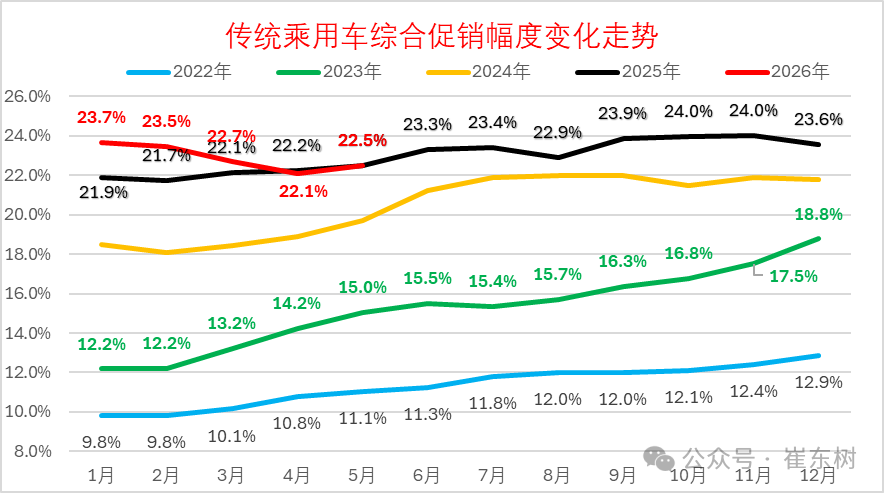

Cui Dongshu stated that promotions for traditional fuel vehicles began to increase slightly from September 2025, with moderate intensity. In 2026, due to significant price reductions, promotions gradually declined. In May, promotions for traditional fuel vehicles rebounded to 22.5%, up 0.4 percentage points from the previous month and remaining flat year-on-year. Fuel vehicle promotions have hovered around 23% for over a year.

Image Source: Cui Dongshu

Even luxury vehicles, which have intensified promotions since May, have seen limited changes in actual transaction prices due to significant MSRP reductions since the beginning of 2026. Promotions for joint-venture fuel vehicles gradually reached a low of 22.3% in May. However, due to particularly low new car prices, the overall promotional intensity remained relatively stable with a slight increase.

Given the current situation, it is more accurate to describe this as a comprehensive restructuring of the pricing system rather than a collapse. The accelerated 'dumping' of inventory vehicles reflects the direct reduction of MSRPs for an increasing number of new models, with significantly reduced premiums. This shift is driven by a combination of policies, technological advancements, and changing consumer psychology, marking a fundamental transformation in how vehicle value is defined in the domestic market.

The Failure of the 'Price-for-Volume' Strategy

Despite continuous price reductions, consumer enthusiasm for fuel vehicles remains unstirred.

The 'retreat' of fuel vehicles is neither as rapid as initially claimed by new energy brands nor as slow as anticipated by traditional brands. In May, fuel vehicles were absent from the top ten best-selling passenger vehicle models in the domestic market. Even when expanding the list to the top twenty, only four fuel vehicle models remained.

The market logic that 'no car is unsellable, only prices are insufficient, and lowering prices will surely boost sales' seems to have completely failed in 2026.

The rebound in sales volume and prices of fuel vehicles observed last year, with three consecutive months of positive growth from June to August, now appears to be a brief 'last hurrah.' Sales quickly declined again in September.

'The diminishing marginal returns of price wars are accelerating,' said Wang Xia, President of the Automotive Industry Committee of the China Council for the Promotion of International Trade, at the 2026 China Automotive Chongqing Forum. He presented a set of data: from January to May 2026, retail sales of passenger vehicles in China reached 7.1 million units, a nearly 20% year-on-year decline. The profit margin of the automotive industry in the first quarter was only 3.2%, significantly lower than the average of 4.9% for industrial enterprises above a designated size nationwide. During the same period, the operating income of the automotive manufacturing industryMB was R 2,412.8 billion, slightly lower year-on-year. China's automotive industry has experienced a rare triple decline in sales, revenue, and profits.

Dealers are bearing the brunt of price inversions. According to a report by the China Automobile Dealers Association, throughout 2025, 81.9% of dealers sold vehicles at prices below their purchase costs, with 51.5% experiencing price inversions exceeding 15%. The industry as a whole incurred losses accounting for 55.7% of dealers. Among traditional fuel vehicle brand dealers, only 25.6% were profitable, while 58.6% operated at a loss.

The immense pressure to meet sales targets has forced dealers to continuously reduce prices to increase sales volume, resulting in losses with each sale. Stopping sales would cut off manufacturer rebates, creating a vicious cycle over the past few years. Data shows that nearly 5,000 4S stores withdrew from the network in 2025, with an additional 1,200 stores closing in the first quarter of 2026.

Inventory pressure continues to mount. In May 2026, the comprehensive inventory coefficient for automobile dealers was 1.63, up 18.1% year-on-year and exceeding the warning level of 1.5. The inventory alert index stood at 57.9%, remaining above the 50% threshold for 47 consecutive months. Approximately 2.6 million vehicles are currently backlogged in dealerships nationwide, available for immediate delivery.

Faced with the current dilemma in the fuel vehicle market, traditional automakers are making every effort to remedy the situation. Currently, the two most typical 'lifesavers' are intelligent connectivity for both fuel and electric vehicles and HEV hybrid technology. To this end, joint-venture and luxury brands such as Volkswagen, BMW, Mercedes-Benz, and Audi have actively pursued more comprehensive local collaborations in recent years. By partnering with local technology companies, they aim to address shortcomings in intelligence and win back lost consumers. Meanwhile, Chinese brands have taken a different approach—extensively covering various market segments with plug-in hybrid models. In addition to attracting the last group of consumers who prefer fuel vehicles or still have long-distance travel needs, hybrid models can bypass overseas tariff barriers targeting pure electric vehicles, serving as a strategic vanguard for Chinese brands going global.

Although fuel vehicles, which have competed for over a century, are now 'past their prime,' they are far from exiting the market. From the perspective of the existing market, as of the end of 2025, the number of fuel vehicles in China reached 322 million units, accounting for nearly 90% of the total vehicle population. This vast existing fleet means that demand for fuel vehicles in areas such as maintenance, repairs, insurance, and the used car market will continue to exist for a considerable period.

This article is original to China Automotive News. Individual sharing is welcome. Media outlets must credit the author and source before reprinting. Any media or self-media creating video or audio content based on this article is strictly prohibited. Violators will bear legal responsibility.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models