First Half of Year Sees Auto Market Under Sales Pressure, New Energy Exports Offer a Glimmer of Hope

07/10 2026

07/10 2026

517

517

Robust production, strong exports, but sluggish domestic demand.

On July 9, the China Association of Automobile Manufacturers (CAAM) unveiled the automobile production and sales figures for June, along with a comprehensive summary for the first half of 2026. Despite the seemingly impressive numbers, there's an underlying market pressure.

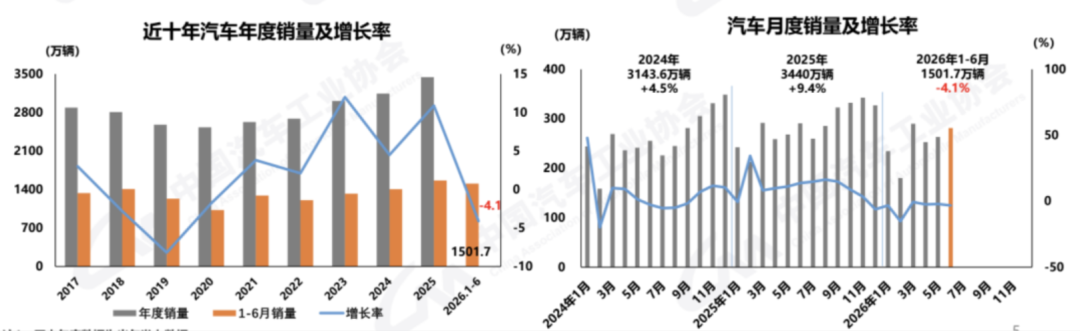

Specifically, in June, automobile production and sales hit 2.76 million and 2.81 million units, respectively, marking a 5.5% and 6.9% increase month-on-month, but a 1.2% and 3.2% decrease year-on-year.

For the first half of the year, automobile production and sales reached 14.993 million and 15.017 million units, respectively, down 4% and 4.1% year-on-year. The only silver lining was that the decline in June was narrower compared to the first five months.

Against the backdrop of sluggish global economic growth, China's auto market still leads in terms of scale. However, in terms of sales growth, it lags behind major markets like Europe, the United States, and Japan, which all saw slight growth in the first half of the year, largely due to policy incentives.

Of course, growth in overseas markets is also mirrored in the sales data. In the era of globalization, Chinese automakers have emerged as key players and contributors to the global automotive industry.

Divergence Between Domestic Demand and Exports

A closer look at the first-half sales data reveals sluggish domestic sales, with automakers frequently highlighting export figures in their sales promotions.

Data indicates that domestic automobile sales in the first half of the year totaled 9.921 million units, down 21.1% year-on-year, while exports soared to 5.096 million units, up 65.3% year-on-year, including 1.037 million units exported in June, up 75.1% year-on-year. The export market has become the "second growth curve" for China's auto industry, with growth far outpacing that of the domestic market.

Weak domestic demand has become the norm in the first half of the year.

The decline in domestic demand can be attributed to several factors. Policy shifts, coupled with intense competition in the auto market in the first half of the year, have led to a sales slump. After all, the auto market has long been a buyer's market. The launch of over 600 new models in the first half of the year has left consumers with an abundance of choices, leading many to adopt a wait-and-see attitude.

Especially under the influence of the ongoing price war over the past two years, waiting for discounts has become more crucial than early purchase benefits. After all, automakers have been aggressive in slashing prices to boost sales.

Amid rising international fuel prices, the phase-out of fuel vehicles has accelerated in the first half of the year. In June, retail sales of conventional fuel-powered passenger vehicles plummeted to only 600,000 units, down 39% year-on-year. Pure fuel vehicles declined by 42%, while conventional hybrid models fell by 7%. Fuel vehicles accounted for 82% of the overall decline in passenger vehicle sales for the month. The market share of conventional fuel vehicles dropped to 37.2% in June.

Of course, fuel vehicles are only declining in the domestic market; they still hold a significant share in exports. According to customs statistics, automobile exports in the first half of the year reached 3.083 million units, up 10.4% year-on-year, including 2.741 million fuel vehicle exports, up 32.7% year-on-year.

Especially during the transition of old and new production capacities, fuel vehicle exports have become an effective way for automakers to phase out fuel vehicle production capacity in an orderly manner. On the other hand, many joint-venture automakers experiencing declining domestic sales are leveraging China as an overseas export base, tapping into the global market with Chinese-made vehicles through China's comprehensive automotive industry chain.

Of course, rising fuel prices have also impacted the sales of extended-range and plug-in hybrid models to some extent. Extended-range models, which are closer to pure electric vehicles, have seen a significant sales decline in the first half of this year, becoming outdated.

From the perspective of the new energy market segment, pure electric vehicle sales in June surged by 26.9% year-on-year, while plug-in hybrid sales rose by 18.1%. Extended-range models, however, declined by 25.2% year-on-year. With technological advancements and improved charging networks, pure electric vehicles are accelerating the replacement of transitional technologies like extended-range models.

Meanwhile, the advantages of new energy vehicles are also evident in exports. Although fuel vehicles remain the mainstay of exports, the proportion of new energy vehicles continues to rise. From January to June, new energy vehicle exports reached 2.355 million units, up 1.2 times year-on-year. In June alone, new energy vehicle exports reached 523,000 units, up 17.2% month-on-month and 1.6 times year-on-year, with growth accelerating.

More importantly, in June, there was a significant milestone: new energy vehicle exports surpassed those of fuel vehicles, enabling China's auto exports to exceed 1 million units in a single month, driven by growing overseas demand for new energy vehicles.

The export of new energy vehicles has also, to some extent, alleviated domestic market fatigue, becoming a core channel for absorbing production capacity and offsetting weak domestic demand.

Accelerated Phase-Out of Fuel Vehicles

When domestic demand slows, trading price cuts for volume is no longer a sustainable strategy, especially given the negative impact of the price war, which has triggered internal changes in the auto market.

According to statistics, from January to June 2026, the average price of new energy vehicle models that reduced prices was RMB 247,000, with an average price cut of RMB 30,000, representing a 12% reduction. For the overall passenger vehicle market, the average price of models that reduced prices was RMB 240,000, with a 12.6% reduction.

However, this price-cutting trend is slowing down. In June, only seven models reduced prices, seven fewer than the same period last year. Cui Dongshu, Secretary-General of the China Passenger Car Association, stated that the market has remained relatively restrained from March to June this year, with brands that reduced prices performing strongly. The benefits of "trading price cuts for volume" are fading.

More importantly, upstream raw materials are quietly rising in price, driving changes in automakers' pricing. Especially with the combined impact of rising prices for power battery raw materials and chips, automakers' cost pressures have surged.

The spot price of battery-grade lithium carbonate has quickly risen to RMB 160,000 per ton. An automaker source revealed that fully absorbing the additional costs brought by new national standards would lead to a roughly 1.5 percentage point decline in gross profit margins.

Under such price adjustments, the auto market in the first half of the year presented the strange phenomenon of "price cuts in the first quarter and price hikes in the second quarter."

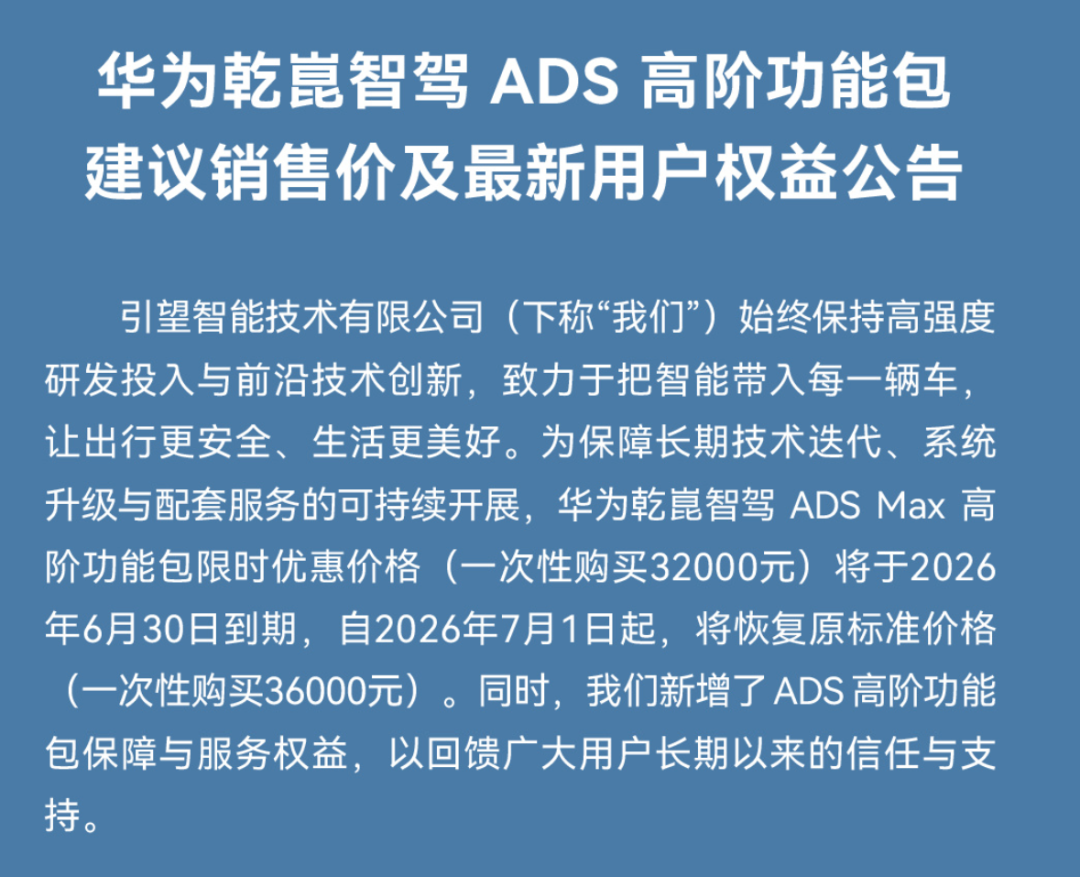

In terms of highly anticipated assisted driving, Huawei's Qiankun Intelligent Driving ADS Max advanced feature package resumed its standard price from July 1, after being offered at a discounted price. BYD's assisted driving system also adjusted its prices in 2026. Of course, these are strong automakers; those with weaker market influence may have to bear these costs themselves in the short term.

However, a general tightening of terminal discounts is expected to become the norm in the second half of the year. Automakers' pricing strategies will shift from "across-the-board price cuts" to "differentiated pricing," with some models raising prices to stop losses and others cutting prices to clear inventory.

Price changes continue to influence automakers' strategies. Most brands are shifting from "price wars" to "value wars." Institutional data shows that the net impact of price factors on car purchase decisions is only 3%, while technological factors account for as high as 20.7%. The competitive logic among automakers is shifting from price competition to technology, quality, and service competition.

In the second half of the year, technological premiums will become a new variable in the price structure. Differentiated features such as intelligent driving, fast-charging capabilities, and safety technologies will become core bases for pricing. The China Passenger Car Association believes that the new energy industry has transitioned from a policy-driven incubation period to a market-driven maturity phase, with "price-driven" growth giving way to "value-driven" growth.

June data shows that in the consumer markets for vehicles priced between RMB 200,000-300,000, RMB 300,000-400,000, and over RMB 400,000, retail sales of passenger vehicles from Chinese brands all exceeded 50%. High-end pure electric vehicles performed strongly, with B-class pure electric wholesale volumes reaching 295,000 units, up 37% year-on-year. The mid-to-high-end market is becoming a new growth pole, while low-end economy models and county-level markets have seen significant declines. In the second half of the year, the market for vehicles priced over RMB 400,000 still has potential.

The core contradiction in China's auto market in the first half of 2026 is the "structural imbalance amid overall growth"—exports and wholesale volumes are surging, while domestic retail demand has declined by more than 20%. The penetration rate of new energy vehicles has surpassed 60%, fuel vehicles are accelerating their exit, Chinese brands are taking full control, and joint-venture brands are continuing to shrink.

Of course, the decline in domestic demand is only a short-term issue. In the long run, China's auto market still has growth potential. On the one hand, there is room for further increase in the penetration rate of new energy vehicles. On the other hand, China's auto market has long been a mature market, with no significant changes expected in overall scale.

Morgan Stanley believes that with a concentrated launch of new models in August and September and continued policy support, China's auto market is expected to see a meaningful rebound.

For automakers, the second half of the year is both a critical window for boosting sales and a watershed moment for accelerated elimination.

Note: Images sourced from the internet. If there is any infringement, please contact us for removal.

-END-

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech

-

![]()

Optical Communication and Robot Vision: OFILM’s Bold Transformation Amid a 460 Million Yuan Loss

-

![]()

From 100,000-GPU Computing Might to Industrial Efficiency: The Logic Behind AI4S-Driven Intelligence

-

![]()

OpenAI, Grok, and Meta Release Three Major Models: Who is the King of Cost-Effectiveness?