Domestic EVs Lead, Overseas PHEVs Flourish

07/13 2026

07/13 2026

564

564

"Normalized Trends in the New Energy Vehicle Market"

Author | Gong Chenyan

Editor | Li Guozheng

Produced by | Bangning Studio (gbngzs)

"Seeking new energy vehicle export resources, with a focus on long-term, stable supply, especially PHEVs!"

This plea for assistance, posted on a social media platform on July 8, garnered nearly a hundred comments in less than three days. Half of the respondents were overseas agents representing mainstream automotive brands, while the other half were traders looking to break into the NEV export business, seeking advice or export resources in the comments.

Moreover, there has been a recent uptick in overseas individual consumers on social media seeking to directly purchase Chinese PHEVs, inquiring about purchase channels and methods for their desired models, reflecting robust overseas demand for Chinese PHEVs.

In stark contrast, Bangning Studio's recent visits to offline NEV stores revealed that multiple sales consultants reported a preference for EVs among customers visiting in the first half of the year, with orders for PHEVs and extended-range EVs on the decline.

On July 9, the China Association of Automobile Manufacturers (CAAM) released data indicating that vehicle export sales reached 1.037 million units in June, marking an 11.6% month-on-month increase and a 75.1% year-on-year surge, the first time monthly exports surpassed 1 million units. For the first half of the year, exports totaled 5.096 million units, up 65.3% year-on-year.

Notably, PHEV exports grew at a significantly faster rate than EV exports. In June, 309,000 battery electric vehicles (BEVs) were exported, up 15% month-on-month and 1.4 times year-on-year; 214,000 PHEVs were exported, up 20.5% month-on-month and 1.9 times year-on-year. From January to June, 1.433 million BEVs were exported, up 1.1 times year-on-year; 922,000 PHEVs were exported, up 1.4 times year-on-year.

In the domestic market, EV sales reached 4.987 million units in the first half of the year, up 13% year-on-year; PHEV sales reached 2.457 million units, down 2.5% year-on-year.

"This year, NEVs have shown a clear divergence in trends, with PHEVs and extended-range EVs faring much worse than EVs. Policy adjustments for scrappage updates and trade-ins have significantly impacted EVs, with A00-class EVs experiencing a sharp decline," said Cui Dongshu, Secretary-General of the China Passenger Car Association (CPCA). "Against this backdrop, it's remarkable that EVs have still achieved overall year-on-year growth."

CAAM stated that in the first half of the year, the Chinese auto market primarily exhibited three divergences: domestic demand faced significant pressure, while exports exceeded expectations and provided stable support; the passenger car market underperformed, while the commercial vehicle market continued to improve; the industry's新旧动能 (old and new growth drivers) continued to shift, with the traditional fuel vehicle market further shrinking and NEVs growing steadily.

▍01 PHEVs Shine as Export Stars

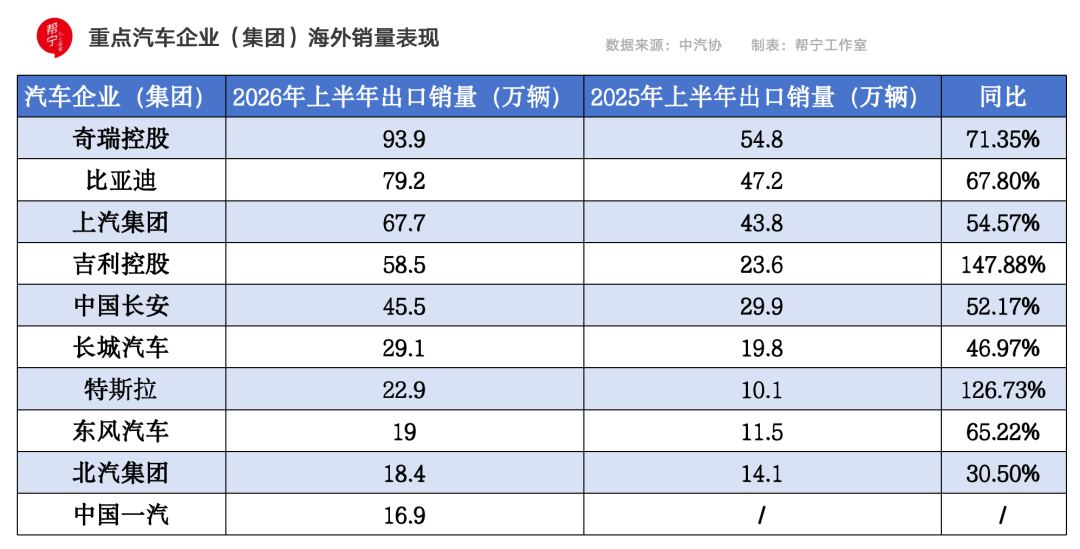

Among the top ten complete vehicle exporters in June, Chery exported 190,000 units, up 78.4% year-on-year, accounting for 18.3% of total exports.

Compared to the same period last year, Tesla's export growth was the most significant, reaching 36,000 units, up 2.6 times year-on-year.

From January to June, among the top ten complete vehicle exporters, Chery exported 939,000 units, up 71.3% year-on-year, accounting for 18.4% of total exports. Geely Holding Group saw the most significant export growth, reaching 585,000 units, up 1.5 times year-on-year.

In the first half of the year, four automakers surpassed 500,000 units in exports, compared to just Chery last year.

Whether it's BYD, Geely Holding Group, or SAIC Motor, an increasing number of automakers are relying on PHEVs as their main driver of overseas growth.

"Extended-range EVs are performing slightly weaker, while EVs and PHEVs are generally trending stronger, especially PHEVs, which have gained high recognition overseas," analyzed Cui Dongshu. "The domestic and international markets differ. Domestically, there isn't significant range anxiety, but overseas infrastructure lags behind China, where consumers must consider issues like charging stations. Thus, PHEVs perform stronger overseas."

Mainstream automakers have also adjusted their overseas product matrices accordingly, forming clear tiered strategies. For example, Chery leverages its global channels accumulated during the fuel era to focus on PHEV models as transitional products, with its Tiggo series PHEVs launching simultaneously in the Middle East, Brazil, and Southeast Asia, setting new monthly export records for four consecutive months in the first half of the year.

Geely adopts a multi-brand tiered strategy: Zeekr targets the high-end European BEV market, while Lynk & Co focuses on PHEVs to deepen its presence in the affordable family market in the Middle East and Southeast Asia.

BYD employs a dual-track strategy: launching the Dolphin and ATTO 3 BEVs in Europe while primarily promoting DM-i PHEVs in Southeast Asia and Oceania. In June, its overseas sales reached 175,300 units, accounting for 43.5% of its total sales, with overseas markets becoming a core growth driver for BYD.

Policy incentives released by various countries have further amplified the overseas advantages of PHEVs.

In mid-June, Colombia's Ministry of Trade, Industry, and Tourism issued a decree establishing a new regulatory framework for the production, import, and assembly of electric and hybrid vehicles. The decree sets up a conversion and assembly system applicable to plug-in hybrid electric vehicles, extended-range electric vehicles, BEVs, and full hybrids.

Under the new regulations, eligible companies can apply for quotas for importing complete NEVs, with 20,000 quotas set for 2026 and 2027, subject to a preferential tariff of 5%.

In Southeast Asia, Thailand introduced the EV3.5 incentive policy in 2025, offering a consumption tax as low as 5% for PHEVs with a pure electric range exceeding 80 kilometers.

According to the latest analysis article by the CPCA, the overseas market shows clear purchasing power tiering: mid-to-low-end BEVs rely on cost-effectiveness for volume, while high-end BEVs face lower market acceptance due to high prices and inconvenient charging; PHEVs cover the price range of RMB 100,000–250,000, balancing affordability and range anxiety-free travel, aligning with the consumption capacity of most developing countries and becoming a differentiated core competitiveness for Chinese automakers going global.

This means that the overseas popularity of PHEVs is not a short-term trend but a necessity during the global electrification transition. Before overseas charging infrastructure is complete, PHEVs will continue to serve as a bridge from fuel vehicles to EVs. Leveraging mature hybrid technology, Chinese automakers are continuously converting global traditional fuel vehicle users, with export growth set to continue.

▍02 EVs Reign Domestically

Domestically, the NEV market tells a different story: it has shifted toward EV dominance, with PHEVs and extended-range EVs facing sustained pressure, declining by double digits year-on-year in the first half of the year.

In June, sales of BEV passenger vehicles reached 685,000 units, up 3.6% year-on-year and 7.4% month-on-month; PHEV passenger vehicles reached 241,000 units, down 27.3% year-on-year and up 5.4% month-on-month; extended-range passenger vehicles reached 82,000 units, down 31.9% year-on-year and 3.8% month-on-month.

Some industry insiders believe that EVs will remain the long-term mainstream of NEVs, and even the industrialization of hydrogen energy will not shake their core position.

Currently, the domestic market has completed the transition from hybrid to direct EV adoption, supported by three fundamental changes: widespread charging infrastructure, declining battery costs, and technological advancements eliminating range anxiety.

This means that the improvement of the domestic charging network is eroding the range anxiety selling point that PHEVs and extended-range EVs rely on.

On social media, many PHEV and extended-range EV owners have posted that after purchasing their vehicles, they almost exclusively use electricity for daily commuting, leaving the fuel tank idle year-round, effectively paying extra for a redundant fuel system, making the cost-effectiveness of their vehicles significantly lower than that of EVs.

Battery prices are also continuing to decline, further narrowing the cost gap between EVs and PHEVs. In the mainstream RMB 100,000–150,000 family car market, EVs have become more competitive than PHEVs. Public data shows that by 2025, the average domestic battery price will drop by 28%, with a further 12% decline in the first half of 2026; lithium carbonate prices have fallen from a peak of RMB 600,000 per ton to RMB 100,000–160,000 per ton.

At similar price points, EV models clearly outperform other powertrains in range and configuration, delivering a significant advantage over PHEVs and extended-range EVs in terms of product strength.

As a result, EVs are gradually becoming the sales mainstay in various mainstream market segments.

From a sales perspective, B-class BEVs have become the growth core of their segment, with wholesale sales reaching 295,000 units in June, up 37% year-on-year. Models like the BYD Song and Tesla Model Y BEV versions continue to sell well, reflecting a significant trend of consumption upgrades, leading many families upgrading their vehicles to skip hybrids and choose EVs directly.

"The A-class and B-class segments are continuously transitioning from plug-in hybrids to BEVs. In the past, (consumers) couldn't afford BEVs, but now they are replacing (hybrids) as the mainstream," said Cui Dongshu. He noted that the domestic market has completed the popularization of electrification awareness, with the new generation of car buyers natively accepting EVs, making the long-term replacement trend irreversible.

On July 10, Qin Lihong, co-founder and president of NIO, predicted at a media briefing that the BEV share in the large five-seater SUV market will rise rapidly, with BEVs surpassing extended-range EVs by the end of this quarter, following a similar substitution path as seen in the large three-row SUV market.

Through the market evolution in the first half of the year, it's clear that the NEV industry is not undergoing a single technological route iteration but forming a differentiated landscape, with PHEVs fitting overseas markets and EVs iterating domestically. The two technological routes are leveraging their strengths in different markets and developing in a staggered manner. Perhaps this will be a long-term, normalized characteristic of China's NEV industry in the future.

-

![]()

Will Changan Mazda, Mired in Difficulties, Follow Skoda’s Path Out of China?

-

![]()

This Week in Home Appliances: Domestic Cool, Overseas Hot – Haier, Midea, Gree, Hisense Break Through; JD.com, TCL, Samsung, Vanward Drive Transformation

-

Seres Anticipates Over 2.2 Billion Yuan Loss in Q2, with Core Subsidiary AITO Automobile Projected to Lose 1.9-2.15 Billion Yuan

-

![]()

Breaking Through Barriers: Five Models for Chinese Automakers to Access Global Markets

-

![]()

Young Generation Trades Cars as Often as Smartphones! Average Age of New Energy Vehicles: Just 1.8 Years...

-

![]()

Musk Declares SpaceX Will Surpass the Combined Value of Everything on Earth! Is He Just Making Bold Claims? Online Debates Rage On…

-

![]()

The Most Terrifying Truth Behind GPT-5.6: AI Has Started to Self-Evolve

-

![]()

Is AI Still the Main Theme of the Market After the Decline of Memory Stocks?