Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

06/08 2026

06/08 2026

449

449

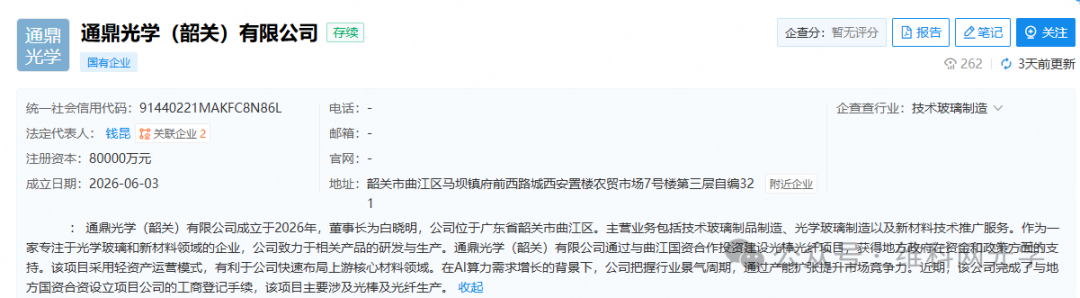

Recently, Tongding Optics (Shaoguan) Co., Ltd. (hereinafter referred to as "Tongding Optics") was officially established, boasting a registered capital of up to 800 million yuan. Its business scope encompasses the manufacturing of technical glass products, optical glass, optical fibers, optical cables, as well as the promotion of new material technologies.

Image source: Qichacha

The equity structure diagram reveals that Tongding Optics is a joint venture between Tongding Interconnect, an A-share listed company, and other shareholders. Behind Tongding Interconnect's decision to establish this new optical subsidiary lies a strategic industrial layout centered around the localization of optical fiber preforms and the company's pursuit of improved profitability.

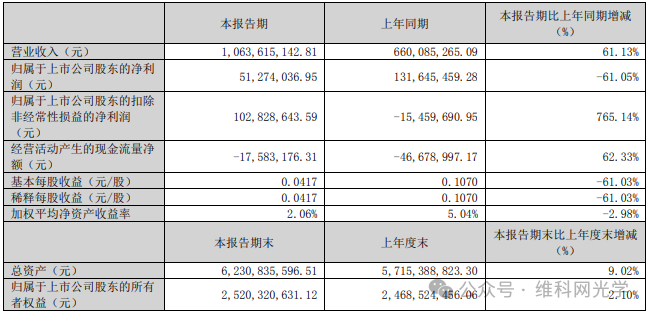

According to the 2025 annual report, Tongding Interconnect achieved a full-year revenue of 3.413 billion yuan, marking a year-on-year increase of 17.08%. However, its net profit attributable to the parent company suffered a loss of 76.3921 million yuan, representing a sharp year-on-year decline of 198.79%. In 2026, the trend of "increased revenue but decreased profit" seemed to persist at first glance: first-quarter revenue soared to 1.064 billion yuan, yet the net profit attributable to the parent company plummeted by 61.05% year-on-year to just 51.274 million yuan.

However, it's important to note that the net profit attributable to the parent company, excluding non-recurring items, reached 103 million yuan, a substantial year-on-year increase of 765.14%. This indicates a significant improvement in the profitability of the core business. The decline in net profit attributable to the parent company was primarily attributable to a high base of non-recurring gains in the same period last year, with significantly lower non-recurring gains this time around.

While revenue has shown robust growth, indicators of net profit attributable to the parent company have fluctuated, and sharp swings in the prices of core raw materials, such as upstream optical preforms, continue to exert pressure on gross margins. Optical fiber preforms constitute a substantial portion of optical fiber production costs, and their price fluctuations directly impact the company's profitability. Many companies with optical preform production capabilities have opted to use them in-house, leading to a persistent widening of the supply gap in the market.

Against this backdrop, Tongding Interconnect's long-standing reliance on externally purchased optical preforms faces challenges, making the move towards self-supply of upstream core materials a crucial strategic decision.

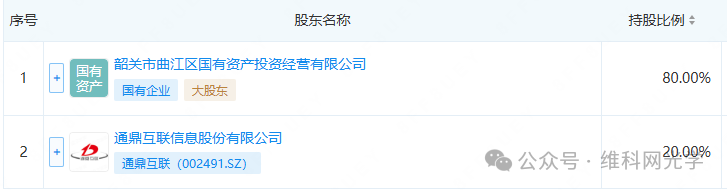

The establishment of Tongding Optics is a targeted response to this challenge. The project plans to construct facilities capable of producing 600 tons of optical fiber preforms and 20 million core kilometers of optical fiber annually, with a registered capital of 800 million yuan. Among this, Qujiang State-owned Assets has subscribed for 640 million yuan, holding an 80% stake; Tongding Interconnect has subscribed for 160 million yuan, holding a 20% stake. Additionally, the project company will secure bank financing of no more than 640 million yuan, with full joint and several liability guarantees provided by Tongding Interconnect and its controlling shareholder, Tongding Group.

Image source: Qichacha

It's worth noting that the project company serves primarily as a financing platform. Tongding Interconnect has separately invested 100 million yuan to establish a wholly-owned subsidiary, Tongding Information and Communication (Shaoguan) Co., Ltd., which will be responsible for the operation and management of the project after completion, operating independently and assuming its own profits and losses. The joint venture partners have also agreed that within five years from the establishment of the project company, Tongding Interconnect will gradually acquire all 80% of the equity held by Qujiang State-owned Assets.

This financial arrangement, characterized by "state-owned capital for construction, private enterprise for later-stage operation, and phased equity repurchase," enables Tongding to secure core assets with minimal cash outlay during the capacity ramp-up phase and fully acquire them once the project reaches maturity. Given the current significant financial pressure and incomplete profit recovery, this approach demonstrates both strategic foresight and financial prudence.

The choice of Shaoguan as the factory location is no accident. Shaoguan is a key area in Guangdong Province's plan to become a "smart computing city" and is accelerating the construction of data center clusters. It has developed the capacity to host 120,000 standard racks and 180,000 PFlops of smart computing power, along with 13 400G all-optical transport networks, making it the largest computing cluster in the Guangdong-Hong Kong-Macao Greater Bay Area.

The region has already attracted 36 upstream and downstream projects, including several data centers under construction, such as China Telecom's Phase II, and is expected to have a hosting capacity of over 260,000 standard racks by the end of 2026. For optical fiber and cable companies, Shaoguan's large data center clusters represent sustained local market demand and a predictable and stable sales outlet.

At the same time, Shaoguan's power and industrial infrastructure also provide favorable conditions for energy-intensive industries. The production of optical preforms and optical fibers is typically energy-intensive, and the relatively low electricity and hydrogen costs in the area are crucial for the long-term cost control of such manufacturing industries.

Overall, through the arrangement of "joint venture factory construction + state-owned capital-led," Tongding does not need to invest substantial capital at this stage while firmly grasping operational control and future exit paths. In this sense, the establishment of Tongding Optics is not just a physical expansion of production capacity but a precisely orchestrated strategic maneuver that highly aligns financial strategy with industrial logic.

Of course, capacity construction is never a quick process. The construction cycle for optical preform production lines typically ranges from 1.5 to 2 years, and the company will still need to bear cost pressures for some time before capacity is released.

Against the backdrop of increasingly prominent supply bottlenecks for optical preforms, Tongding Interconnect's strategic move to establish a presence in Shaoguan at this juncture is clearly a well-considered decision.

For this company, which has been operating in the optical communication sector for many years and seeking a way forward amid fluctuating performance in recent years, the future of Tongding Optics will serve as a litmus test for the viability of the breakthrough path of "seeking profits from the upstream sector."

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once