Despite a 225 Million Yuan Loss, Costar Continues to Ramp Up Investment in Automotive Optics!

07/06 2026

07/06 2026

427

427

Recently, Costar announced to the public that production and delivery across its various business sectors are proceeding in an orderly fashion. Existing orders are being scheduled for production as planned, and several new automotive and advanced optical products have commenced batch supply.

Furthermore, the company revealed that it has acquired the production technology for AR core component optical waveguide devices. This series of announcements came at a sensitive time when the controlling shareholder was planning a restructuring, prompting the market to closely examine the strategic direction of this seasoned enterprise.

As a core photonic defense enterprise under China South Industries Group Corporation, Costar possesses extensive expertise in special photonic technologies. Its product range encompasses low-light, infrared, and multi-spectral fusion technologies, which are widely applied in night vision sights, reconnaissance and surveillance, laser ranging, and photoelectric countermeasures for national defense equipment.

Regarding the statement "existing orders are being scheduled for production as planned," although it is not specifically directed at the defense sector, it encompasses all business segments, including defense. This directly addresses external concerns about the pace of military procurement and indicates that this fundamental business remains stable.

However, the timing of defense order placement and delivery cycles has always been contingent on the military's annual procurement plans, leading to inevitable periodic fluctuations. In its semi-annual performance forecast for 2025, the company stated that revenues from its main photonic defense products in the first half of the year fell short of expectations due to the characteristics of order placement and delivery rhythms.

Nevertheless, the forecast also highlighted that orders for optical components and assemblies increased year-on-year in the first half, with key new products achieving batch delivery. The current losses are a result of the phased pressure on defense revenues and the fact that new businesses are still in the process of ramping up production capacity and improving yield rates. Given the long-term trend of deepening national defense informatization, demand in the photonic defense sector remains robust. However, short-term performance flexibility will hinge on the follow-up order conversion situation.

While the defense fundamental business is operating smoothly, what truly piques the market's interest is Costar's strategic layout of a second growth curve in the automotive optics sector. The company established an automotive photonic display subsidiary in October 2024, specializing in head-up display (HUD) systems and PGU core modules, with design and manufacturing capabilities for a full range of W-HUD, AR-HUD, and P-HUD products.

In terms of business progress, automotive optics is showing signs of accelerated breakthroughs. Revenue from automotive photonic components and assemblies witnessed significant growth throughout 2024, and in the first quarter of 2025, the company secured multiple new project designations.

In the HUD segment, after securing an AR-HUD designation from a leading domestic brand in 2024, the company recently obtained a 3D-HUD designation from a joint-venture automaker. Automotive lens products have also entered batch supply, while optical components and parts are being steadily supplied to clients in the lidar and projection headlight sectors. However, objectively speaking, automotive optics is still in a typical phase of technical validation and designation introduction, and it will take time to transition from designations to scalable profitability.

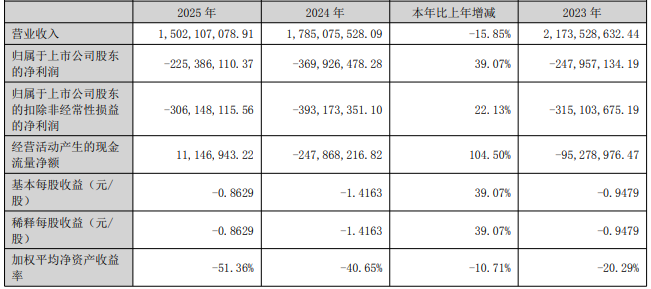

In contrast to the positive signals on the business front, Costar's financial fundamentals are still undergoing a challenging restoration process. The 2025 annual report showed that Costar achieved revenue of 1.502 billion yuan for the year, down 15.85% year-on-year, with a net loss attributable to shareholders of 225 million yuan, although this represented a 39.07% reduction in losses compared to the previous year. Net cash flow from operating activities turned positive at 11.1469 million yuan, indicating initial success in cost reduction, efficiency improvement, and product mix adjustment.

However, historical burdens remain significant. As of the end of 2025, consolidated undistributed profits stood at -473 million yuan, far exceeding one-third of the total paid-in capital. Monetary funds decreased compared to the previous year-end, while short-term borrowings remained high, making liquidity pressure a non-negligible concern. The company stated that it has sufficient bank credit facilities to cover maturing debts, but optimizing the financial structure will not happen overnight, and turning losses into profits remains the top priority.

In February of this year, the controlling shareholder announced plans for a restructuring. That same month, the company officially launched the "3040" critical leapfrogging project, covering ten major areas including product development, technological innovation, digital and intelligent upgrades, market expansion, and quality improvement and cost reduction. These initiatives aim to inject new strategic resources and governance vitality into the company but also add uncertainty at the operational level.

Looking at the entire optics industry, automotive optics has emerged as a core sector where various players are vying for position. Costar possesses inherent advantages, including its military technology heritage and precision optical processing capabilities, but also faces practical challenges such as long client introduction cycles and insufficient scale effects.

In summary, Costar is currently at a critical juncture where three major variables intersect: the stable operation of its defense business, the potential buildup in automotive optics, and the restructuring by its controlling shareholder. The company's statements on interactive platforms convey positive signals about orderly business progress, but it will take time for automotive optics to transition from designations to scalable profitability. Meanwhile, the unresolved losses exceeding 470 million yuan and high short-term debt underscore the urgency of turning losses into profits, compounded by the need to observe the strategic integration effects following the change in control.

For this seasoned enterprise carrying the legacy of military-grade optoelectronics, the key test for the market in the coming year will be how effectively it can convert its technological reserves into market competitive advantages and transform designated projects into tangible revenue and profits.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models