Zhipu AI's Time-Sensitive Pursuit of a Hong Kong IPO

12/22 2025

12/22 2025

615

615

Zhipu AI and MiniMax are locked in a time-sensitive race to go public in Hong Kong.

On December 17, 2025, Zhipu AI successfully cleared the listing hearing stage at the Hong Kong Stock Exchange. By a remarkable coincidence, MiniMax also received the green light for its listing on the same evening.

Data reveals that since its inception in 2019, Zhipu AI has secured over 15 rounds of financing, with its latest valuation soaring to RMB 40 billion. In 2025, MiniMax completed a substantial Series C funding round, raising nearly $300 million and achieving a post-investment valuation exceeding $4 billion (approximately RMB 30 billion).

The first company to go public and claim the title of Hong Kong's inaugural large-model stock stands to reap substantial dividends from the capital market. For Zhipu AI, a smooth IPO process could also position it as the "world's first publicly traded foundational large model."

The Rationale Behind Vying for Hong Kong's First Large-Model Stock Status

Zhipu AI's冲刺 (chōngcì, which here means "fierce push" or "determined effort") for a Hong Kong listing is not merely about securing the "world's first large-model stock" title. It signifies that, as the pioneer in this category, the company can draw increased attention from investors and command higher price-to-earnings and price-to-sales ratios. Zhipu AI's ambition to become Hong Kong's first large-model stock is underpinned by robust confidence.

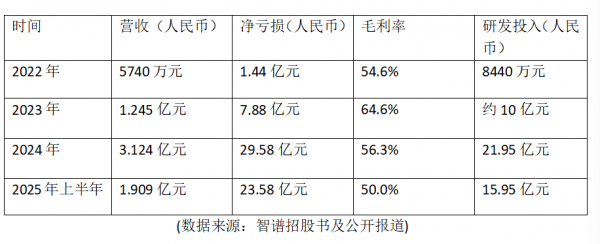

Firstly, this confidence stems from the impressive revenue growth generated by its AI large models. Despite the substantial early-stage costs of large-model development, with Zhipu AI reporting a net loss of RMB 2.958 billion in 2024 and RMB 2.358 billion in the first half of 2025, its R&D expenditures alone reached RMB 1.595 billion, more than eight times its revenue during the same period. Most of these funds were allocated to purchasing expensive computational resources (GPUs) and recruiting top-tier talent.

Nevertheless, Zhipu AI is experiencing rapid revenue growth, a factor highly prized by the capital market. From 2022 to 2024, its revenue surged from RMB 57.4 million to RMB 312.4 million, boasting a compound annual growth rate of 130%. It is anticipated that total revenue in 2025 will also witness a year-on-year increase exceeding 100%.

Secondly, Zhipu AI boasts an illustrious shareholder base. The company is backed by China's premier capital firms and internet technology giants, including Hillhouse Capital, Sequoia Capital, and Legend Capital, as well as internet behemoths such as Meituan, Tencent, Alibaba, Xiaomi, and Ant Group.

More impressively, it has also garnered investments from state-owned assets in Beijing, Shanghai, Hangzhou, Chengdu, and other regions, endowing Zhipu AI with a unique "national team" attribute. This provides a significant edge when competing for government and state-owned enterprise contracts.

Finally, Zhipu AI's business model is highly regarded by the capital market. The company is transitioning from a "capital-intensive" to an "asset-light" model.

Currently, Zhipu AI's primary revenue streams stem from localized deployments for governments (ToG) and large enterprises (ToB). However, this approach is resource-intensive, with a high gross margin of 50%, but it demands substantial human resources and faces challenges in achieving rapid scalability.

Nonetheless, Zhipu AI is pivoting towards an "asset-light" model, placing significant bets on MaaS (Model as a Service). This enables developers to access models on-demand through API interfaces, a model akin to OpenAI's, with the potential for exponential growth.

However, strong confidence does not guarantee a stress-free Hong Kong IPO or universal acclaim from the capital market for Zhipu AI.

The Hidden Forces Shaping Zhipu AI's Future

From a 2024 revenue perspective, Zhipu AI has indeed made remarkable strides, securing the top spot among China's independent general-purpose large-model developers with a 6.6% market share. Most notably, Zhipu's GLM architecture has achieved full domestic adaptation and is beginning to establish a presence in overseas markets such as Southeast Asia.

Nevertheless, Zhipu AI also confronts several hidden challenges.

One challenge is the uncertainty surrounding its bid for Hong Kong's first large-model stock title. MiniMax, another member of the "Six Little Tigers," is also diligently preparing for its Hong Kong IPO, with an anticipated listing in January 2026. This indicates that industry competition has evolved from purely technological rivalry to a "ranking race" in the capital market.

Another challenge is Zhipu AI's heavy reliance on computational resources, which poses multiple risks.

The first risk is the immense cost pressure. Currently, computational service fees account for over 70% of Zhipu AI's total R&D expenditures, which is not conducive to long-term R&D efforts. Zhipu needs to allocate more research funds to enhancing AI technology and attracting top talent, rather than spending on computational costs, to maintain its leading position in the AI large-model field.

The second risk is the significant supply chain vulnerability. As is widely recognized, the global supply of high-end chips is highly uncertain, particularly under U.S. chip sanctions, leading to a persistent shortage of domestic high-end AI chips. This directly impacts the survival and iteration of Zhipu AI's models.

The third risk is the uncertainty surrounding when profitability will be achieved, a point of great concern to the capital market. Although Zhipu AI's current revenue growth is relatively rapid, its expenditures are even more so, meaning that increased investment could lead to greater losses. When will it truly start generating profits? Clearly, the prospectus does not provide a definitive timeline for profitability.

Hong Kong IPO: China's Large-Model Industry Transitions from "Technological Competition" to "Capital Scrutiny"

This time around, whether it is Zhipu AI, MiniMax, or Yuezhi'anmian (Moonshot AI), which plans to follow suit with a Hong Kong IPO, their listings will signify China's large-model industry officially entering a new phase of "capital scrutiny" from "technological competition."

For companies, going public in Hong Kong enables them to raise substantial funds, significantly alleviating the current enormous R&D costs associated with large models. This is not merely an opportunity to "replenish" funds; it will also determine who can advance further in the costly race of AI large models in the future.

For the entire AI large-model industry, going public means that companies must begin to undergo regular performance evaluations. The era of relying solely on compelling narratives is over, and the ability to generate genuine profits and provide sustained investment returns to shareholders will become a more critical metric.

Zhipu AI is currently in a phase of massive capital expenditure, but it has also demonstrated to the outside world that AI large models can generate scalable revenue. However, following this Hong Kong listing, Zhipu AI will face even stricter "capital scrutiny," particularly regarding whether it can truly chart a path to sustained profitability.

-

![]()

Tencent Spearheads Manus Buyback: Unveiling the Strategy

-

![]()

Will Changan Mazda, Mired in Difficulties, Follow Skoda’s Path Out of China?

-

![]()

This Week in Home Appliances: Domestic Cool, Overseas Hot – Haier, Midea, Gree, Hisense Break Through; JD.com, TCL, Samsung, Vanward Drive Transformation

-

Seres Anticipates Over 2.2 Billion Yuan Loss in Q2, with Core Subsidiary AITO Automobile Projected to Lose 1.9-2.15 Billion Yuan

-

![]()

Breaking Through Barriers: Five Models for Chinese Automakers to Access Global Markets

-

![]()

Young Generation Trades Cars as Often as Smartphones! Average Age of New Energy Vehicles: Just 1.8 Years...

-

![]()

Musk Declares SpaceX Will Surpass the Combined Value of Everything on Earth! Is He Just Making Bold Claims? Online Debates Rage On…

-

![]()

The Most Terrifying Truth Behind GPT-5.6: AI Has Started to Self-Evolve