400 Billion Market Cap Reversal: The Twilight of the AI Four Little Dragons and the Dawn of New Large Model Contenders

04/28 2026

04/28 2026

474

474

The story of legacy AI has reached a dead end. The story of new AI is just beginning. The early frontrunners, the Four Little Dragons, have strayed off course and been left behind.

December 30, 2021, Central, Hong Kong.

Tang Xiaoo, founder of SenseTime, stood before the gong at the Hong Kong Stock Exchange, raising his wooden mallet. This was no ordinary IPO. Those present believed it marked a milestone for China's AI industry—the 'world's largest AI IPO.' On its debut day, SenseTime's market capitalization reached HK$137.5 billion.

At the same time, a 32-year-old made a starkly different decision.

Yan Junjie, then Vice President of SenseTime, Deputy Dean of the Research Institute, and CTO of the Smart City Business Group, submitted his resignation just before SenseTime's listing. While everyone expected him to stay with the soon-to-be-listed company and share in the glory of ringing the bell, he chose to leave.

The following spring, Yan founded MiniMax in Shanghai.

Four years later, on January 9, 2026, MiniMax went public on the Hong Kong Stock Exchange, with its market cap once surpassing HK$410 billion. Meanwhile, SenseTime's market cap had shrunk from over HK$300 billion at its peak to less than HK$80 billion.

The choice of a 'departing player' unexpectedly marked the dividing line between the old and new eras of China's AI industry.

Part.

01

Two Worlds

The 'AI Four Little Dragons,' represented by SenseTime and CloudWalk, and the new AI contenders represented by Minimax and Zhipu, are like two intersecting lines that diverge sharply after crossing.

The former 'AI Four Little Dragons' have reached a stage of stagnation and sluggish growth.

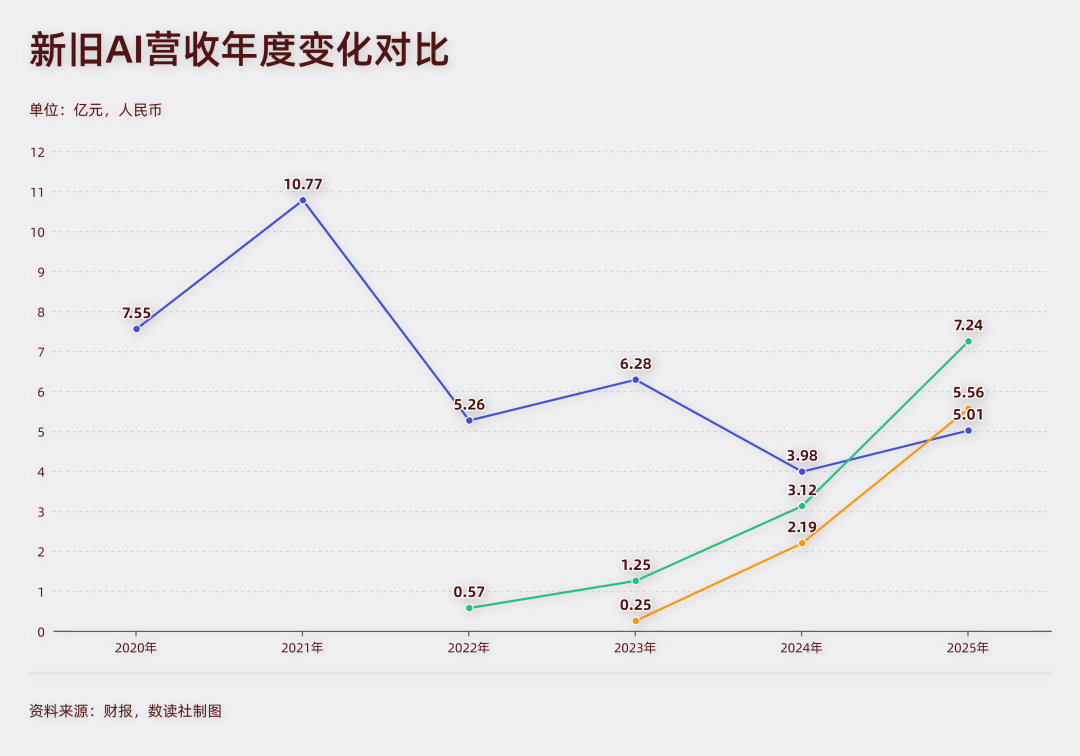

CloudWalk's revenue in 2024 was only RMB 398 million, a sharp decline of 36.69% year-on-year, hitting a new low since its listing. Losses widened to RMB 696 million, up 8.12% from 2023. While there was a recovery in 2025, with revenue reaching RMB 501 million, up 25.86% year-on-year, it was still only half of the peak in 2021.

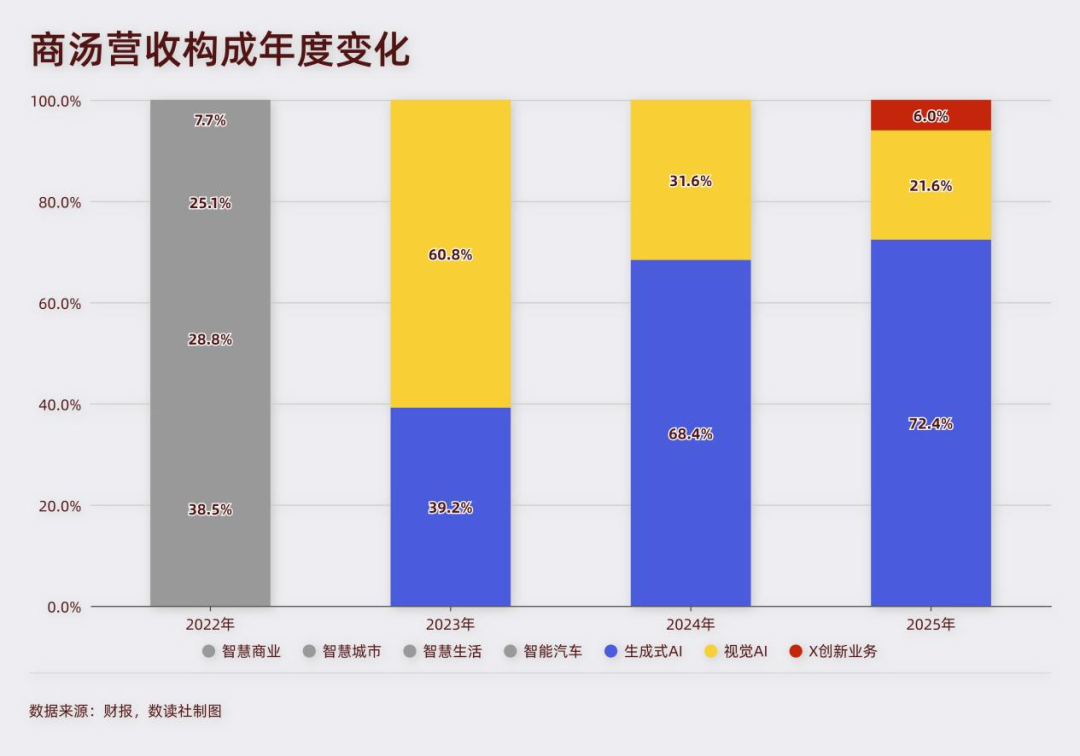

SenseTime's situation was slightly better. In 2025, its revenue exceeded RMB 5 billion for the first time, reaching RMB 5.015 billion, up 32.9% year-on-year, the fastest growth in three years. However, its core business had undergone a complete transformation. Once divided into smart business, smart cities, smart living, and smart automotive, these segments have now all disappeared from its financial reports.

Transformation or gradual decline—these are the choices currently facing the 'AI Four Little Dragons.'

In contrast, large model contenders like Zhipu AI and MiniMax are demonstrating high-growth models.

Zhipu AI achieved total revenue of RMB 724 million in 2025, up 131.9% year-on-year. Compared to its RMB 57.4 million revenue in 2022, its compound annual growth rate reached 132.78%.

MiniMax was even more remarkable, with revenue of only RMB 24.51 million in 2023, increasing to RMB 556 million in 2025, up 158.9% year-on-year. Its two-year compound annual growth rate reached 376.28%.

It took CloudWalk nearly a decade to achieve annual revenue of RMB 500 million, while MiniMax reached the same scale in just three years.

New AI contenders are experiencing rapid growth, with revenue doubling.

For the same AI technology, capital markets have assigned vastly different valuations. Since listing, Zhipu's stock price has surged 785%, while Minimax's has risen 420%. In contrast, SenseTime's stock has fallen 9%, and CloudWalk's has dropped 7%.

Zhipu and Minimax have market caps of HK$458.3 billion and HK$269.3 billion, respectively, compared to SenseTime's HK$80 billion and CloudWalk's mere HK$13.8 billion. The AI boom has brought no benefits to the Four Little Dragons.

The new AI contenders and the 'AI Four Little Dragons' now inhabit two entirely different worlds.

Part.

02

Platforms vs. 'Engineering Teams'

The root cause of all this lies in the dramatic transformation of business models in the AI world.

The early Four Little Dragons shared a common keyword: 'solutions,' primarily offering customized AI projects for enterprises or governments.

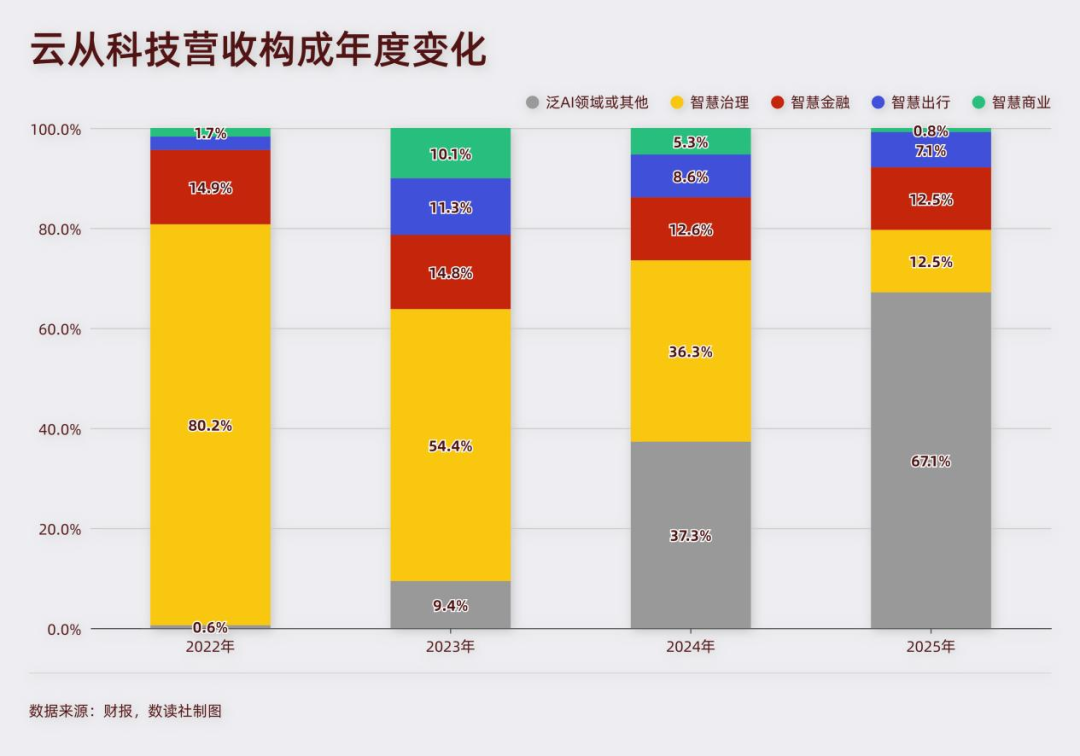

In the early revenue breakdowns of SenseTime and CloudWalk, items like 'smart cities' and 'smart security' were clearly listed, with government projects contributing the majority of revenue.

In CloudWalk's revenue structure, its four major smart businesses accounted for over 60% for a long time before 2025.

Customization involves non-standardized products, with the primary issue being high costs, low scalability, and weak profitability. Each client requires a fresh round of needs assessment, data labeling, model tuning, deployment, and maintenance, keeping marginal costs high.

In contrast, Zhipu and Minimax resemble standardized products, with 'open platforms' as a common keyword in their revenue structures. They provide technical services such as APIs and enterprise agents based on AI large model capabilities.

The 'new AI' adopts the 'MaaS (Model as a Service) + subscription' model, charging based on usage volume. The key to this model lies in metrics such as user numbers and paying users.

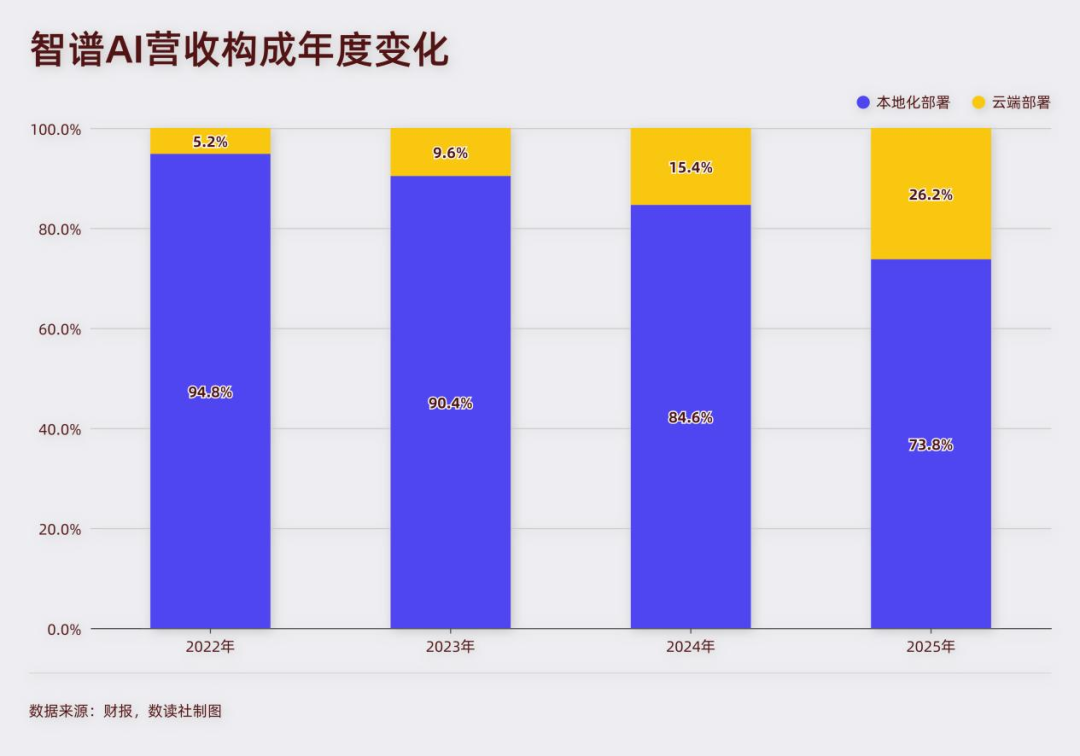

Zhipu's 2025 annual report shows that its revenue mainly comprises localized deployments and cloud deployments, accounting for 74% and 26%, respectively. It stated in its financial report that its MaaS platform's annualized recurring revenue (ARR) had surged 60-fold to RMB 1.7 billion, with registered users exceeding 4 million and paying developers reaching 242,000.

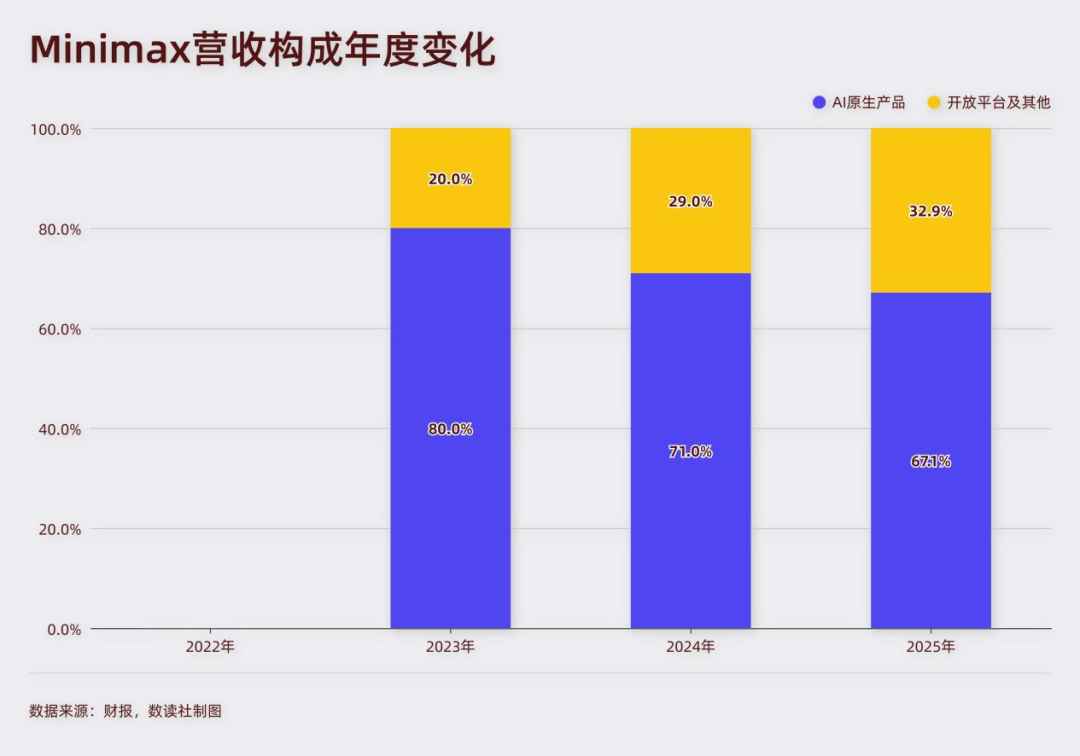

MiniMax's revenue consists of AI-native products (67.2%) and open platforms and others (32.8%). Its 'Xingye' AI application had accumulated 147 million users and 1.39 million paying users by the end of September 2025.

Legacy AI operates on a 'take one order, complete it, then find the next' engineering team model. New AI follows a 'build a platform, wait for users, train the model once, deploy it millions of times, greatly compress marginal costs, and earn more with more usage' approach.

These differing models have led to vastly different growth rates. The consumer-driven model mirrors the user growth curves of internet products, with far greater explosive potential than B2B customized projects.

The emergence of OpenClaw has amplified the power of the new AI logic.

Data from the OpenRouter platform shows that from March 16 to 22, 2026, the weekly usage volume of China's AI large models reached 7.359 trillion Tokens, up 56.9% month-on-month.

New AI players are the biggest beneficiaries in this landscape.

Part.

03

Heavy 'Strategic Burdens'

Faced with growth ceilings and rigid models, legacy AI companies must correct their course.

SenseTime is striving to catch up. In 2025, its generative AI business revenue reached RMB 3.63 billion, up 51% year-on-year, with its share of total revenue rising from 63.7% in 2024 to 72.4%.

SenseTime launched the 'Everday New V6.5' model, which it claimed ranked first domestically with a score of 75.35 in the SuperCLUE multimodal visual language model evaluation, leading in seven subtasks domestically.

However, a major obstacle to transformation lies in the heavy 'strategic burdens.'

First, existing technological accumulations do not align with current large model technology iterations and are even outdated. The technological foundations of the Four Little Dragons were built on computer vision: facial recognition, image classification, and video analysis. This technological framework was marginalized after the emergence of ChatGPT and pales in comparison to the Token-driven economic engine brought by OpenClaw.

Second, legacy AI companies struggle to keep pace in the race for large model capabilities. In early 2025, DeepSeek rose to prominence, while domestic brands like Qwen, GLM, and Kimi frequently appeared on international large model rankings. This is an arms race centered on 'parameter scale, reasoning ability, and multimodal fusion,' rather than the 'algorithm precision and engineering implementation' competitions of the visual recognition era.

Reflected in financial reports, MiniMax's AI-native products saw average MAU grow from 3.14 million in 2023 to 27.64 million in the first three quarters of 2025, serving over 236 million users in total. Meanwhile, the consumer-facing products of CloudWalk, Megvii, and Yitu have barely entered the mainstream consumer market.

Additionally, compared to the all-in commitment of new AI players, legacy AI companies must consider performance, allocate resources to traditional businesses, and account for capital market reactions, facing numerous constraints.

While SenseTime's transformation has shown initial success, compared to 'large model-native' companies like Zhipu and MiniMax, it must maintain a massive visual AI business volume and absorb a research and development team of thousands, all while facing persistent profitability pressures as a listed company.

Compared to the Four Little Dragons, new AI players like Zhipu and Minimax are more willing to incur losses. Zhipu's net loss reached RMB 4.718 billion in 2025, up 59.5% year-on-year, while MiniMax's annual loss widened to RMB 13.16 billion, up over 300% year-on-year.

In contrast, CloudWalk's loss narrowed to RMB 545 million in 2025, and SenseTime's net loss shrank significantly by 58.6% year-on-year to RMB 1.782 billion.

The primary reason is that legacy AI companies already carry heavy historical burdens. Since 2018, SenseTime's cumulative losses have still exceeded RMB 30 billion, while CloudWalk's cumulative losses have reached RMB 5.1 billion.

New AI companies start with a clean slate, building teams and products around large model architectures from day one, resulting in unparalleled decision-making efficiency and technological iteration speed.

SenseTime is the fastest among the Four Little Dragons to pivot. With generative AI accounting for over 70% of its business, its EBITDA turned positive for the first time, and its operating cash flow turned positive for the first time since listing. These signs indicate that SenseTime is struggling to emerge from the quagmire of 'legacy AI' and transition toward 'new AI.'

However, the other three Little Dragons are still struggling: CloudWalk is caught between RMB 500 million in revenue and RMB 600 million in losses, Megvii has withdrawn its IPO and is wandering in 'strategic adjustments,' and Yitu has nearly faded into obscurity amid the large model wave.

Their stories represent a ruthless reshuffling of China's AI industry from 'Version 1.0' to 'Version 2.0': early starters do not necessarily win, and choosing the wrong path means being left far behind by latecomers.

The challenges for new AI have only just begun.

Behind high valuations and rapid growth lies even more staggering losses. Who can be the first to reach profitability in this 'burn money for market share' game remains unknown.

The story of legacy AI has reached a dead end. The story of new AI is just beginning. The early frontrunners, the Four Little Dragons, have strayed off course and been left behind.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?