MiniMax Price Adjustment Sparks Public Outcry: Is the $300 Billion Market Cap Myth at Risk?

06/11 2026

06/11 2026

441

441

The sudden introduction of a new large model and escalating computing costs have led to an unexpected price adjustment, plunging Hong Kong-listed AI sensation MiniMax into a public relations crisis.

Several days ago, MiniMax, a rising star in the large model sector that saw its market valuation surge past HK$300 billion just a month earlier, abruptly shifted from a per-use billing model to a Token-based billing system. The Starter package price soared from HK$29/month to HK$49/month without prior notification to users.

The outcome was predictable. A significant number of users only discovered the billing rule change upon logging in. Under the new system, Token consumption for the same tasks significantly exceeded expectations, with monthly allowances being depleted in days. One developer calculated that while 3 to 5 billion Tokens previously cost HK$49 per month, the same quantity now costs around HK$175—a staggering 257% increase.

What infuriated many users even further was the perceived double standard in API pricing between Chinese and international users. For input under 512K, the domestic price is HK$2.1 per million Tokens, while the international price is just US$0.3 per million Tokens (approximately HK$2.04). Isn't this blatant discrimination?

Faced with a torrent of complaints, MiniMax's parent company, Xiru Technology, issued an emergency apology on the evening of June 2.

The company acknowledged that "this adjustment failed to adequately communicate in advance with everyone and thoroughly explain the changes to the M3 Token Plan billing and package options. Our execution fell short, and our handling of issues such as weekly limits for existing users was inadequate."

The official explanation was that M3, being a larger and more capable model with a 1M context window, demands significantly more computing resources. In simpler terms, the original package model could no longer effectively manage computing costs in the era of AI agents.

In response to market sentiment, the company subsequently offered a compensation package: existing users retained their unlimited weekly allowance privileges, new users received a 50% bonus on their allowance, and usage allowances were uniformly reset for the period from June 1 to June 7.

Behind the Glittering Performance on the Stock Exchange

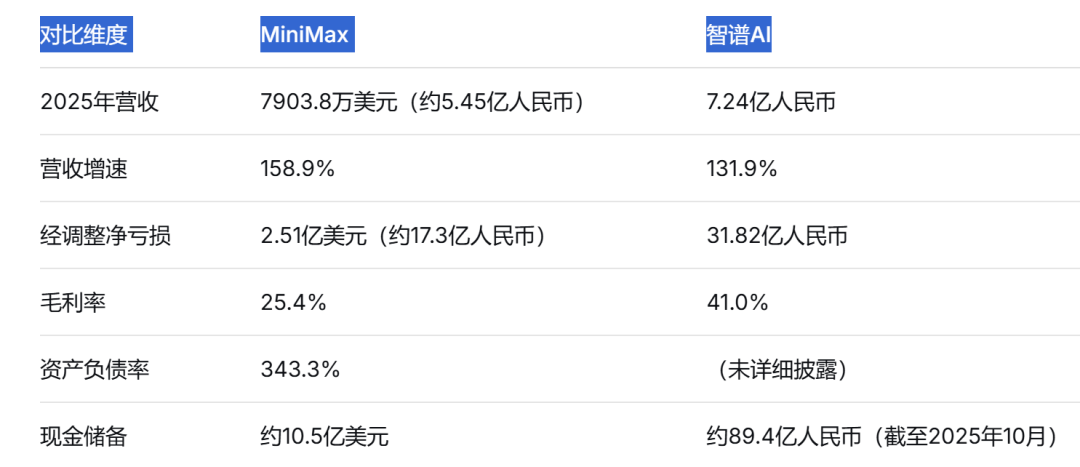

If we focus solely on MiniMax's revenue growth, it indeed resembles a star company. In 2025, revenue reached US$79.038 million, up 158.9% year-on-year; gross profit surged from US$3.738 million in 2024 to US$20.079 million, a 437.2% increase; and the gross margin improved from 12.2% to 25.4%.

The stock price once soared to HK$1,330, a sevenfold increase from the issue price of HK$165, pushing the market cap past HK$300 billion. The company also recently announced plans to list on the A-share market, aiming to join Zhipu on the Science and Technology Innovation Board.

However, a closer examination of the financial statements reveals three issues worthy of attention behind these impressive figures.

Revenue soars, but losses soar even higher. In 2025, the net profit attributable to the parent company was a loss of US$1.872 billion, approximately RMB 12.9 billion, more than tripling year-on-year. From 2022 to 2025, cumulative losses reached US$2.698 billion, nearly US$2.7 billion. A simple calculation reveals: for every US$1 earned, US$3.17 was lost.

Data source: 2025 annual reports and prospectuses of various companies

Over 70% of revenue comes from "virtual companions" targeting foreign users. A look at the prospectus reveals that over 70% of MiniMax's revenue comes from overseas markets, primarily from the AI virtual companion app Talkie (Xingye).

As of the third quarter of 2025, cumulative individual users reached 212 million, with 27.6 million monthly active users. Paid users surged from fewer than 120,000 at the end of 2023 to 1.77 million.

But the problem is, no matter how popular virtual socializing becomes, it cannot change the fact that the gross margin for the company's C-end AI-native products was just 4.7% in the first three quarters of 2025. Isn't this akin to "charity"? Meanwhile, B-end enterprise services accounted for only 32.8% of total revenue.

Using the most easily monetizable "dopamine economy" to fund the extremely expensive development of foundational models—is this path a shortcut to AGI, or a dangerous game of "subsidizing ideals with quick money"?

A 343% asset-liability ratio and profligate spending. R&D expenditure reached US$253 million, up 33.8% year-on-year. Net cash outflow from operating activities was US$280 million. CCB International estimates that MiniMax burns through approximately US$28.1 million in cash each month.

The market's reaction was telling. After the news broke, the stock price fell more than 20% in two days, and the market cap halved from its peak of HK$300 billion to HK$1,417.

The market is no longer buying the story of funding AGI through foreign users' in-app purchases.

The Harsh Reality of the Large Model Price War: Giants Compete on Ecosystems, Startups Struggle to Survive

In May 2024, ByteDance ignited the price war. The Doubao Pro model was priced at US$0.0008 per thousand Tokens, 99.3% lower than the industry average. Alibaba Cloud soon followed by slashing prices for its main model, Tongyi Qianwen, by 97%. Baidu made its two main Wenxin large models completely free, while Tencent reduced prices for its Hunyuan large model by up to 87.5%.

By 2025, DeepSeek-V2 had driven prices down to 1% of GPT-4's, and DeepSeek-R1 pushed the envelope to the brink of "zero cost."

Why are the tech giants so bold? Because they're not calculating based on single API calls but on ecosystem value. Alibaba Cloud uses AI models to retain cloud computing clients, ByteDance integrates AI into Douyin and Feishu, and Tencent subsidizes its AI business with cash flow from WeChat, QQ, and games. For these giants, AI is infrastructure, not a profit center—a strategic layout they can afford to lose money on.

But what about independent startups?

Without external funding or an ecosystem moat, they have no choice but to weather the price war.

Even more awkwardly, while MiniMax was struggling to digest the backlash from its price adjustment, its archrival Zhipu was moving in the opposite direction, thriving. Zhipu raised API call prices by 83% against the trend, with its MaaS platform's annual recurring revenue (ARR) reaching approximately RMB 1.7 billion, a 60-fold increase in 12 months.

The contrast between the two sides is striking.

Data source: Prospectuses and public financing information of various companies

Additionally, the company's move to "return to A-shares" has also drawn attention.

On May 29, information disclosed on the China Securities Regulatory Commission's website showed that MiniMax had signed an IPO counseling agreement with CITIC Securities, officially initiating the process to list on the A-share Science and Technology Innovation Board.

The market is concerned that this signals the company's urgent need for funds. This topic will be explored in a dedicated feature another day and will not be expanded upon here.

Behind the Price Adjustment Controversy

In my view, this price adjustment controversy is not merely a "communication issue" but a trust crisis for the entire industry.

While the controversy can certainly be attributed to MiniMax's "inadequate communication," a deeper reason lies in the industry-wide anxiety over computing costs devouring all profits.

Industry insiders point out that the computing-powered economic model in the AI era has brought forth entirely new consumer trust issues, necessitating the rapid establishment of a consumer rights protection framework.

As large models transition from "free trials" to "pay-per-Token" models, companies must confront a fundamental question: How can they convince users that their billing rules are fair and transparent?

Kimi previously faced a wave of concentrated complaints due to similar billing adjustments. This is not just an operational mishap for one company but a warning signal for the entire industry.

From the user's perspective, MiniMax's apology and compensation package demonstrate sincerity. Users who purchased packages before March 22 and enjoyed unlimited weekly allowances will retain that privilege; users who purchased during the period will receive a permanent 50% bonus on their weekly allowance; usage allowances will be uniformly reset, and allowances for the first week will be doubled.

But simply offering coupons cannot resolve the fundamental issues with the business model.

Don't Just Focus on the Plummeting Market Cap—the Industry's Value Has Only Just Begun

Many people, seeing MiniMax's stock price collapse, immediately conclude that "another bubble has burst." But I believe this judgment is overly simplistic.

The AI large model sector is moving away from the initial "hundred-model battle" in 2023 to the "price war" of 2025. In 2025, China's large model market was worth approximately RMB 220 billion, with growth exceeding 150%. According to a Frost & Sullivan report, Alibaba Cloud and Baidu Intelligent Cloud together accounted for over 50% of the domestic AI cloud market share. The industry is indeed consolidating, but that doesn't mean the story is over.

While MiniMax's narrative has been overshadowed by the price adjustment controversy, it still holds strong cards—accumulating 212 million users across over 200 countries, with its video generation tool, Hailuo AI, achieving global popularity and its voice model once surpassing ElevenLabs to top the charts.

If it can truly convert C-end traffic into B-end clients and transition from "dopamine-driven business" to "productivity tools," the situation could change entirely.

As Zhipu CEO Zhang Peng said, APIs represent a model for transforming AI infrastructure capabilities into resources for economic operations. "The quality of intelligence creates pricing power, and deep usage by enterprises and users drives scalable growth." The real barrier lies not in price but in whether users are willing to pay for superior capabilities.

For MiniMax, the price adjustment controversy serves as a loud wake-up call.

But for the industry as a whole, these "growing pains" are pushing all companies to move away from the wild growth of "acquiring traffic through subsidies" toward the right path of "earning trust through value."

Users' anger is real, but it points not to a rejection of AI but to an expectation for more transparent, fair, and sustainable business models.

The temporary fluctuations of a HK$300 billion market cap will not alter the industry's forward trajectory.

For the new generation of AI tech companies, if you cannot quickly prove your profit-generating capabilities in the enterprise market, your API pricing power, and customer loyalty, then no matter how eye-catching your C-end products are, your stock price will eventually collapse under the harsh scrutiny of the capital markets.

Disclaimer: This article is solely a financial hotspot analysis, citing publicly available data, company announcements, and Tonghuashun IFinD. The views expressed are for reference only and do not constitute any investment or consumption advice.

What are your thoughts on the MiniMax price adjustment controversy?

We welcome your civil and rational insights in the comments section.

Disclaimer: Our team has been deeply engaged in financial and tech media for 13 years, focusing on in-depth interpretations of capital markets, listed companies, and the latest trends in business and technology. With over 3 million followers across platforms, we welcome submissions and will pay fees for adopted content. For copyright issues related to cited articles or images, please contact our administrators, who will promptly correct attributions, pay fees, or remove content upon verification.

-

![]()

From Hardware to AI: Has the Intense Competition in Smartphone Imaging Reached Its Limit?

-

![]()

Mired in Pricing Controversy and Stock Price Slump: What Ails MiniMax?

-

![]()

DJI and Insta360 Release 'Cinematic Cameras': Can Pocket Stabilizer Cameras Truly Make It onto Professional Film Sets?

-

![]()

AISpeech's IPO Journey: Valuation Soars by RMB 2 Billion in a Month, Alibaba Trims Stake for RMB 280 Million Gain, Short-Term Debt Deficit Hits RMB 168 Million

-

![]()

DingTalk: At a Crossroads

-

![]()

Uber Exhausts Annual AI Budget in Just Four Months: Why Even Uber Can’t Sustain Token Costs?

-

![]()

"Explosive Risks" in the Trunk: The Unauthorized Battery Modifications in New Energy Vehicles Fuel a Shadowy Industry

-

![]()

From Deep Ties to Strategic Divestment: Is Chery Reevaluating Its Stake in This Industry Leader?