From Hardware to AI: Has the Intense Competition in Smartphone Imaging Reached Its Limit?

06/11 2026

06/11 2026

371

371

By | Xiaofeng

Source | Bowang Finance

With hundreds of millions of pixels, blockbuster-level shooting capabilities, and ultra-wide-angle lenses with tens of millions of pixels... Can imaging in the smartphone realm still be a reason for you to buy?

Many people experience a conflict when choosing a smartphone. They compare the imaging capabilities and shooting effects of different brands and models, yet feel that the performance parameters of these cameras, big or small, seem quite similar.

However, strong subjective opinions persist on which brand or model offers clearer and more visually appealing photos. Every brand has its loyal fan base.

Yet, this does not deter smartphone manufacturers from engaging in fierce competition and intensification in the imaging sector.

During the summer 2026 product cycle for new smartphones, the mid-range price segment of 2,000 to 4,000 yuan was crowded with iterative models from four major brands. The Huawei nova 16, Honor 600, OPPO Reno 16, and vivo S60 were launched one after another, all implicitly betting on imaging hardware and AI shooting capabilities.

Manufacturers continue to introduce flagship imaging sensors to lower-tier models and enhance AI computational photography. However, consumers are increasingly less swayed by camera specifications when deciding to upgrade their devices. The deeper the intensification in the imaging sector, the faster manufacturers' profit margins shrink.

Despite this, imaging alone is struggling to stimulate new demand for device upgrades or purchasing desires.

01 The Fierce Battle in Imaging

Competition in imaging was not so intense more than a decade ago. Photography and beauty features were often sufficient to provide a competitive edge. However, everything has changed now. Compared to features like gaming, cooling, drop resistance, refresh rates, and signal strength, the practicality and appeal of photography have become more prominent.

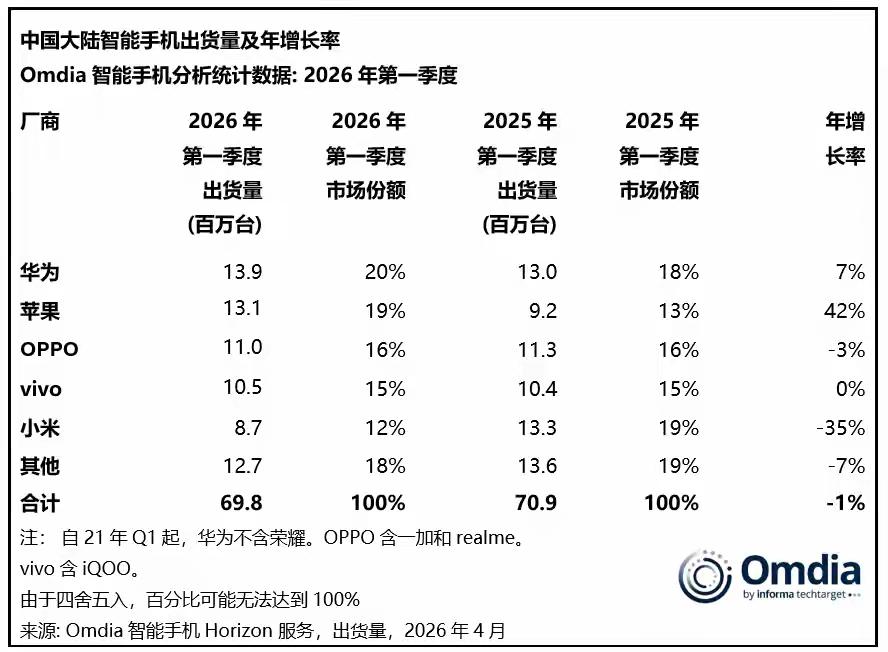

In the first quarter of the year, there were significant disparities in market share among smartphone brands in China. Many factors contribute to these differences, with imaging being one of them. Industry research indicates that over 60% of users now demand more than just basic photography from their smartphones; they seek high-quality content creation capabilities. Therefore, mobile imaging represents an urgent industry challenge for smartphones, compelling major manufacturers to accelerate innovation.

Currently, the mid-range imaging sector has entered an indiscriminate hardware arms race. Several brands have introduced flagship-grade optical components to models priced in the two to three thousand yuan range for their summer releases. The specifications for lenses, sensors, and image stabilization systems are converging towards those of high-end models. Hardware homogenization directly dilutes differentiated competitiveness, with cost pressures first eroding profits in the mid-range product lines.

The most noticeable change in the mid-range market in 2026 is that features previously exclusive to flagship models priced above 5,000 yuan, such as large-aperture primary cameras and telephoto lenses, have become standard across some mid-range models.

The OPPO Reno 16 series is equipped with a 200-megapixel primary camera across all models, complemented by a 50-megapixel periscope telephoto lens and a 50-megapixel ultra-wide-angle lens. The OPPO Reno 16 Pro also incorporates a micro-gimbal structure, supporting intelligent correction of up to 5° of focal plane rotation to enhance stability in video and motion shooting scenarios. The front camera also boasts 50 megapixels and supports live photo functionality.

The vivo S60 series continues to focus on portrait photography, further refining portrait bokeh and skin tone optimization. It emphasizes the "Native 4K Live" experience, optimizing 4K Live at the system level to reduce memory usage and enhance picture smoothness. In terms of hardware, the vivo S60 features a 50-megapixel Sony gimbal-grade image stabilization primary camera, supporting 3° OIS optical stabilization, along with a 50-megapixel Sony periscope telephoto lens that supports 360° horizon stabilization and CIPA 5.0-level stability performance.

The Honor 600 Pro is equipped with a 200-megapixel ultra-clear large-aperture primary camera, paired with ultra-strong CIPA 6.0-level image stabilization. It supports 4K Live lossless retouching, and after retouching, it can directly support 4K Live lossless sharing on the Xiaohongshu platform without image quality (image quality) being compressed or degraded. Vibrant moments of youth can be steadily preserved and shared without compression. This series achieves full-focal-length 4K Live output and is the industry's only model supporting 7X ultra-telephoto 4K Live output.

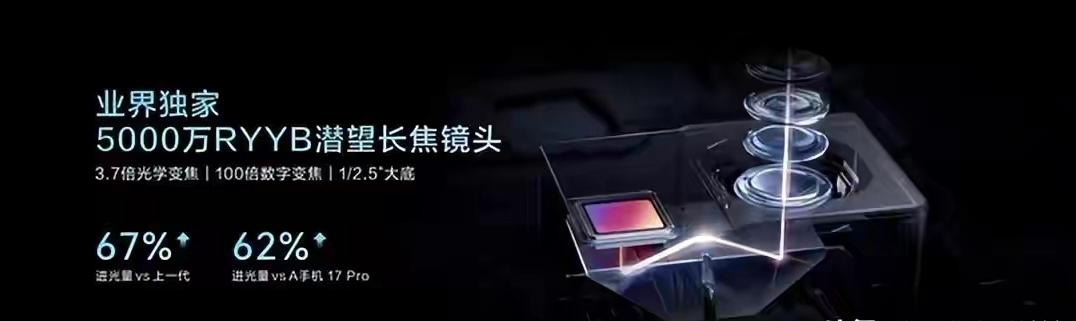

The Huawei nova 16 series, relying on the XMAGE domestic imaging system, is fully equipped with an industry-exclusive 50-megapixel RYYB periscope telephoto lens. The nova 16 Pro and nova 16 Ultra also support 3.7X optical zoom and 100X digital zoom. Paired with the new AI telephoto enhancement technology, clear shots can be taken even from the back row at concerts.

From an industry perspective, after viewing the above imaging performance introductions, most people will have two impressions: things are getting more impressive, but it's hard to distinguish which brand is truly superior.

These doubts are normal. Three years ago, mid-range models generally featured a single 100-megapixel primary camera paired with filler depth-of-field lenses. The average number of lenses per device stabilized at around 3.2, with most complaints focusing on battery life, screen quality, and system smoothness. Heavy investments in imaging hardware similarly failed to translate into core reputation advantages.

When encountering some young female consumers, they may not understand these specifications but will still insist that Apple's photography and videography capabilities are the best.

Therefore, all commercial competitions follow the same pattern: when the barriers to entry in a sector are relentlessly lowered, even substantial hardware investments become sunk costs. The mid-range imaging sector is now at this stage, with manufacturers competing on sensor size, pixel count, and telephoto magnification. However, consumers find it difficult to discern subtle differences in image quality, and hardware intensification only raises overall industry costs without any brand being able to establish long-term barriers based on imaging alone.

Currently, there are no clear winners in the imaging arms race, only continuously shrinking profit margins. With hardware competition reaching its peak, manufacturers can only pin their hopes on AI imaging algorithms, attempting to break free from parameter homogenization through software differentiation. The actual commercial value of AI imaging needs to be re-evaluated, stripped of promotional rhetoric.

02 How Valuable is AI Imaging?

More than a decade ago, major manufacturers competed on features like ultra-wide-angle lenses. Now, they view AI imaging as a breakthrough from hardware intensification. However, when implemented in mid-range models, AI imaging falls short of industry expectations in terms of monetization capability, user frequency, and device upgrade Pull effect (pulling effect). The cost-effectiveness of AI algorithm investments continues to decline.

From a product implementation perspective, most manufacturers have introduced AI imaging capabilities to their mid-range models.

Their strategies are clear: leveraging on-device models to support live photo editing, automatic video motion generation, AI noise reduction optimization in low-light scenes, and built-in dozens of AI short video templates, primarily targeting young users' Vlog creation. AI-powered intelligent skin tone zoning for portraits and dynamic live sticker generation are core features, with scene-specific optimizations for selfies and portrait photography.

Other manufacturers utilize AI multi-frame night photography, intelligent frame interpolation for motion capture, and automatic composition correction to cover all shooting scenarios. Their algorithms, paired with AI color reconstruction, distinguish between landscapes, portraits, and night scenes, automatically switching underlying imaging logic.

When it comes to consumers, most users only utilize the default auto mode for shooting. Core promotional features like AI beauty, AI composition, and video AI editing see limited monthly usage. Moreover, in complex lighting conditions, mid-range models' AI scene recognition accuracy is limited. In low-light and backlight scenarios, AI algorithms are prone to color distortion and overexposure, with algorithm stability far inferior to high-end flagship models. Constrained by NPU computing power, mid-range models cannot run complete large models, and lightweight stripped-down versions offer significantly diminished experiences.

It's worth noting that many AI imaging features fail to justify product premiums. E-commerce price monitoring data shows that the price difference between standard and AI imaging Pro versions within the same smartphone series typically ranges from 300 to 500 yuan. However, Pro versions generally see a 200 yuan price drop in channels within three months of launch, quickly erasing the price differential. Consumers are unwilling to pay a long-term premium for AI imaging capabilities.

While high-end models can sustain premiums with complete large models and exclusive imaging partnerships, mid-range models, constrained by computing power and lacking exclusive algorithm barriers, can only use AI as a promotional gimmick without converting it into sustained purchasing motivation.

Clearly, the speed of technological expansion does not equate to the speed of commercial value realization. At the end of technological proliferation lies functional homogenization. Currently, mid-range AI imaging is replicating the path of hardware stacking, with highly overlapping algorithm functions across brands, primarily focusing on three basic scenarios: portraits, night scenes, and short video editing. There are no exclusive or irreplaceable features.

Substantial investments in algorithm development and chip upgrades only briefly generate buzz for new product launches. Translating these into long-term brand competitiveness faces increasing pressure from homogenization.

This reflects another core truth: after intensification in both hardware and software imaging sectors, the market reveals its most fundamental reality: overall smartphone growth can never rely solely on a single imaging segment.

03 Smartphone Growth Cannot Rely on Imaging Gimmicks

Currently, structural differentiation in the inventory (stock) smartphone market is a foregone conclusion. Goldman Sachs predicts that the global mid-range model market share will shrink from 35% in 2021 to 23% by 2027, with the high-end market continuing to expand and the low-end market contracting. The survival space for the mid-range sector is continuously narrowing. Simply doubling down on imaging cannot reverse industry growth fatigue. The underlying logics of upgrade cycles, consumer demand, and market segmentation collectively determine that imaging alone cannot drive industry growth.

First, the fundamental driving force behind user device upgrades has long shifted away from pure imaging dimensions. Currently, user upgrade cycles exceed 40 months, with consumers simplifying their upgrade criteria to "when the device can no longer function normally" rather than the addition of new imaging features. The widespread adoption of short video and social media platforms over the years has saturated user shooting demands. The basic image quality of smartphone cameras fully meets daily needs for posting photos and short videos, making the incremental experience gains from imaging upgrades barely perceptible.

Second, market segmentation undermines the pulling effect of the imaging sector.

The share of high-end models priced above 600 continues to rise, with high-end users willing to pay a premium for fully self-developed imaging systems, exclusive optical partnerships, and complete AI large models. Mid-range users are highly price-sensitive, with many rejecting smartphone price hikes and adhering to budgets in the 2,000 to 3,500 yuan range. Under budget constraints, manufacturers' imaging investments continuously squeeze other hardware budgets, leading to imbalanced overall product experiences and further reducing user repurchase intentions. Low-end models priced below 1,000 yuan focus solely on basic communication and battery life, completely abandoning imaging enhancements and relying on low prices to siphon off budget-constrained users. Mid-range models face pressure from both ends, with imaging serving only as a marketing tool to attract fleeting attention without expanding the overall market size.

Meanwhile, the core growth drivers for the industry lie beyond imaging. HarmonyOS and iOS cross-device ecosystems, satellite communication, lightweight on-device full-scenario AI, and long-lasting fast charging are increasingly becoming the core levers for driving sales in high-end models.

In contrast, in the mid-range market, manufacturers allocate all their resources to imaging R&D and material procurement, continuously shrinking investments in screen, battery, and system interaction innovations. Products lack other memorable features besides the camera, falling into the trap of being "good only for photography and nothing else."

It's evident that market competition logic has long shifted. A single functional advantage cannot sustain the growth of an entire product line. Comprehensive and balanced experiences across all dimensions, differentiated form factors, and ecosystem synergies represent the growth formula for the stock market.

Of course, resource misallocation is the core issue behind mid-range imaging intensification. Manufacturers bet all their limited R&D and cost budgets on imaging, chasing short-term buzz for new product launches while neglecting users' actual upgrade needs and the industry's long-term growth sectors.

However, no single function can support the trillion-yuan smartphone market in the long run. Over-allocating resources only exacerbates sectoral infighting and prolongs the industry's profit recovery cycle. Imaging can serve as a product bonus but will never become the primary engine for industry growth.

Looking back, the dilemma in the imaging sector essentially stems from industry innovation path dependency. Various parameter innovations still fall within the realm of parameter stacking and intensification. Manufacturers are accustomed to using lenses, pixels, and algorithms to create product differentiation but overlook that users' actual demands have shifted towards battery life, systems, cross-device ecosystems, and entirely new product form factors.

If all brands crowd into the same narrow track (sector), no matter how lively new product launches are, they cannot conceal the clear growth ceiling.

In consumers' eyes, a smartphone's value extends far beyond the images captured by its camera.

-

![]()

From Hardware to AI: Has the Intense Competition in Smartphone Imaging Reached Its Limit?

-

![]()

Mired in Pricing Controversy and Stock Price Slump: What Ails MiniMax?

-

![]()

DJI and Insta360 Release 'Cinematic Cameras': Can Pocket Stabilizer Cameras Truly Make It onto Professional Film Sets?

-

![]()

AISpeech's IPO Journey: Valuation Soars by RMB 2 Billion in a Month, Alibaba Trims Stake for RMB 280 Million Gain, Short-Term Debt Deficit Hits RMB 168 Million

-

![]()

DingTalk: At a Crossroads

-

![]()

Uber Exhausts Annual AI Budget in Just Four Months: Why Even Uber Can’t Sustain Token Costs?

-

![]()

"Explosive Risks" in the Trunk: The Unauthorized Battery Modifications in New Energy Vehicles Fuel a Shadowy Industry

-

![]()

From Deep Ties to Strategic Divestment: Is Chery Reevaluating Its Stake in This Industry Leader?