From Deep Ties to Strategic Divestment: Is Chery Reevaluating Its Stake in This Industry Leader?

06/11 2026

06/11 2026

414

414

The automotive components sector recently witnessed significant turbulence following an announcement regarding stake reduction in Bethel [603596.SH] on the secondary market.

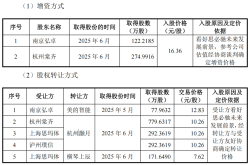

On June 5, Bethel disclosed that its second-largest shareholder, Wuhu Chery Technology, intends to divest up to 26.9292 million shares, equivalent to 3% of the company's total share capital, within the next three months.

As of the announcement date, Wuhu Chery Technology held 130.6727 million shares in Bethel, representing 14.56% of the company's total share capital. Based on the closing price of RMB 30.82 on that day, Chery Technology stands to realize up to RMB 830 million from this divestment.

Ironically, just half a month prior, this domestic frontrunner in intelligent chassis systems had submitted its IPO prospectus to the Hong Kong Stock Exchange, officially embarking on its A+H dual-listing journey.

The timing of this established industrial capital's exit for cash, juxtaposed with the listed company's hurried rush to raise funds in Hong Kong, seems somewhat paradoxical. Market attention has now shifted to Bethel's operational performance in 2025 and the underlying risks associated with its Hong Kong listing.

At the crossroads of intelligent chassis localization and the evolving growth dynamics of new energy vehicles, this combination of shareholder stake reduction and HKEX IPO actually reveals the company's growth trajectory and inherent challenges.

1

2025 Product Structure: A Mixed Bag

Bethel primarily operates within the automotive intelligent chassis systems domain, with a current business portfolio encompassing automotive braking systems, steering systems, suspension systems, intelligent driving systems, and lightweight components.

In 2025, the company ventured into core robot components, focusing on breakthroughs in the independent research and manufacturing of planetary roller screw nuts, micro screw nuts, high-performance brushless motors, and robot joint modules.

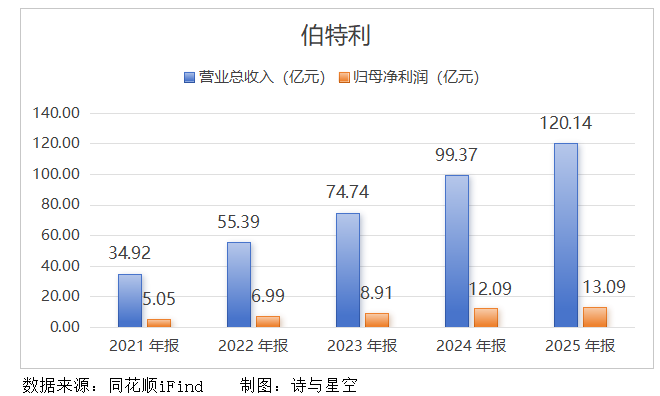

In 2025, Bethel reported annual revenue of RMB 12.014 billion, marking a significant year-on-year increase of 20.91%. However, net profit attributable to shareholders grew by a mere 8.32% year-on-year, to RMB 1.309 billion. Revenue growth significantly outpaced profit growth, with a decline in gross margin being the primary culprit behind the sluggish profit expansion.

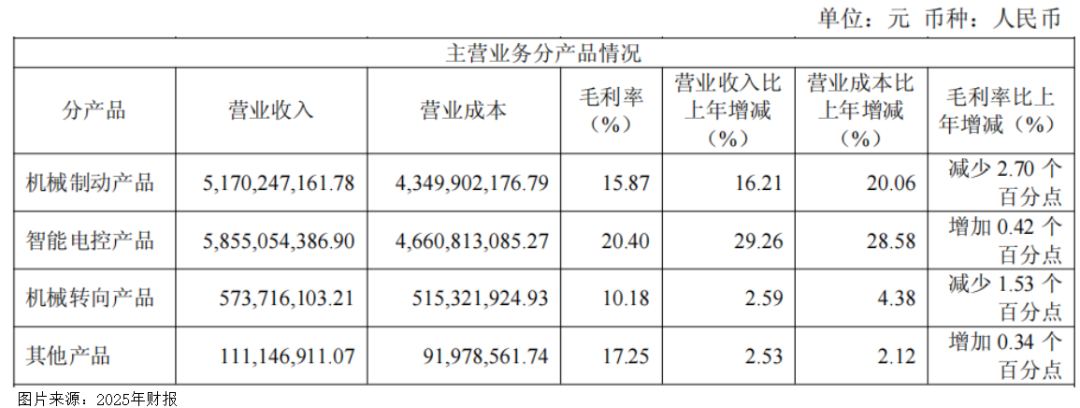

By product category, revenue from intelligent electronic control reached RMB 5.855 billion, up 29.26% year-on-year, with a gross margin of 20.40%. Multiple new platforms for WCBS brake-by-wire systems entered mass production in 2025, and EMB (electro-mechanical braking) achieved small-volume deliveries by year-end. Overseas EPB (electronic parking brake) orders were secured from Ford Europe and Renault, directly fueling growth in this segment.

Revenue from mechanical braking products was RMB 5.170 billion, up 16.21% year-on-year, although gross margin declined by 2.7 percentage points. Mechanical steering revenue was just RMB 574 million, up 2.59% year-on-year, with gross margin shrinking by 1.53 percentage points.

This was primarily attributable to rising raw material costs for steel and aluminum ingots, compounded by sustained price pressure from vehicle manufacturers, which trapped traditional chassis components in a dilemma of increasing volume but shrinking profits.

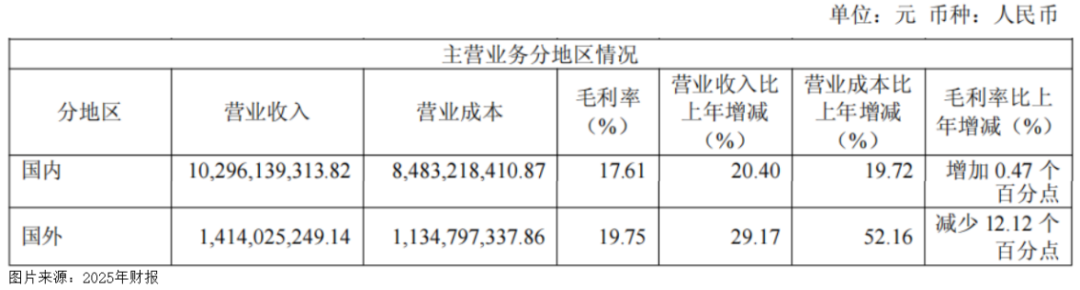

Regionally, domestic revenue was RMB 10.296 billion, up 20.40% year-on-year, with a slight 0.47 percentage point increase in gross margin. Overseas revenue reached RMB 1.414 billion, up 29.17% year-on-year.

Despite impressive revenue growth, gross margin plummeted by 12.12 percentage points, primarily due to the newly commissioned Mexican factory still ramping up production, coupled with amortization of factory construction costs, rising overseas labor costs, and increased tariffs, all of which weighed on overseas profitability.

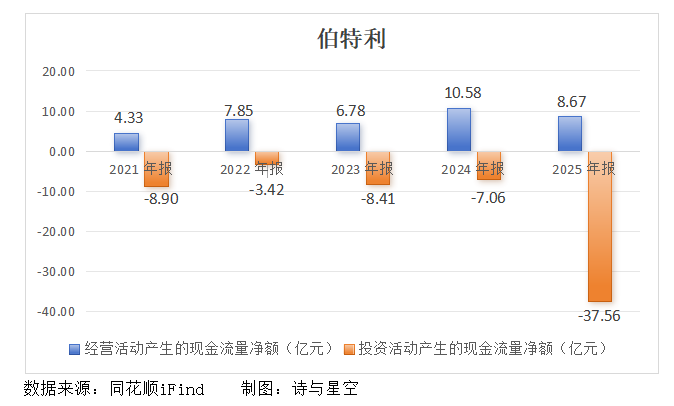

Concerns also linger at the cash flow level. In 2025, operating cash flow was RMB 867 million, down 18.04% year-on-year, mainly due to increased inventory for expansion and rising accounts receivable. Investing cash flow saw a substantial net outflow of RMB 3.756 billion, driven by ongoing overseas factory construction in Mexico and Morocco, as well as continued investment in EMB/EPB brake-by-wire and fundraising projects.

Overall, while Bethel's high-end electronic control business grew in 2025, traditional operations and overseas factory construction continued to erode profit margins.

2

The Rationale Behind Chery Technology's Stake Reduction

As a founding-level industrial capital partner that has accompanied Bethel from inception to listing, Chery Technology began small-scale stake reductions in 2022, officially citing the group's need for industrial capital coordination.

In recent years, Chery Group has ramped up investments in multiple sectors, including new energy vehicles, semiconductors, low-altitude economy, and robotics. Chery Technology, as the group's capital operation platform, holds stakes in multiple listed companies. Recouping funds through phased reductions of high-quality assets to support the group's core businesses and emerging industry investments is a standard capital maneuver.

Data reveals that Chery Technology initially held 66.378 million shares from the IPO. Through stock splits and capital reserve transfers over the years, its holdings have now increased to 131 million shares, with an extremely low cost basis. Having already cashed out RMB 319 million in 2022, a full reduction in this round would recoup an additional RMB 830 million, significantly bolstering the group's cash flow.

Moreover, in the first half of 2026, the automotive components sector continued to strengthen, driven by brake-by-wire and robotics concepts, with Bethel's stock price consistently above RMB 30. Chery's holdings have generated substantial unrealized gains, making the timing of this reduction—during Bethel's Hong Kong IPO and amid high market sentiment—particularly precise.

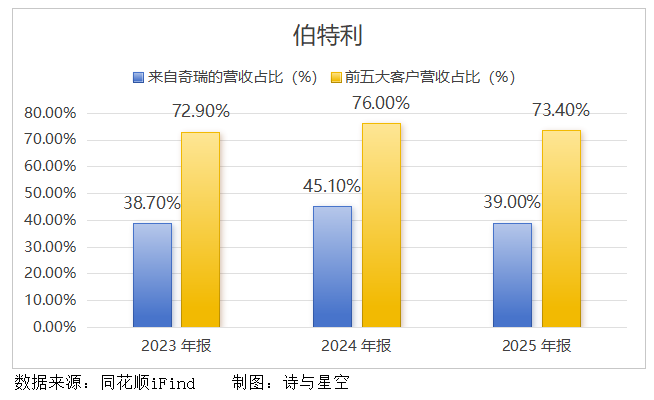

Notably, Chery is Bethel's largest customer, accounting for nearly 40% of revenue from 2023 to 2025, although this figure declined to 39% in 2025. As the customer base continues to diversify, with increasing orders from domestic and foreign automakers such as GM, Ford, NIO, and XPeng, Bethel's reliance on Chery has diminished year by year.

Gradual stake reductions at the equity level, coupled with deepened supply cooperation at the business level, are standard practices for Chery. Equity exits do not affect upstream-downstream ties, as evidenced by the parties raising the cap on sales-related connected transactions to RMB 6.73 billion in 2026, indicating no loosening of supply cooperation.

It is important to clarify that Chery's stake reduction does not equate to a lack of confidence in Bethel's intelligent chassis sector. The domestic market for brake-by-wire, EMB, and air suspension systems is still expanding, and Bethel's position as a domestic leader remains secure. The reduction is more about the industrial capital's own financial optimization.

3

Potential Risks Associated with the HKEX Listing

On May 21, Bethel submitted its prospectus to the Hong Kong Stock Exchange, formalizing its A+H listing plan. The company stated that the funds raised would be used for the second phase of its Mexican factory, a new factory in Morocco, expansion of EMB and air suspension production, and R&D of robot components. However, given the 2025 financial results and industry conditions, the HKEX listing path harbors multiple uncertainties.

First, the top five customers account for over 73% of revenue, with Chery alone contributing nearly 40%. Although the customer base is diversifying, order fluctuations from major automakers can still directly impact the company's revenue.

In recent years, the automotive industry has been plagued by frequent price wars, with automakers continuously pressing for lower prices from suppliers, putting long-term pressure on component margins. If Chery or major new energy vehicle manufacturers underperform in production and sales, Bethel faces immediate risks of order contraction and profit decline. Consequently, HKEX investors are generally cautious in valuing manufacturing enterprises with high customer concentration.

Coupled with a surge in investment spending in 2025, including simultaneous construction of a lightweight factory in Mexico, a vehicle component base in Morocco, and multiple new EMB brake-by-wire production lines, as well as ongoing investments in robot screw nut and motor joint ventures, capital expenditures for projects under construction will remain substantial over the next 2-3 years. Rising depreciation and financial expenses will continue to suppress net profit margins.

Notably, the Mexican factory relies on the USMCA agreement to supply North American customers, but trade policies between the U.S. and Mexico are subject to change, and tariff adjustments could raise production costs. The Moroccan factory targets the European market, but geopolitical risks, local labor laws, and infrastructure progress introduce variables. Especially since overseas factories typically have longer ramp-up periods than domestic ones, delays in production could hinder capacity utilization and profitability.

Additionally, the robot components sector is fiercely competitive, with numerous domestic players entering the fray. For Bethel, uncertainties persist in technology commercialization, customer nominations, and scalable mass production. The new business is unlikely to contribute significant profits in the short term, and sustained losses could erode profits from the core business, affecting HKEX valuation and pricing.

The timing of this large-scale stake reduction plan by the second-largest shareholder, Chery, during the IPO window could easily signal to potential HKEX investors that original shareholders are exiting at a high, dampening institutional subscription enthusiasm and increasing issuance difficulty. If A-share prices fluctuate downward during the reduction process, the HKEX offering price will also face downward pressure, potentially leading to reduced fundraising.

4

Conclusion

Overall, Chery's stake reduction is a capital cycle maneuver that does not undermine Bethel's fundamentals as a domestic leader in intelligent chassis systems. In 2025, Bethel achieved steady revenue growth, continued expansion in high-end electronic control, and orderly progress in three new businesses: EMB, air suspension, and robotics. The long-term logic of import substitution and global expansion remains valid.

The HKEX listing is a necessary step in the company's globalization strategy, providing international financing channels to support overseas factory construction and customer expansion. However, in the short term, it must confront multiple challenges, including customer concentration, heavy investment, and valuation disparities.

Going forward, attention should focus on the mass production and gross margin trends of Bethel's intelligent electronic control products, the ramp-up progress and profitability of its Mexican and Moroccan factories, as well as the actual scale of Chery's stake reduction and the outcome of the HKEX IPO.

-END-

Disclaimer: This article is based on the public company attributes of listed companies and relies primarily on information disclosed by the companies in accordance with their legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms) as the core basis for analysis and research. Shiyu Xingkong strives to ensure fairness in the content and viewpoints presented in its articles but does not guarantee their accuracy, completeness, or timeliness. The information or opinions expressed in this article do not constitute any investment advice, and Shiyu Xingkong assumes no responsibility for any actions taken based on this article. Copyright Notice: The content of this article is original to Shiyu Xingkong and may not be reproduced without authorization.

-

![]()

From Hardware to AI: Has the Intense Competition in Smartphone Imaging Reached Its Limit?

-

![]()

Mired in Pricing Controversy and Stock Price Slump: What Ails MiniMax?

-

![]()

DJI and Insta360 Release 'Cinematic Cameras': Can Pocket Stabilizer Cameras Truly Make It onto Professional Film Sets?

-

![]()

AISpeech's IPO Journey: Valuation Soars by RMB 2 Billion in a Month, Alibaba Trims Stake for RMB 280 Million Gain, Short-Term Debt Deficit Hits RMB 168 Million

-

![]()

DingTalk: At a Crossroads

-

![]()

Uber Exhausts Annual AI Budget in Just Four Months: Why Even Uber Can’t Sustain Token Costs?

-

![]()

"Explosive Risks" in the Trunk: The Unauthorized Battery Modifications in New Energy Vehicles Fuel a Shadowy Industry

-

![]()

From Deep Ties to Strategic Divestment: Is Chery Reevaluating Its Stake in This Industry Leader?