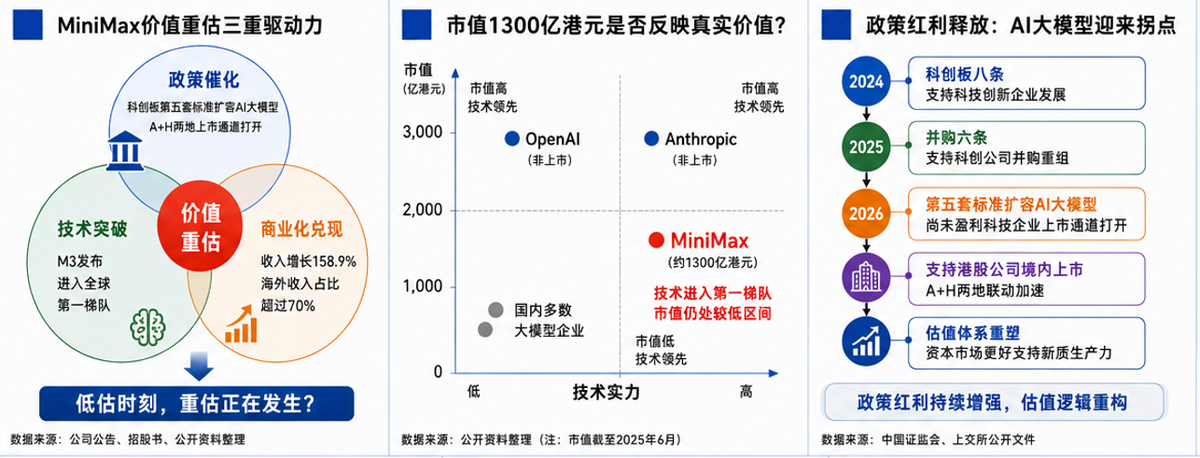

Policy Support & Tech Leap: MiniMax at a Pivotal Moment for Revaluation

06/18 2026

06/18 2026

328

328

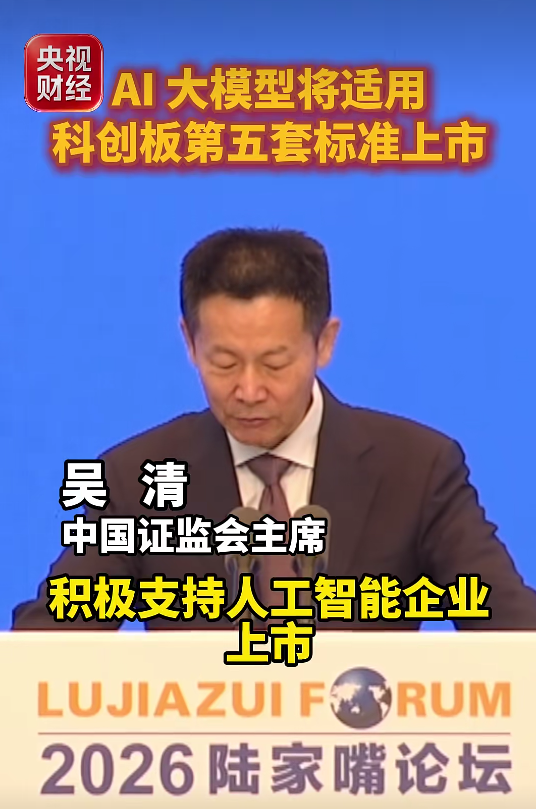

On June 17, 2026, at the Lujiazui Forum, a speech by Wu Qing, Chairman of the China Securities Regulatory Commission (CSRC), sent a strong policy signal to China's domestic large model sector.

Just half a month prior, MiniMax unveiled its new flagship model, M3, which has proven competitive with leading global models in multiple international benchmark tests.

With policy tailwinds and technological breakthroughs converging, MiniMax, a leading AI company listed in Hong Kong, now stands at a valuation crossroads that warrants a fresh look.

I. Policy "Boost": STAR Market Expands Inclusion for Large Models

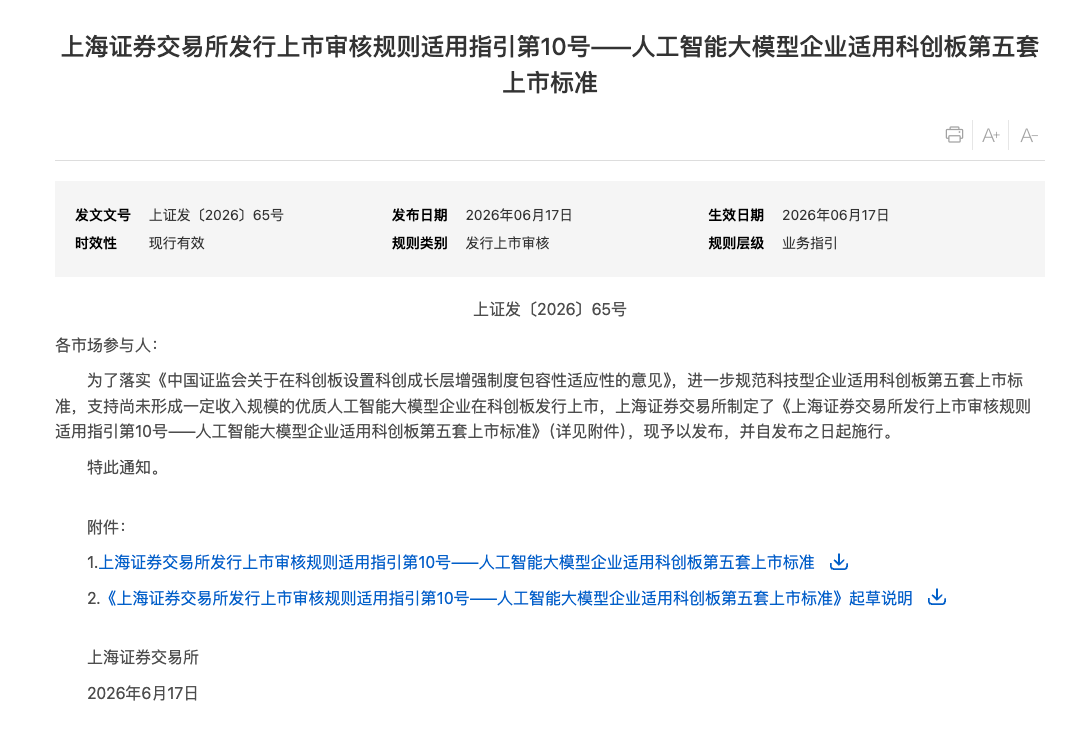

At the Lujiazui Forum, Chairman Wu Qing explicitly announced that the fifth set of listing criteria for the STAR Market would be expanded to include AI large model companies.

A-shares are set to roll out a series of policy measures, including the "Eight STAR Market Initiatives," "Six M&A Reforms," "STAR Market 1+6 Framework," and deepening reforms of the ChiNext board. Innovative steps such as establishing a STAR Growth Tier, implementing a pre-review mechanism, and allowing local governments to recommend companies for listing are all expected to proceed smoothly.

Currently, the fifth set of criteria is tailored for tech companies that have yet to achieve profitability but possess core technologies. Key thresholds include an expected market capitalization of no less than RMB 4 billion and the need to demonstrate "stage-based achievements."

This means that AI large model companies that are not yet profitable but possess core competitiveness will face significantly fewer institutional barriers when listing on the A-share capital market.

Meanwhile, Wu Qing also explicitly stated, "We support eligible Hong Kong-listed companies to list domestically, fostering linked development between the two markets." This statement is widely interpreted by the market as an institutional pathway that could accelerate the return of Hong Kong-listed AI companies to the A-share market.

The combination of these policies creates a "triple boost" for large model companies: AI firms yet to list gain a smoother path to market, while those already listed in Hong Kong open up possibilities for a return to the A-share market.

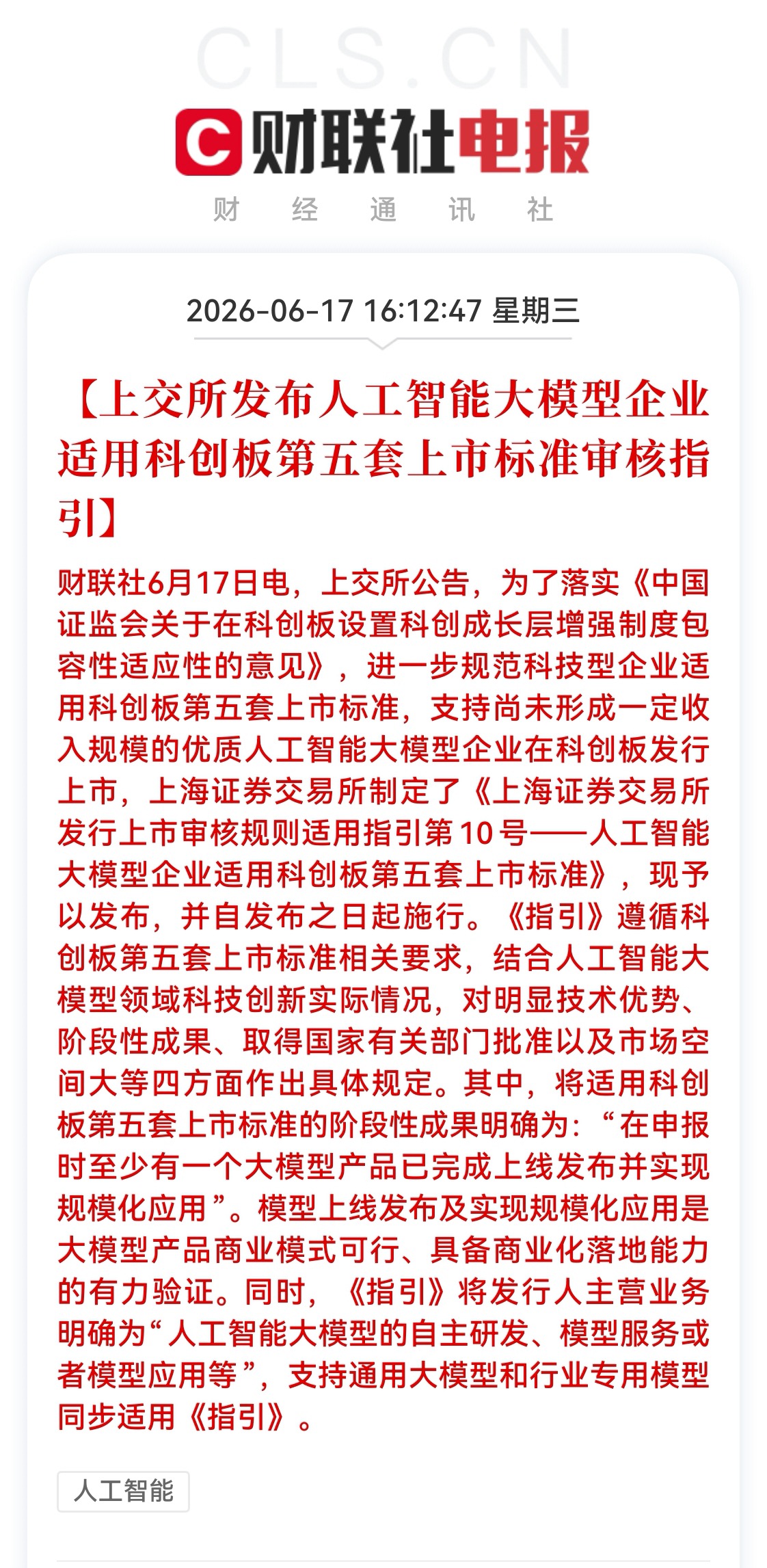

Simultaneously, the Shanghai Stock Exchange issued the "CSRC's Opinions on Establishing a STAR Growth Tier on the STAR Market to Enhance Institutional Inclusiveness and Adaptability," further clarifying the application of the fifth listing criteria for tech companies on the STAR Market and supporting high-quality AI large model companies without significant revenue scale to list on the STAR Market.

Among these, the "stage-based achievements" required for applying the fifth listing criteria on the STAR Market are clarified as: "At least one large model product must have been officially launched and achieved large-scale application at the time of application."

MiniMax, which officially listed on the Hong Kong Stock Exchange in January this year, has a clear commercialization path. In 2025, its total revenue grew by 158.9% year-on-year to reach USD 79 million, with over 70% of revenue coming from international markets.

Its M2 model quickly gained recognition from the global developer community after its release, becoming the first Chinese model on OpenRouter to exceed 50 billion daily Token consumption and topping the HuggingFace global hot list, perfectly meeting the new regulatory requirements.

Moreover, the technology sector now accounts for over 30% of the market capitalization of A-share tech stocks, with tech companies making up 45% of listed companies with market caps exceeding RMB 100 billion.

If a series of eligible high-quality large model tech stocks like MiniMax can list more efficiently on the A-share market, the trend of mutual empowerment between the capital market and new quality productive forces will accelerate.

II. MiniMax M3: Technological Prowess Ranks Among Global Elite

In addition to past achievements, half a month before the policy announcement, MiniMax officially released its new flagship model, M3, on June 1.

This model has proven with solid data that domestic large models now possess the capability to compete head-to-head with global leaders.

Official data shows that on the SWE-Bench Pro benchmark, which measures programming capabilities, MiniMax M3 outperformed OpenAI's GPT-5.5 and Google's Gemini 3.1 Pro, approaching Claude's Opus 4.7. On the SVG-Bench benchmark, which comprehensively evaluates a model's ability to generate scalable vector graphics, MiniMax M3 surpassed Opus 4.7.

Even more astonishing is M3's "autonomous work" capability.

The research team assigned M3 a task: train four models from scratch with only pre-trained bases within 12 hours. M3 autonomously completed the full closed loop of "data synthesis—training—evaluation—iteration," ultimately scoring 0.37, closely trailing GPT-5.5 (0.39) and Opus 4.7 (0.42).

In another extreme test, M3 worked continuously for 24 hours, completing 147 benchmark submissions and 1,959 tool calls, pushing the peak hardware utilization rate of CUDA kernels on NVIDIA's Hopper architecture from 7.6% to 71.3%, achieving a 9.4x speedup—all without human intervention.

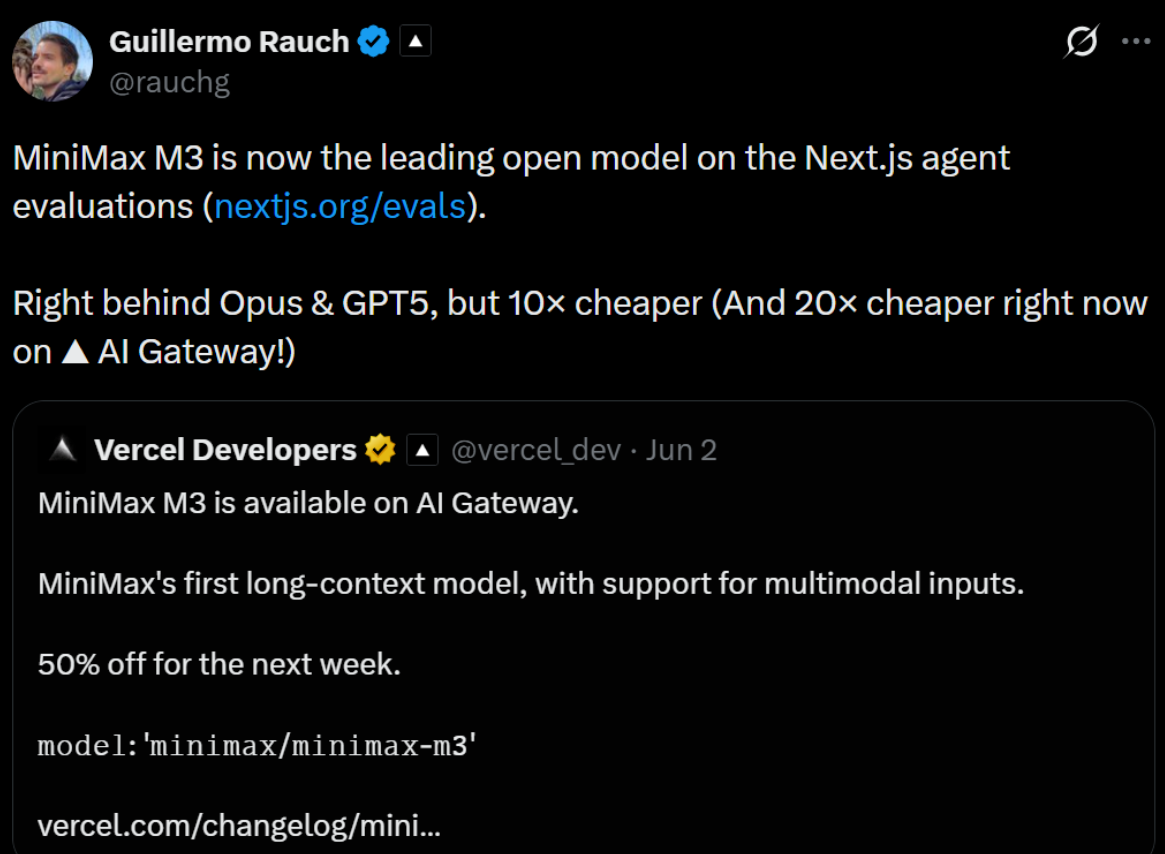

The response from the international tech community has been equally enthusiastic.

Guillermo Rauch, CEO of Vercel with 5.4 million followers, rarely publicly endorsed M3. Thomas Wiegold, a notoriously strict AI evaluator, described M3 as "one of the most interesting models I've tested this year."

III. Standing at the Forefront of the Era: Catalysts for Valuation Reassessment Gather

On May 28, MiniMax disclosed its latest business data. To date, the company serves over one million global enterprise and developer clients, a 5x increase from six months ago, with a global user base of approximately 300 million. Over the past two months, the company's Annualized Recurring Revenue (ARR) has grown by over 100%, with its B-end commercialization engine entering a phase of vertical acceleration.

According to public information from its March earnings call, by February 2026, MiniMax's ARR had exceeded USD 150 million. During the same period, the daily Token consumption of its M2 series models grew 6x within two months, while new registrations on its open platform increased more than 4x. The latest data indicates that MiniMax's ARR doubling cycle has compressed to 60 days, with growth rates on par with the fastest-growing global AI companies during the same period.

MiniMax has built full-modal R&D capabilities, with globally competitive models in key modalities such as language, video, voice, and music.

Now, with the strong launch of M3, its outstanding performance has given the market more room for imagination and provided more users and enterprises with the impetus to choose MiniMax.

On June 15, Alipay's official Weibo account announced that Token Pay would fully integrate with MiniMax M3, launching the country's first MaaS payment solution for large-scale application.

By integrating with Alipay's Token Pay, MiniMax has effectively established a comprehensive payment SaaS system, enabling enterprises to manage Token allocations with "bulk purchasing and one-click distribution," taking a significant step forward in the commercialization of large models.

IV. Valuation Reassessment: The Underestimated Certainty

Previously, when JPMorgan downgraded MiniMax's Hong Kong stock rating to neutral, the core concern was the lack of a new domestic SOTA model since M2.

Now, M3 has answered with scores, dispelling that concern. On June 15, BofA Securities gave a "buy" rating, noting that MiniMax is "China's leading foundational model company, early to commit to multimodal model innovation, and possesses global consumer AI reach."

But pricing is another matter.

The market's state for such AI companies is typical. Expectations have already been tempered once, with share prices at lows, but policy margins are rising, technologically verifiable results continue to emerge, and commercialization infrastructure is beginning to fall into place. Historically, this combination often points to a situation: share prices no longer reflect the grand narrative; instead, they begin to reflect a more fundamental question—whether the market is still willing, or daring, to give it another chance at revaluation.

For investors, the growth trajectory of quarterly ARR, the pace of gross margin improvement, and the timing of the profitability inflection point will be the three most critical metrics to track continuously. It is reported that MiniMax has initiated preparations for a STAR Market IPO. Once the A+H dual-listing structure is in place, as a pioneer in responding to this policy channel, it is poised to enjoy the valuation premium that A-shares offer for hard-tech companies.

Now, M3 has proven that domestic large models can score on the global top stage, Token Pay is converting technological capabilities into trackable revenue data, and the policy gates have opened. Together, these three events constitute a rare certainty amid uncertainty.

At its current market capitalization of around HKD 130 billion, the pricing of this certainty is clearly inadequate.

But with M3 having proven that Chinese large models can outperform global leaders, value discovery in the capital markets is unlikely to remain absent for long.

-

![]()

Chinese New Energy Vehicle Design: Stepping Out of the Shadows

-

![]()

Li Auto Awards Executives 35 Million Shares Based on Performance Metrics

-

![]()

Rushing Towards AI 2.0: How Confident is Unisound?

-

经过今年上半年各路AI豪强对市场的反复教育,有一个判断,可能决定未来一两年的走向:

-

![]()

Global Tech Sector Sees Collective Panic: Is the AI Hype Finally Deflating?

-

![]()

Three Consecutive Rises in Heavy Truck Sales: Both New and Old Players are Betting on the Same Thing!

-

![]()

Why Can’t Vivo Bridge the High-End Perception Gap Despite Support from Authoritative Media?

-

![]()

Regulatory Measures and Industry Norms: The Transformation of GEO's Trajectory in the Second Half