Rushing Towards AI 2.0: How Confident is Unisound?

06/18 2026

06/18 2026

505

505

Anyone with a dream is remarkable!

Editor: Chu Yi

Contributor: Zhang Ge

Source: Shoucai - Shoutiao Finance Research Institute

Going public has never been the finish line, but rather the starting point for new value. This sentiment is vividly exemplified by Unisound.

On June 8th, the company unveiled its native agent large model U2, 'Built for Execution,' systematically showcasing continuous execution capabilities for real-world tasks. In complex office scenarios, software engineering, in-depth research, and multi-tool collaboration, U2 can autonomously break down and advance complex workflows exceeding 100 steps. Moving from 'providing answers' to 'completing tasks' marks the emergence of a 'native agent large model company.'

It should be noted that since going public on June 30, 2025, and becoming the 'first AGI stock on the Hong Kong Stock Exchange,' the market has placed high hopes on the company. Founder Huang Wei views the listing as a new starting point. According to LatePost, Huang revealed, 'U2 is more symbolic. The entire AI paradigm has shifted from 1.0 to 2.0, and Unisound has completed its listing. We hope everyone, from top to bottom, realizes that we can no longer approach 2.0 with a 1.0 mindset.'

In other words, the release of U2 represents not just a technological upgrade but a comprehensive shift in the company's strategic direction. As the one-year anniversary of its listing approaches, its development ambitions are clear. How appealing is the 2.0 narrative? How close is Unisound to taking off anew? Are there any lingering obstacles?

1

Results-Oriented Business Approach

High Intelligence Density × High Token Value

Peter Drucker, the father of modern management, famously said, 'The focus of innovation is the market, not the product. Only by continuously meeting market demands can businesses and industries sustain growth.' This perfectly captures a prevalent issue in the current AI industry.

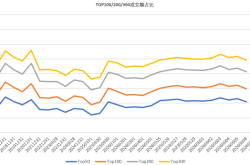

According to J.P. Morgan's forecasts, China's AI inference token consumption will surge from approximately 10 quadrillion in 2025 to around 390 quadrillion by 2030, a 370-fold increase over five years. The token consumption of a complex agent task can easily be dozens or even hundreds of times that of a standard conversational mode. Avoiding a disorderly 'token consumption race' in AI is a serious topic.

Against this backdrop, Unisound U2 proposes its technical philosophy: high intelligence density × high token value. Huang Wei explains that high intelligence density does not simply emphasize small model size but rather measures how much knowledge, reasoning ability, and task-solving efficiency are packed into each unit of parameters after the model achieves global top-tier performance. High token value focuses not on quantity but on whether each invocation truly translates into business results.

In simpler terms, the goal is not to stack parameters or extend output length but to achieve stronger capabilities with fewer resources, ensuring each token invocation brings results closer to actual delivery.

To efficiently implement this philosophy, Unisound did not follow the industry's common practice of 'completing model training first, then adding an agent framework.' Instead, it proposed a more groundbreaking approach:

First, it adopted a native agent model and Harness co-evolution mechanism. Traditional agent systems often resemble a shell wrapped around a general-purpose chat model, where the model only generates language, while task planning, tool invocation, and instruction execution are handled by external frameworks, leaving the model itself unaware of these processes.

In contrast, Unisound U2 internalizes complete capabilities—such as planning, execution, and result validation—directly into the model during training. Throughout training, the model and Harness (task execution scaffolding) continuously co-evolve. As the model's core structure becomes more complex, the scaffolding's support nodes and verification precision expand and refine, forming a self-reinforcing positive cycle.

To maximize the value of every client investment, U2's underlying technology strives for extreme optimization. Through the co-evolution of the model and its toolchain, it completes planning, invocation, execution, and validation with fewer interactions, significantly reducing token waste from repeated trial-and-error and improving task completion rates.

Second, it employed systematic application of process supervision and curriculum learning methods. During training, U2 introduces a 'curriculum learning' mechanism, guiding the model to gradually enhance its capabilities—from simple to complex tasks, short to long contexts, and single-tool to multi-tool coordination.

For long-duration tasks, U2 adopts advanced process supervision, where higher-performing models dissect, evaluate, and correct each critical node of task execution. This allows U2 to optimize not just the final outcome but also every execution step, dramatically accelerating learning convergence.

Third, it focused data scenarios on serving the real economy and hardcore industries. While most large models heavily rely on internet-derived general-purpose corpora for training, Unisound proactively reduced the proportion of low-value entertainment-related corpora, allocating more resources to high-value industry scenarios such as healthcare, medical insurance, government affairs, and industrial sectors. Training also incorporates real de-identified data accumulated from years of business deployments, aiming to directly serve the real economy and hardcore industries while cultivating efficient operational characteristics.

Thanks to its reconstructed underlying capabilities, U2 demonstrates strong performance competitiveness without blindly stacking parameters. For instance, it consistently ranks among the top performers in instruction-following evaluations like IFBench. In Claw-related assessments, its agent capabilities and tool invocation levels show prominent advantages. In evaluations involving hardcore knowledge reasoning and long-context tasks like GPQA, U2 rivals the world's top large models. In GDPval, which assesses real-world office and knowledge work delivery capabilities, U2 scored 72.5, showcasing solid professional office skills.

Ultimately, a token race detached from business results is merely another form of the 'technological miracle' trap. Unisound U2's reconstructive explorations and efficiency improvements directly address user pain points, paving a new path for the industry to avoid high-consumption, low-output traps and reach the market's core.

2

Continuous Evolution

The Foundation of Crossing Boundaries

Success is never accidental. These milestone breakthroughs stem from strategic deep cultivation (shēn gēng, meaning 'deep cultivation') and solid fundamental skills. Specifically, three core approaches have been pivotal:

First, prioritizing technology and infrastructure development. Founded in June 2012, Unisound specializes in IoT artificial intelligence services. According to 36Kr, Huang Wei once explained the meaning of 'sound' in the company's name: 'Behind sound lies language, and behind language lies intent. We listen not just to sound but to the consciousness behind it.' This encapsulates the company's technical philosophy: not settling for surface information but striving to understand genuine underlying needs.

Guided by this philosophy, the company has continuously accumulated technical expertise. For example, it established the Atlas AI infrastructure as early as 2016, laying the computational and architectural foundation for subsequent R&D.

Second, releasing foundational large models and nurturing core platform capabilities. In 2023, the company launched the Shanhai Large Model on its infrastructure and built the technical platform Unisound Brain. By 2025, it had doubled down on enhancing model capabilities along two main lines.

The first line involved breakthroughs in multimodal and deep reasoning capabilities. Unisound achieved deep alignment of text, image, audio, and cross-modal semantics. The Shanhai Large Model developed an efficient hybrid reasoning mode, effectively addressing model hallucination issues in serious scenarios and propelling the model from 'information retrieval and generation' to 'expert-like deep thinking.'

The second line focused on strengthening full-chain agent capabilities. The company upgraded its foundational architecture for native agent adaptation, enabling full-chain capabilities such as intelligent task decomposition, autonomous tool invocation, dynamic execution error correction, and multi-agent collaborative scheduling. This facilitated the upgrade from a 'conversational interaction tool' to an 'agent capable of autonomously completing complex tasks.'

Third, constructing and deploying a vertical large model matrix. Enhanced core capabilities accelerated the formation of a large model matrix. On one side are industry-specific vertical language large models for healthcare, medical insurance, and transportation. On the other are multimodal large models for medical imaging, Shanhai Zhiyin voice, and industrial-grade document OCR.

Take the healthcare sector as an example. The 'Shanhai·Zhiyi 5.0' adopts a 'text + multimodal' dual-core system, capable of parallelly processing multi-source heterogeneous data such as medical records, images, and test results. It also Derived from (yǎn shēng chū, meaning 'derives') a medical insurance large model deeply customized for insurance scenarios. In early 2026, Unisound successively released 'Shanhai·Zhiyin 2.0' and the industry's first industrial-grade document intelligence foundational large model, Unisound U1 OCR.

Supporting all these large-scale deployments is a mature, replicable business model and long-term strategic R&D investment. As the core of Unisound Brain, the Shanhai Large Model significantly reduces the data and labor required for model fine-tuning in developing new solutions, freeing AI products from traditional 'cottage industry' models. Meanwhile, leveraging its accumulated expertise in smart healthcare and smart living, the company plans to replicate its 'industry large model + agent platform + scenario solution' model across more high-value fields, achieving a leap from standalone projects to platform-based, large-scale deployments.

According to East Money Choice data, from 2020 to 2025, Unisound invested a cumulative R&D expenditure of RMB 1.6017 billion, with annual investments of RMB 189.3 million, RMB 188.2 million, RMB 287.1 million, RMB 286.3 million, RMB 370.1 million, and RMB 380.7 million, respectively.

From technical platforms to foundational large models and then to multimodal large models, Unisound has progressed steadily, building solid fundamentals while maintaining technical innovation. Nearly every growth phase has aligned with industry hotspots, giving it the confidence to leap toward 2.0.

3

Soaring Large Model Revenue

Accelerating the 'Vertical-Horizontal' Flywheel

Operationally, Unisound has established a closed-loop from technological R&D to commercial applications, implementing a 'one vertical, one horizontal' dual-drive strategy—vertically deep cultivation (shēn gēng) in smart healthcare and horizontally expanding into smart living. In 2025, large model business revenue soared by 1,076% year-on-year to RMB 610 million, accounting for over 50% of total revenue and becoming its core income source.

Focusing on smart healthcare, a key sector since 2016, Unisound leverages speech recognition, natural language understanding, and clinical knowledge graphs. Relying on its 'industry large model + agent platform + scenario solution' approach, it provides AI solutions such as medical record voice entry, intelligent quality control, medical insurance review, and clinical decision support to hospitals, medical insurance, and health commission institutions.

By the end of 2025, its products had been deployed at scale in nearly 450 hospitals nationwide, covering approximately 35% of China's A++ and higher-tier hospitals. Its medical knowledge graph had accumulated over 10.02 million medical relationships and 5.19 million medical terms, providing crucial support for medical large model iterations. In 2025, healthcare-related revenue reached RMB 240 million, up 22.3% year-on-year, accounting for 20.1% of total revenue.

Among these, the medical record entry and generation product stood out: integrating voice hardware, foundational large models, and medical large models across three technical layers, it accurately extracts key information from natural doctor-patient conversations and rapidly generates structured medical records. For example, at Beijing Friendship Hospital affiliated with Capital Medical University, the product increased medical record generation volume tenfold at a single campus in 2025.

Along the 'hospital-insurance-regional healthcare' value chain, Unisound accelerated its application boundaries. In 2025, hospital-derived medical business revenue grew approximately 3.9 times, with 'insurance + regional healthcare' business surging over fourfold. On the medical insurance side, the company secured the nation's first provincial-level medical insurance large model project—Jiangsu Province's medical insurance large model—and collaborated with health commissions in Shijiazhuang, Zhengzhou, and elsewhere to advance medical insurance vertical large models and regional healthcare quality management. In commercial insurance, its cooperation with leading insurance groups expanded from intelligent medical reviews to disability assessments, three-phase evaluations, and other auto insurance claim risk control scenarios, boosting cost control rates to approximately 20% and increasing case processing volume via its agent platform by 37 times year-on-year.

The smart living sector also demonstrated strong growth: in 2025, sector revenue reached RMB 970 million, up 30.8% year-on-year, accounting for 79.9% of total revenue. Smart transportation performed exceptionally well. Leveraging its UniGPT-based transportation large model and Shouya agent platform, it secured the Nanning Rail Transit's full-business-domain AI project, deployed the Jinan Metro's remote intelligent customer service system, and rolled out Shanhai Large Model agent applications in over 10 cities.

In smart cockpits, Unisound deployed a 0.5B end-side intent understanding large model, serving multiple flagship models from SAIC Motor's IM Motors, Geely, and others, achieving scaling front-end mass production replication. For AI hardware, its self-developed chips and modules continued to empower leading home appliance giants like Midea, Gree, and TCL, maintaining a stable 70%+ market share in white goods voice interaction. By the end of 2025, cumulative shipments of its AI chip series had exceeded 110 million units.

From technological breakthroughs to large-scale deployments, the 'one vertical, one horizontal' strategy has acted like two interlocking flywheels, gaining momentum and increasingly becoming the core engine of Unisound's industrial intelligence transformation.

4

Three Concerns

Anyone with a Dream Is Remarkable

Yet, as the saying goes, no person or company is perfect. Looking at Unisound, several concerns linger, adding uncertainty to its 2.0 ascent.

First, it remains mired in losses, with profitability a pressing question. From 2022 to 2025, revenue steadily climbed from RMB 600.6 million to RMB 1.211 billion. However, net losses attributable to parents were RMB 366 million, RMB 375 million, RMB 454 million, and RMB 327 million, respectively, totaling RMB 1.522 billion in four years. Commercialization must accelerate further to achieve scale effects and cover soaring operational costs.

Second, persistent operating cash outflows and high debt levels warrant caution against funding pressures. From 2022 to 2025, net cash flows from operating activities were outflows of RMB 166 million, RMB 284 million, RMB 319 million, and RMB 213 million, respectively, totaling RMB 982 million in outflows. This indicates that its core business has yet to form a self-sustaining 'blood-making' cycle, relying heavily on external financing for daily operations.

From 2022 to 2025, the debt ratios of Unisound were 435.99%, 308.11%, 354.9%, and 55.64%, respectively. The figure for 2025 has significantly decreased due to the listing and financing, but upon closer examination, it still cannot be considered easy:

As of the end of 2025, the company had cash and cash equivalents of RMB 341 million, while its short-term borrowings for the same period stood at RMB 337 million. Adding in the trade and other payables of RMB 359 million for the same period, the funding gap is clearly visible.

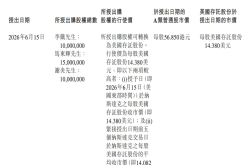

Furthermore, frequent financing efforts have put pressure on the stock price, leading to a break below the issue price. In June 2025, Unisound listed on the Hong Kong Stock Exchange, raising a net amount of approximately HKD 237 million through its IPO. Entering 2026, it successively initiated three rounds of placement financing. On January 22, it completed its first placement of new H shares, issuing 780,000 shares at a placement price of HKD 252 per share, raising a net amount of approximately HKD 192 million. On February 9, it completed its second placement, issuing 1,008,000 shares at a placement price of HKD 310 per share, raising a net amount of approximately HKD 307 million. On May 28, it announced the initiation of its third placement, issuing 1.7 million shares at a placement price of HKD 228 per share, representing a 19.89% discount to the closing price of the previous day, and raising a net amount of approximately HKD 381 million.

The total net amount raised from the three placements is approximately HKD 880 million, which is 3.71 times the net amount raised from the IPO. For a secondary new stock listed for less than a year, the scale of 'replenishing blood' from the secondary market far exceeds that from the primary market, which is rare in the Hong Kong stock market. It inevitably raises questions about the size of the company's funding gap and whether it affects investor confidence.

Looking at the trend of placement prices, the expectations are not overly demanding. The first placement was at HKD 252, and the second rose to HKD 310, indicating that the market still had some confidence at that time. However, the third placement was directly discounted to HKD 228, representing a nearly 20% discount to the closing price of the previous day.

As of June 17, the company's stock price was HKD 165.9 per share. Based on this calculation, investors who participated in all three rounds of placements have all incurred paper losses. The market capitalization is less than HKD 12.4 billion, representing a cumulative shrinkage of nearly 20% from the issue price of HKD 205.

A review reveals that Unisound's narrative for its 2.0 phase is full of highlights but also carries significant burdens. It is both timely and urgent. From boosting profitability to lifting the stock price, aiming to shine again as the 'pioneer' and embarking on a new journey of value creation, there are still tough battles to be fought.

Fortunately, judging from the release of the large model U2, the direction of effort is correct. The rest will then be left to time and patience.

Whether it's smart healthcare or smart living, both are grand narratives. Eliminating drawbacks, embracing renewal, and embarking on the 2.0 journey, everything is just beginning, and there is still time. With dreams, anyone can achieve greatness!

This article is original to Shoucai.

-

![]()

Duan Yongping Offers Insightful Perspectives: New Hurdles for Long-Term AI Investment

-

![]()

Chinese New Energy Vehicle Design: Stepping Out of the Shadows

-

![]()

Li Auto Awards Executives 35 Million Shares Based on Performance Metrics

-

![]()

Rushing Towards AI 2.0: How Confident is Unisound?

-

经过今年上半年各路AI豪强对市场的反复教育,有一个判断,可能决定未来一两年的走向:

-

![]()

Global Tech Sector Sees Collective Panic: Is the AI Hype Finally Deflating?

-

![]()

Three Consecutive Rises in Heavy Truck Sales: Both New and Old Players are Betting on the Same Thing!

-

![]()

Why Can’t Vivo Bridge the High-End Perception Gap Despite Support from Authoritative Media?