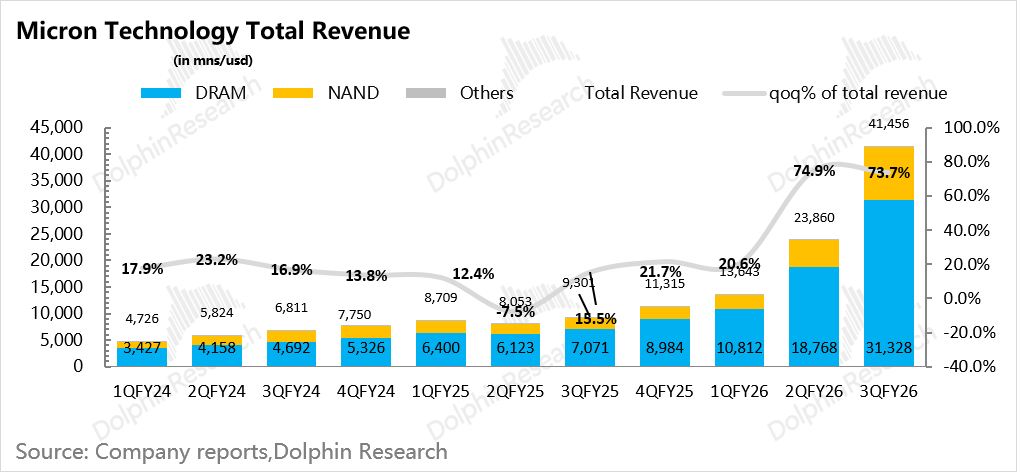

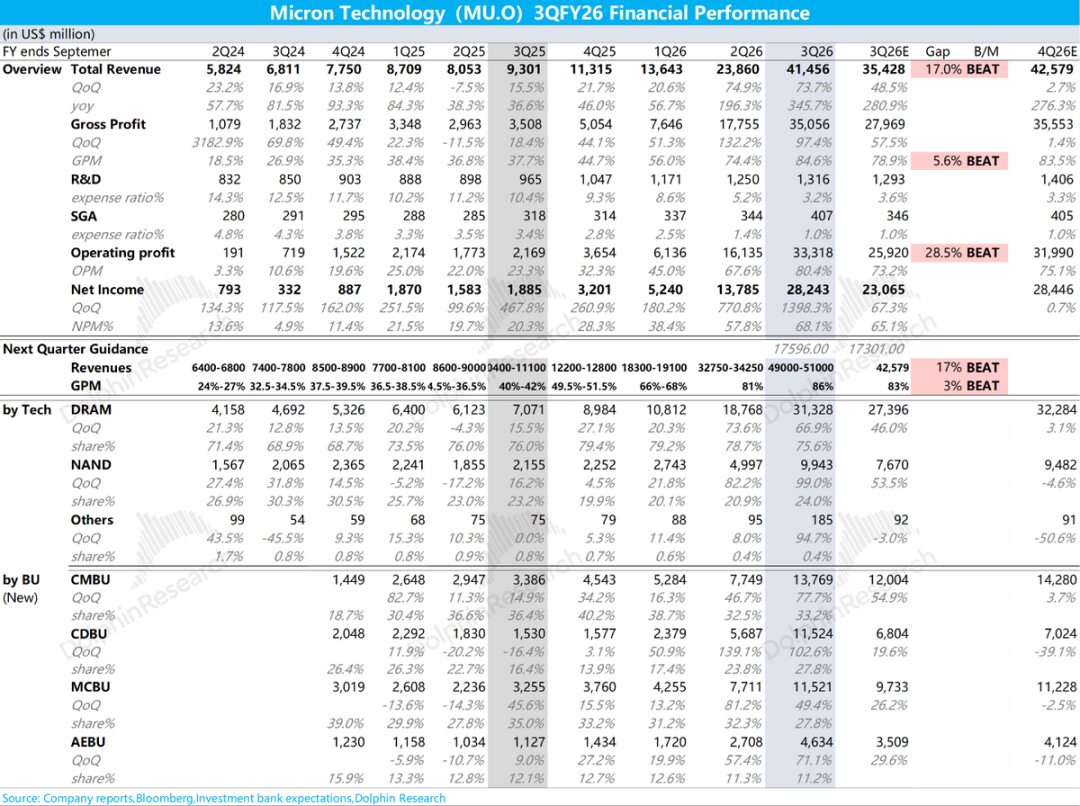

Micron has released its financial report, showing revenues of $41.5 billion, a 74% increase quarter-over-quarter, with a gross margin of 84.6%. The company provided both short-term and long-term guida

06/25 2026

06/25 2026

460

460

Key points are as follows:

1. Overall Performance: Micron's revenue for the quarter was $41.5 billion, a direct increase of 74% quarter-over-quarter, maintaining growth of over 70% for two consecutive quarters. This far exceeds the company's previous guidance of a maximum of $34.2 billion and market expectations of $35.4 billion.

When providing guidance, shipment volumes are largely determined, with flexibility primarily depending on price factors. The significant difference between expectations and guidance suggests that even industry leaders are unsure how intense market demand will be.

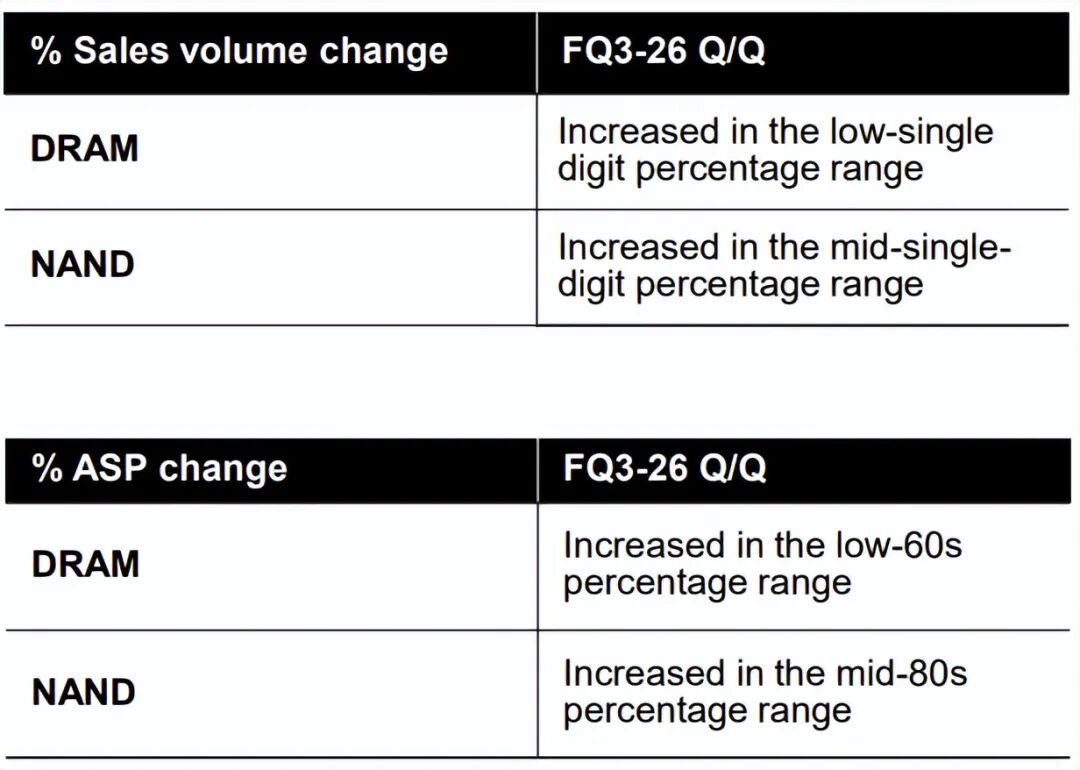

The relationship between volume and price is straightforward: shipment volumes are increasing 'at a snail's pace'—DRAM seeing low single-digit growth and NAND mid-single-digit growth quarter-over-quarter; prices have gone wild—DRAM unit prices increased by over 60%, and NAND by around 85%. The significance of this data is clear: in this unprecedented super cycle for memory stocks, everything except capacity is negligible.

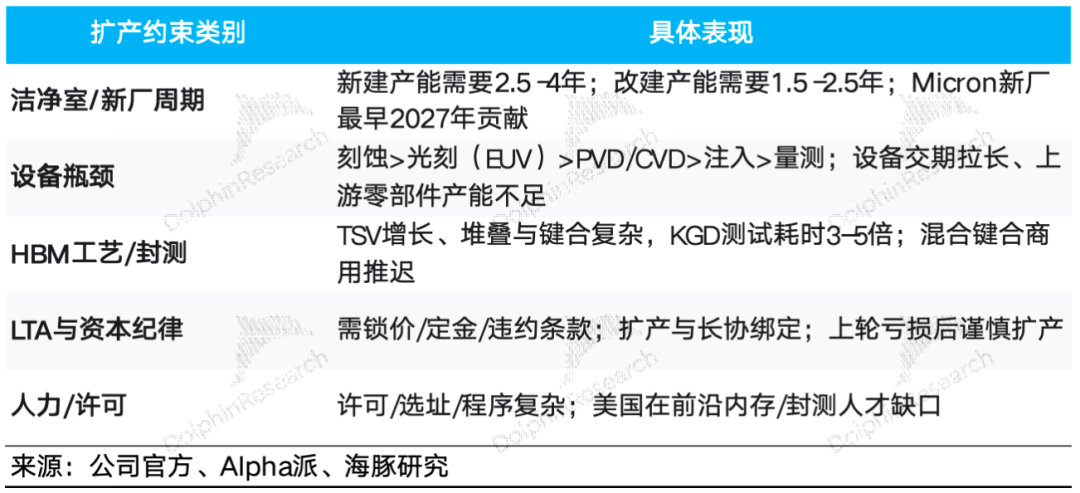

Who can secure clean rooms that meet standards (2.5-4 years for new construction, 1.5-2.5 years for renovations)? Setting aside the willingness of the three major memory manufacturers, physical constraints have become a critical bottleneck!

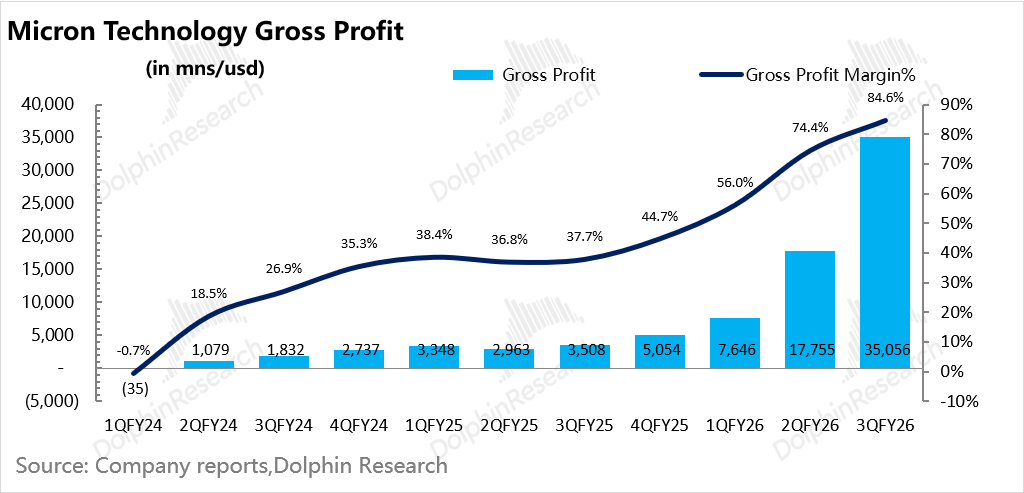

Gross Margin: Reaching new heights! With an 84.6% gross margin, Micron is a cash-generating machine! Under the current revenue-driven structure, the gross margin is a byproduct, as revenue growth is primarily driven by price increases, with marginal delivery costs nearly zero. Thus, nearly all new revenue translates into new gross profit. This quarter, the conversion rate of new revenue to new gross profit reached 98%.

2. Solid Short-Term Guidance: Equally impressive is the company's guidance, with revenue projections at $42.6 billion and EPS at $31. These projections exceed expectations based on this quarter's performance. In terms of sequential growth, the revenue guidance implies a 20% increase, aligning with market expectations. With most new revenue likely turning into profit, the new revenue guidance implicitly includes EPS expectations.

The company's EPS projection of $31 matches the current most optimistic market expectations. Given the uncertainty around future price increases, the short-term guidance allows some room for error, likely to exceed expectations. Under such guidance, market optimism is expected to rise further.

3. Confident Long-Term Guidance: The company has extended the period of tight supply-demand conditions beyond 2027, suggesting that even if conditions begin to ease in 2028, it will be difficult to predict when supply will truly meet demand. This implies that supply-demand imbalances may become a structural issue for an extended period, warranting a reevaluation of valuation multiples!

4. The core factor supporting this valuation shift is strategic long-term agreements: The first five-year agreement was signed last quarter. Now, there are 16 strategic agreements in place. Acknowledging this as a key concern for the market in structurally revaluing the company, Micron provided detailed explanations:

a. Client Structure: Covering three major end markets—data centers, consumer electronics, and automotive; client composition: 4 hyperscale clients + 3 medium-sized clients, with the rest being small and medium-sized clients in the automotive industry.

The company specially (deliberately) pointed out that securing so many long-term agreements so quickly is primarily because clients value their 'U.S. production capacity' attribute, aligning with the market's logic of assigning them a premium. Among the three memory giants in the AI era, while SK Hynix and Samsung may have more advanced capacity and technology than Micron, Micron is the rare 'Made in the USA' darling that Trump cherishes.

b. Duration: Typically 5 years (from the 2026 calendar year to the end of 2030); automotive agreements generally last 3 years.

c. Key Contract Terms:

'Take or pay' provisions; significant penalties for client default; large agreements have upper and lower limits, with price caps for existing products set at current Q2 market prices and price floors in effect throughout the contract term. Other agreements follow market prices; pricing for new-generation products (e.g., HBM4, DDR6) to be negotiated in the future, not fully locked in;

d. Financial Implications:

4 agreements generate cumulative revenues of approximately $100 billion at contract minimum prices; signed agreements bring in about $22 billion in cash deposits and related financial commitments; price floors support gross margins well above historical peak levels; upon full execution, agreements with fixed or capped prices near current CQ2 market prices will account for about 40% of total revenue. After all planned SCAs are executed, it is expected that about half or more of Micron's revenue will fall under the SCA framework.

From Dolphin Research's perspective, while the four major agreements guarantee only $100 billion in revenue at minimum prices, amounting to $20 billion annually over five years, this represents a guaranteed floor during potential downturns, determinism (deterministically) raising the bottom during cyclical lows.

Additionally, Micron has secured $22 billion in performance guarantees, strengthening its risk resistance against client defaults. Although these funds cannot be used for capital expenditures, they alleviate market concerns about the 'cyclical fate' of memory stocks—expanding during booms and wasting capacity during busts, erasing profits made during good times.

With this detailed explanation, is the next phase of revaluing memory stocks upon us? After all, thus far, memory stock prices have primarily been driven by EPS.

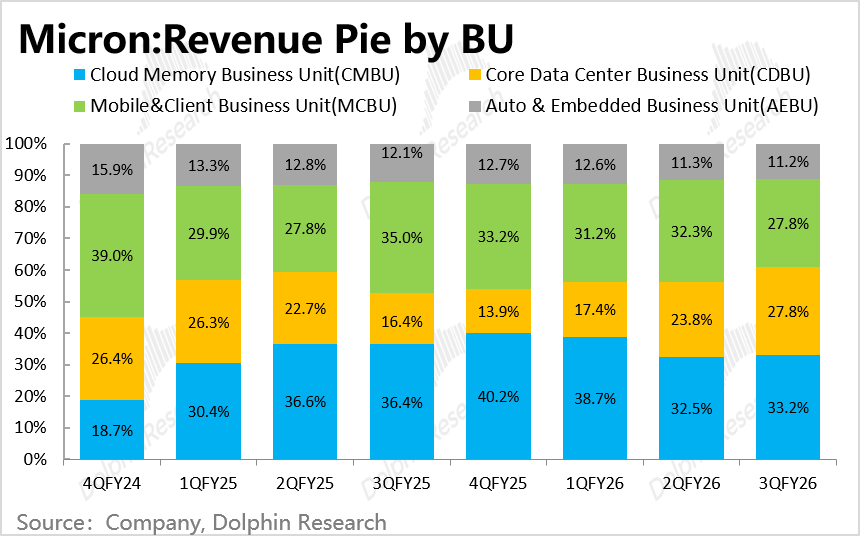

4. Price Surge: DRAM revenue reached $31.3 billion, a 67% increase quarter-over-quarter, with over 60% driven by price hikes; NAND revenue was $9.9 billion, a 99% increase, with unit prices surging by around 85%. Clearly, such price increases are only possible when demand soars and capacity cannot be released shortly.

In terms of revenue by segment, core data center revenue representing AI scenarios increased by 103% quarter-over-quarter to $11.5 billion, exceeding expectations the most. The market still underestimates the frenzy of AI data centers; traditional cloud storage also saw a 78% increase due to price hikes across specifications, but revenue of $13.8 billion will soon be overtaken by core data center business.

Even the worst-performing segments, mobile and PC storage, saw growth of nearly 50% quarter-over-quarter, putting pressure on the gross margins of mobile and PC manufacturers.

Moreover, due to HBM's larger chip size, complex stacking, lower yields, and heavier packaging and testing requirements, the Trade Ratio for replacing traditional DRAM capacity with HBM is as high as 2.5-3 times, squeezing out traditional capacity and prolonging supply-demand mismatches for traditional products.

More importantly, despite HBM's high unit prices, its gross margins remain low. When supply tightness shifts to traditional DRAM and NAND, their gross margins will be higher.

Memory manufacturers have explicitly stated that non-HBM DRAM gross margins exceed those of HBM. Some outsiders estimate that, on a per-wafer basis, conventional DRAM generates twice the revenue and three times the gross profit compared to HBM.

The persistent supply-demand imbalance in traditional products brings memory manufacturers significantly greater profit elasticity than the pure incremental benefits of HBM.

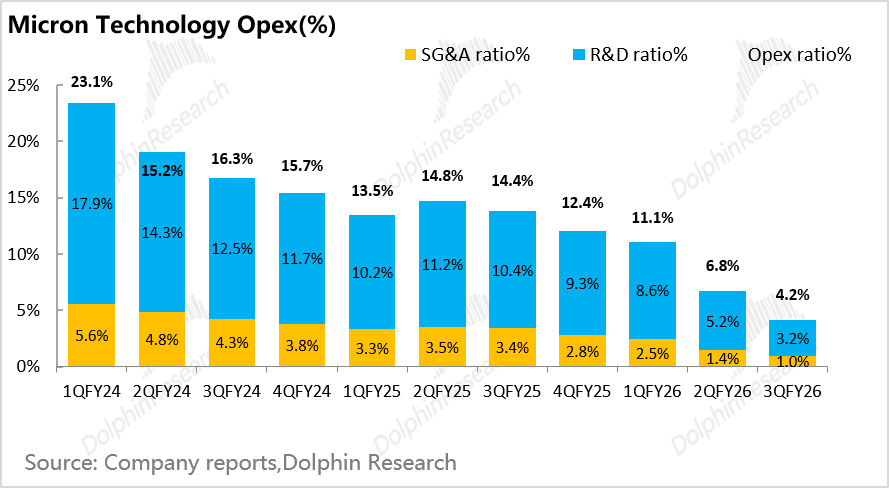

5. Extreme Operating Leverage: Compared to the surge in revenue, expenses have increased minimally, similar to memory shipment volumes. Research and development expenses, the largest component, increased by only 5% quarter-over-quarter, while selling and administrative expenses rose by 18%—negligible compared to the 74% revenue increase.

With extreme price increases and ample operating leverage, the company's operating profit reached $33.3 billion, with a profit margin of 80%! A veritable money tree, leaving even NVIDIA in awe.

6. Capital Expenditures: The market fears that impulsive capacity expansions in this memory cycle will erode profitability during downturns, raising concerns about rapidly rising capital expenditures.

However, after reviewing the details, Dolphin Research can only say: Don't panic, capital! This time, physical constraints are killing the urge to expand, leaving money unspent!

This quarter, the company's capital expenditures, excluding government subsidies ($700 million), were $7.1 billion, with plans for $10 billion next quarter. Capital spending per quarter in the new fiscal year 27 will remain above $10 billion. For comparison, operating cash flow this quarter was $25.4 billion—plenty of cash on hand.

The company specifically noted that over half of the new capital expenditures will be for 'construction expenses,' meaning advancing clean room construction rather than simply purchasing equipment. Additionally, the company disclosed a multi-year EUV supply agreement with ASML to support the advancement of the 1δ process and beyond.

Dolphin Research's Overall View: Is a Growth Stock Valuation Logic Emerging?

Historically, memory stocks have been standard cyclical plays, typically earning significant profits during good times, only to succumb to the urge to expand capacity, leading to low utilization rates and erased profits during downturns. Because of this, these companies have been valued as cyclical stocks, with peak earnings often coinciding with low PE ratios due to valuation caution.

Clearly, the core controversy the market focuses on and the point the company has tirelessly explained—are strategic agreements and long-term contracts. The company aims to use 3-5 year agreements, hefty client deposits, and capital expenditure budgets tied to profit ratios to reassure the market that this cycle is different!

The essence of this stringent long-term contract mechanism, from Micron's perspective, is to convert about half of its revenue into binding, price-banded, and predictable contract revenue, reducing cyclical volatility and enhancing revenue and cash flow visibility and stability. It also upgrades memory manufacturing, a commodity business, into a 'pre-manufactured' product based on prepaid contracts.

The $22 billion in deposits, in Dolphin Research's view, is the crowning touch. Even though these funds cannot be directly used for capital expenditures, they represent client money used for expansion, effectively lightening Micron's 'asset-heavy' nature to some extent.

This may slightly suppress upside during industry booms but ensures strong earnings during good times and, more importantly, raises the floor during downturns, achieving what the company calls a 'fundamental transformation of the business model.'

In the industries Dolphin Research has covered over the past two years, when commodity assets like lithium ore were touted with growth logic at prices of 600,000-700,000 yuan per ton, we were highly skeptical, as it often signaled industry mania.

However, in tracking the AI-driven super cycle of AI infrastructure over the past two to three years, our strongest takeaway has been to clear our historical 'memory' and maintain 'awe' for the nonlinear evolution of new technologies, avoiding the cliché of 'There is nothing new under the sky.'

After all, as recently as the first half of 2025, industry leaders like Micron, deeply embedded in the sector, still expected NAND inventory clearance to take some time, consistently shifting NAND capacity to HBM! Evidence from the Q3 fiscal year 25 earnings call supports this, as previously compiled and released on the Longbridge App by Dolphin Research.

Although Micron has already been a 4-bagger stock since the beginning of the year, based on current performance and guidance, its valuation stands at only 10 times. If Micron can secure more long-term agreements for various products (e.g., traditional products like NAND) and given its slower-than-expected capacity expansion, the market, once fully educated, may grant Micron some valuation premium, moving from 10X to 12X and eventually to 15X?

Moreover, Micron's financial report holds significance beyond the memory industry, offering greater upside for upstream AI capital expenditure stocks. For instance, Micron explicitly stated that it signed a long-term EUV agreement with supplier ASML. Switching to EUV reduces the need for multiple exposures, etchings, and alignments required with DUV.

In short, while the AI infrastructure era was primarily a computing power rally during the training phase, the Agentic AI era will see a comprehensive boom in AI infrastructure.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. For reprint authorization, please obtain approval.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes, intended for users of Dolphin Research and its affiliated institutions for general reading and data reference. It does not consider the specific investment objectives, product preferences, risk tolerance, financial status, or unique needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referencing the content or information in this report are at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect consequences or losses arising from the use of the data in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives but does not guarantee the reliability, accuracy, or completeness of this information and data.

The information mentioned or the viewpoints expressed in this report shall not be considered or deemed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction, nor shall it constitute advice, inquiry, recommendation, etc., regarding relevant securities or related financial instruments. The information, tools, and data contained in this report are not intended for distribution to, or for the use by, any person or entity in any jurisdiction or country where such distribution, publication, availability, or use would be contrary to applicable laws or regulations or would subject Dolphin Research and/or its subsidiaries or affiliated companies to any registration or licensing requirements within such jurisdiction.

This report solely reflects the personal viewpoints, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’