Is Momenta’s “Physical AI” Premium Justified?

07/09 2026

07/09 2026

568

568

Produced by | Intelligent Machinery Island

On the Hong Kong Stock Exchange’s digital display, the ticker 06880 flickered to life for the first time. On July 8, 2026, five companies rang the opening bell, with Momenta—the largest by scale—taking center stage.

Priced at HK$295.6 per share, it opened at HK$301, valuing the company at over HK$70 billion. The public offering was oversubscribed 414 times, with international placements attracting over HK$100 billion in institutional orders. Fourteen cornerstone investors subscribed to nearly HK$3 billion, including GIC and Fidelity International (each investing US$100 million), while Mercedes-Benz and BYD formed a rare strategic partnership to increase their stakes.

Amid a broader downturn in Hong Kong’s tech sector in 2026, this fervor stood out as a bold contrarian bet.

Yet a closer look at Momenta’s prospectus reveals a stark reality: cumulative losses exceeding RMB 9 billion over three years, with no profitability in sight. Why, then, are the world’s most discerning long-term investors doubling down on a company bleeding red?

Momenta’s origin story begins with an unconventional pivot.

In 2004, 18-year-old Cao Xudong left Gansu for Tsinghua University to study engineering mechanics. After earning his bachelor’s degree, he qualified for direct PhD admission but discovered a passion for artificial intelligence during his doctoral studies—and dropped out.

He joined Microsoft Research Asia and SenseTime, cementing his reputation in AI before founding Momenta at age 30 in 2016.

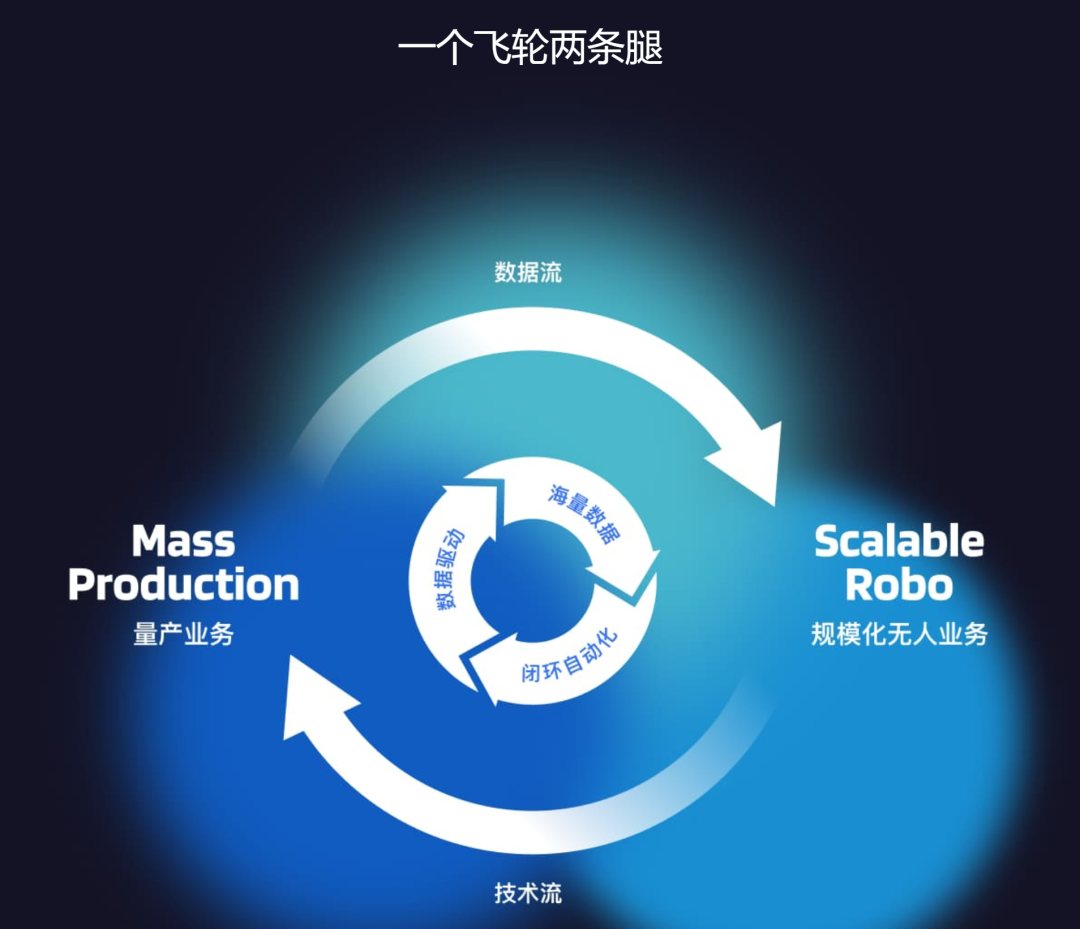

“One Flywheel, Two Legs” strategy. Source: Momenta’s official website

From the outset, Cao embraced a strategy that seemed counterintuitive: “One flywheel, two legs.”

This meant equipping mass-produced vehicles with L2+ advanced driver-assistance systems (ADAS) to collect real-world driving data, refining algorithms, and then using those algorithms to support L4-level Robotaxi deployment. At the time, the industry was obsessed with L4 autonomy, with companies showcasing demos and launching test fleets. L2 was seen as far less glamorous.

In hindsight, this “less sexy” path proved prescient. A decade later, Momenta stood on the Hong Kong Stock Exchange, branding itself as the “first physical AI stock.”

The label sparked intense debate. Horizon Robotics founder Yu Kai posted a Weibo message after Momenta’s IPO filing, stating Horizon “doesn’t play the game of being the ‘XX first stock’” and self-deprecatingly referred to his company as “rather boring.” While Yu didn’t name names, the timing and tone led many to interpret it as a veiled critique of Momenta’s narrative.

Is the “first physical AI stock” label a technical breakthrough or a carefully crafted capital markets story? Behind its HK$70 billion valuation, can Momenta’s business model justify such expectations? As automakers accelerate in-house R&D and competition intensifies, how will it defend its competitive edge?

1. Why Can Gross Margin Exceed CATL’s?

The most striking figure in Momenta’s prospectus is its gross margin.

From 2023 to 2025, it surged from 17.5% to 71.6%—a rarity in the automotive supply chain. For context, Horizon Robotics’ margin hovered around 64.5%, CATL’s at 26%, and Tesla’s automotive business at 18%.

For a company specializing in intelligent driving software to outpace a battery market leader defies traditional manufacturing logic.

According to the prospectus, Momenta’s revenue comes from two segments: technology development services and licensing. The former involves customizing solutions for automakers, billed per project with revenue tied to engineering headcount. The latter collects per-vehicle licensing fees post-mass production, with negligible incremental costs since software development costs are already sunk.

In 2023, technology services accounted for 96.8% of revenue, with licensing at just 3.1%. By 2025, technology services fell to 59.9%, while licensing rose to 40.1%—soaring from RMB 23 million to RMB 968 million, a 42-fold increase in three years.

Momenta’s licensing business follows a “one-time development, full-lifecycle reuse” model, inherently high-margin. Thus, the jump in gross margin wasn’t due to cost-cutting but a revenue mix shift.

Yet while revenue and gross profit rose, net losses widened.

From 2023 to 2025, Momenta’s net losses attributable to shareholders were RMB 2.57 billion, RMB 3.206 billion, and RMB 3.458 billion, totaling RMB 9.234 billion over three years. At first glance, this seems to negate all positive signals—how could a company with a 70%+ gross margin still lose money?

The bulk of losses stemmed from “fair value changes in preferred shares and other financial liabilities.” These are instruments issued to pre-IPO investors. Preferred shares are accounted for as liabilities, and each valuation increase enlarges this liability, recorded as a loss. In 2023, this amounted to RMB 1.19 billion; in 2024, RMB 1.968 billion; and in 2025, RMB 2.843 billion.

The more valuable the company becomes, the larger the book loss—but this doesn’t represent actual cash outflows. It’s an accounting illusion.

Excluding this and non-cash items like share-based compensation, adjusted net losses narrowed from RMB 1.093 billion to RMB 959 million over three years, then to RMB 303 million. Net operating cash outflow also shrank from RMB 1.069 billion in 2023 to RMB 281 million in 2025.

While Momenta is still unprofitable, losses are narrowing rapidly.

The real cash burn comes from R&D. From 2023 to 2025, R&D expenses were RMB 1.281 billion, RMB 1.508 billion, and RMB 1.869 billion, respectively. In 2025, R&D accounted for 77.5% of revenue, focused on three core barriers: physical AI, end-to-end autonomy, and reinforcement learning models.

2. Why Did Momenta Rebrand Before Its IPO?

Given improving operational performance, why did Momenta pivot its narrative on the eve of listing?

A overlooked timeline reveals Momenta initially planned a U.S. IPO. In June 2024, China’s securities regulator approved its filing to issue up to 63.35 million ordinary shares on NASDAQ or the NYSE, positioning it as an “intelligent driving solution provider.” However, that filing expired in June 2025, and the U.S. listing was shelved.

In March 2026, Momenta quietly submitted its Hong Kong prospectus. When it reemerged, it had adopted the “first physical AI stock” title. At the Beijing Auto Show in April, it unveiled its R7 reinforcement learning world model and systematically introduced “physical AI” to the public.

The timing aligned with peak enthusiasm for the concept.

In July 2025, NVIDIA CEO Jensen Huang declared “physical AI is the next wave of growth.” At CES 2026, he devoted a 90-minute speech to proclaiming “the ChatGPT moment for physical AI is approaching.” Market fatigue with “intelligent driving” contrasted sharply with excitement over “physical AI.”

Peer performance clarifies the rationale. Pony.ai and WeRide broke below their IPO prices, with market caps now just over HK$20 billion and HK$10 billion, respectively. Horizon Robotics’ stock halved from its peak, at one point falling below its IPO price—signaling waning patience for the “intelligent driving” label.

Listing as an “intelligent driving provider” would have forced the market to value Momenta purely on performance, limiting imagination. The “physical AI” narrative elevated it from “a supply chain link” to “an AI infrastructure layer,” shifting valuation logic from “a company selling algorithms” to “a platform defining the next computing paradigm.”

GIC, Fidelity, and BlackRock’s willingness to bet big on an unprofitable company hinged on this story.

Meanwhile, Momenta priced its IPO at HK$295.6 per share, valuing it post-issue at HK$69.6 billion (~US$9 billion). Based on 2025 revenue of RMB 2.413 billion, this implies a price-to-sales ratio of ~25x.

For comparison, Horizon Robotics’ market cap is ~US$7.58 billion, and Pony.ai’s ~US$3.017 billion—both below Momenta’s valuation. As a “physical AI” company, Momenta already trades at a premium to all listed intelligent driving peers.

This premium reflects the market’s choice between two valuation logics.

Momenta Introduction. Source: Momenta’s official website

While a company can label itself, market acceptance depends on substance. Momenta’s “first physical AI stock” claim gained traction due to its real-world foundations: data scale, technological execution, and commercial closure.

Data Scale: Physical AI requires machines to understand the physical world, demanding exposure to vast real-world samples. By end-2025, vehicles equipped with Momenta’s systems exceeded 900,000 units, accumulating over 12 billion kilometers in driving mileage. These vehicles act as roaming data collectors—a capability pure L4 companies struggle to match.

Technological Execution: In April 2026, Momenta mass-produced its R7 reinforcement learning world model, becoming the first third-party intelligent driving company to achieve nationwide mapless urban NOA, end-to-end large model mass production, and reinforcement learning model mass production. While most physical AI players remain at lab demo stages, R7 was already deployed in vehicles.

Commercial Closure: Cao Xudong advocates a “ticket theory,” arguing that general-purpose physical AI requires a cash-flow business. Momenta’s L2++ mass production provides revenue and real-world data, while its L4 autonomy validates technological limits and feeds back into mass production. Autonomous driving is the only physical AI scenario achieving both data and commercial scaling, and Momenta has closed the loop from data to models to monetization.

Judging by its debut, the market gave Momenta a vote of confidence. Its stock opened over 6% higher, valuing it at over HK$70 billion.

3. Why Did Horizon Robotics Feel Compelled to Respond?

The most intriguing episode of Momenta’s listing wasn’t its circuitous path to going public but Horizon Robotics founder Yu Kai’s Weibo post.

Yu wrote: “ isnHorizon’t good at playing the ‘XX first stock’ game and is a rather boring company.” That afternoon, he commented under a netizen’s post: “It’s not that we’ve softened; we’re just busy serving clients and don’t have time for stock prices.”

Horizon Robotics founder Yu Kai’s critique. Source: Yu Kai’s personal Weibo

The tension between the two companies is rooted in shifting competitive dynamics. Once misaligned, their rivalry now centers on clashing business models within the same market.

Horizon Robotics began with chips.

Founded in 2015, it focused on automotive-grade AI chips. Its Journey series chips are its core products, with shipments exceeding 4 million units in 2025, up 39% year-over-year. Shipments of chips supporting mid-to-high-level intelligent driving functions reached 1.8 million units, nearly five times the 2024 figure, accounting for 45% of total shipments. By August 2025, cumulative Journey series shipments surpassed 10 million units.

The chip business is characterized by deep integration into a vehicle’s electrical architecture once adopted, with extremely high switching costs. Even if automakers develop in-house algorithms, replacing a widely deployed chip platform is difficult. This “physical locking” effect constitutes Horizon’s core moat.

In 2025, Horizon’s full-year revenue was RMB 3.76 billion, up 57.7% year-over-year, with a gross margin of 64.5% (67.2% for automotive business). Revenue comprised two segments: product and solution revenue at RMB 1.622 billion, up 144.2% year-over-year (rising from 28% in 2024 to 43% of total revenue), and licensing and service revenue at RMB 1.935 billion, up 17.4%.

Notably, the licensing business had a gross margin of 94.5%, serving as Horizon’s stable profit source, while product solutions had a margin of just 34.5%. In essence, Horizon uses chips to gain market access and software licensing to generate profits—chips as the gateway, software as the profit engine.

The challenge with this business model stems from its low hardware profit margins and substantial R&D investment. By 2025, Horizon Robotics' R&D expenditure had soared to RMB 5.154 billion, marking a 63.3% year-on-year increase and accounting for a staggering 137.1% of its revenue. Consequently, its adjusted operating loss widened to RMB 2.372 billion, up 58.7% from the previous year. Essentially, the company found itself in a situation where it was "investing roughly RMB 1.37 in R&D for every RMB 1 earned in revenue."

In contrast, the differences in Momenta's business model become more apparent.

Momenta began with algorithms and gradually expanded into hardware. As previously analyzed, Momenta's core assets lie in data and software, with its competitive advantage being the data flywheel effect: more vehicles on the road generate more data; more data strengthens the models; stronger models, in turn, attract more partnerships with automakers.

Simply put, Horizon Robotics' competitive edge is hardware-based: once its chips are installed in vehicles, they are difficult to replace, effectively locking automakers into its ecosystem. Conversely, Momenta's strength is data-driven: newcomers cannot easily replicate the data accumulated from 1 million vehicles, as its barrier is built on the data flywheel—automakers using Momenta's solutions benefit from continuous algorithm upgrades.

4. Horizon Robotics and Momenta Are Converging

Horizon has expanded its scope from chips to algorithms.

In November 2025, Horizon's all-scenario urban assisted driving solution, HSD, officially entered mass production. By early 2026, HSD had secured designated cooperation with 10 automakers for over 20 vehicle models. The first models equipped with HSD, the Exeed ET5 and Seres L06, saw more than 25,000 activations of their intelligent driving features within just eight weeks of launch. Yu Kai projects that by the end of 2026, approximately 20 models equipped with "Journey + HSD" will have been delivered cumulatively.

HSD V2.0, released in June 2026, features model upgrades based on world models and end-to-end reinforcement learning. During an earnings call, Yu Kai revealed that the top-tier versions of models equipped with HSD accounted for 83% of sales, with intelligent driving mileage making up 41%. He views the 41% milestone as the eve of a strategically significant turning point.

This signifies Horizon's transformation from a chip seller to a provider of intelligent driving solutions—a market traditionally dominated by Momenta.

Introduction to Horizon's Business, Image Source: Horizon's Official Website

Momenta is also encroaching on Horizon's territory. In April 2026, Momenta announced that its first jointly developed self-research chip, the X7, had been integrated into SAIC Volkswagen's ID.ERA 9X. Momenta is transitioning into a provider of integrated hardware-software solutions.

Yu Kai claims Horizon is both a software algorithm company that best understands chips and a chip company that best understands software algorithms. The same applies to Momenta, albeit in reverse.

The fiercest battleground for both companies is a shared client: BYD.

Momenta serves as the core algorithm provider for BYD's "Divine Eye" solution, offering algorithmic support on NVIDIA chips. BYD is also one of Momenta's cornerstone investors for its IPO, contributing $15 million.

Horizon supplies BYD with its Journey series chips, with an estimated 2.5 million Journey 6 chips expected to be shipped to BYD in 2025. The Journey 6M and the cockpit-driving fusion chip, Xingkong, can save RMB 1,500 to 4,000 in hardware costs per vehicle.

However, both companies face a common threat: BYD's in-house R&D efforts.

On May 28, 2026, BYD unveiled its self-developed 4nm intelligent driving chip, Xuanji A3, boasting over 700 TOPS of computing power. Horizon's stock price fell more than 7% the following day.

In the long run, as BYD's self-developed capabilities expand across all price segments, the market share for both Momenta and Horizon within BYD's ecosystem will shrink.

This dilemma is not unique to BYD. SAIC holds a 9.45% stake in Momenta while signing a deep cooperation agreement with Huawei and continuing to invest in self-developed technologies. Mercedes-Benz is both a shareholder and cornerstone investor in Momenta while ramping up its own R&D investments.

An increasing number of leading automakers are adopting a dual-track strategy of "self-developed + outsourced" solutions, continuously squeezing the bargaining power of third-party suppliers.

Meanwhile, from a competitive standpoint, the battlefield is shrinking. Remarkably, Yu Kai and Cao Xudong share strikingly similar visions for the industry's endgame.

In October 2025, Cao Xudong publicly stated that the competition for assisted driving would conclude in 2026, with only three domestic players surviving. Yu Kai, at a shareholders' meeting in June 2026, predicted that autonomous driving would become standard in vehicles by 2030, with Horizon achieving $1,000 in profit per vehicle through its chip-software combination.

Both companies believe they will be among the final contenders.

Over the past two to three years, nearly a dozen autonomous driving-related companies have gone public, all trading below their IPO prices. Every industry undergoes two phases: dream-building and delivery. During the dream-building phase, capital markets assign high expectations and valuations; in the delivery phase, the focus shifts to revenue growth, gross margins, and market competitiveness.

Momenta is entering its delivery phase, while Horizon is already deep in it. Both must prove they can not only survive but thrive in this phase.

Yu Kai's veiled jab at the "first mover" on Weibo, while seemingly emotional, reflects a clear-eyed recognition of shifting competitive dynamics. A showdown between Horizon and Momenta is inevitable, and the winner will be the first to cross the finish line in a market reduced to just two or three players.

V. The World Model Hype: Solving Old Problems with New Labels

The "world model" is arguably the hottest and most chaotic term in AI in 2026, becoming the new universal label in the field—much like the metaverse or large language models in previous years. Affixing this label guarantees entry into the capital and media spotlight.

The fact that the same company and technology, when labeled as the "first physical AI unicorn," can command a 25x price-to-sales ratio speaks volumes.

So, what role does the world model play in the autonomous driving technology stack?

A widely accepted view is that world models in today's intelligent driving industry represent technological paradigm upgrades to existing simulation tools. They aim to resolve end-to-end model testing and validation issues in virtual worlds with higher fidelity, richer scenarios, and greater freedom.

Leading players are largely developing world models as simulators. Li Auto uses its Driving World Model as a scoring teacher, while XPENG employs world models for simulation testing to evaluate new model algorithm capabilities.

A crucial distinction exists: using world models for simulation versus using them to understand the physical world are two different endeavors.

The former is a tool-level improvement. A more realistic simulation environment accelerates model iteration but does not require the model itself to understand physical laws. As long as the simulation is authentic, the test results hold value.

The latter is a capability-level advancement. It requires onboard models to genuinely comprehend physical laws—such as object inertia, how road friction coefficients affect braking distance, or that pedestrians might run into the street when a ball bounces toward them. This demands continuous real-world driving learning, far beyond what simulation environments can provide.

Currently, nearly all industry players developing world models focus on the former issue. They are building better simulators, not AI that truly understands the physical world.

This explains why world models from leading players function similarly, all claiming capabilities in scenario generation, closed-loop simulation, and reinforcement learning training—because they address the same engineering challenge.

Momenta's R7 World Model pushes this framework further with a three-tier architecture: a world model pre-training layer compressing physical laws, a simulation layer for deducing long-tail scenarios, and a reinforcement learning layer for autonomous decision optimization. Momenta claims R7 has optimized false braking by over 3x and improved in-lane avoidance performance nearly 5x.

However, R7's core innovation—introducing reinforcement learning into world model training—is not unique to Momenta.

NIO rolled out its "world model + closed-loop reinforcement learning" architecture to hundreds of thousands of vehicles in January 2026. Qcraft also launched a solution based on a unified world model + reinforcement learning architecture. Huawei's ADS 5 WEWA 2.0 architecture incorporates online reinforcement learning.

Momenta's R7 aligns technologically with peers; the difference lies in timing and scale of mass production.

Thus, world models face an intriguing paradox: the greater their value, the lower their scarcity.

When everyone pursues the same goal, the technology itself ceases to be a barrier. The true differentiators become who has more data, larger production scales, and stronger engineering capabilities.

This circles back to Momenta's original competitive edge: 1 million mass-produced vehicles and a 65% market share in third-party urban NOA. The world model is a new narrative to package this advantage, not a replacement technology.

Image Source: AI-Generated

Another notable trend is the industry's shift from debating world models to discussing their implementation.

In 2025, the rivalry between VLA and world model routes dominated industry discourse. By late 2026, growing voices acknowledged that both approaches could converge. As technical routes shifted from "either-or" to "both," the differentiated value of world models further diluted.

While world models undoubtedly represent a critical direction for autonomous driving technology, the journey from academic concept to tangible user experience remains long.

For Momenta, the "first physical AI unicorn" label provides a higher starting point than its intelligent driving peers. However, whether world models can evolve from a marketing concept into a genuine technological moat depends on its ability to prove itself through data, products, and users.

VI. Conclusion

Momenta's stock opened over 6% higher, briefly surpassing a HK$70 billion market cap. The rally faded by afternoon, closing flat at HK$295.6, matching its IPO price.

The gap between the morning surge and afternoon decline mirrors market ambivalence: willing to pay a premium for the "first physical AI unicorn" narrative but reassessing its validity over a single trading day.

Narratives must eventually deliver. The physical AI story's credibility hinges on three factors: data scale, model capability, and commercialization speed.

At the listing ceremony, Cao Xudong stated, "Over the past decade, we've taught AI to drive. In the next decade, we'll bring dedicated robots—nannies, doctors, teachers—to every household."

This vision is grand, but the decade-long timeline feels prolonged for a publicly traded company answering to quarterly markets.

Momenta starts with a higher benchmark than its peers: a $9 billion valuation and 25x price-to-sales ratio.

Yet this benchmark is also a higher hurdle. Post-IPO, the market will demand answers: What has physical AI changed? Is it merely a technical architecture upgrade, or a business model transformation?

Momenta's ticket is genuine, and the physical AI direction is real. But whether the "ChatGPT moment" for physical AI has truly arrived depends on Momenta's ability to establish irreplicable differentiation as everyone rushes toward the same goal.

Cover Source: The Truman Show

Header Image Source: Momenta's Official WeChat Account

Copyright ZhiXie Island. All rights reserved. No reproduction without authorization.

-

![]()

Emerging Leaders Surge Ahead, While Others Grapple with Challenges|Mid-Year Review ①

-

![]()

BYD Executive Sheds Light on Electric Vehicle Wading Prowess: Theoretical Edge Over Fuel Cars, Yet Battery Seal Integrity Is Key

-

![]()

Zhipu Stages a 'Deep V' Turnaround on Lock-up Expiry Day: Can the 'Pioneer Large Model Unicorn' Maintain Its Edge?

-

![]()

Switch Transition from Copper to Optical: From 500 Wafers to a $10 Billion Market

-

![]()

Fuel Vehicle Pricing System Undergoes Severe Stress Test: Unraveling the Root Causes

-

![]()

Xiaomi Steps into Car Manufacturing, Embracing 'Extended Range' Strategy

-

![]()

Next-Gen 13-inch Surface Pro Review: Huge Improvements in Performance and Energy Efficiency, Integrated Graphics Rival Latest X86

-

![]()

SpaceX: Space Computing Power - Musk's New Vision or Real Future?