What’s the Status of AR Glasses Commercialization?

04/05 2026

04/05 2026

547

547

As a leading contender for the "next-generation computing terminal," AR glasses have been in the limelight for nearly a decade. They’ve ridden the wave of metaverse hype, witnessed Apple’s high-profile launch of VisionPro—which set the industry’s course toward spatial computing—and seen domestic tech giants join the fray in recent years.

Yet, amid this sustained excitement, the industry has lacked publicly available financial data to gauge true commercialization progress.

That changed on April 1st when XREAL—dubbed the "world’s No.1 in AR glasses shipments"—officially submitted its prospectus, offering a crucial case study for assessing the AR glasses sector’s commercialization.

From launching its first consumer-grade product in 2019 to capturing the top global market share by 2025, XREAL has navigated a seven-year journey from tech exploration to规模化 expansion. However, the prospectus reveals persistent losses, heavy reliance on hardware sales, and dependence on overseas markets—challenges that reflect broader industry dilemmas.

Is the AR glasses business sustainable? The XREAL case may provide clues.

I. Commercialization Breakthrough: Strong Sales, Yet Persistent Losses

Founded by Chi Xu in 2017, XREAL counts him as its largest shareholder, holding a combined voting stake of 27.98%. Prior to XREAL, Chi Xu worked at NVIDIA and Magic Leap, contributing to optical display technology development.

Within two years of its founding, his team developed the world’s first consumer-grade AR glasses.

Today, XREAL’s product lineup spans three tiers: the entry-level Air series targets high-frequency scenarios like immersive movie-watching and mobile productivity; the mid-range One series enhances display and interaction capabilities; and the premium Light-Ultra-Aura line offers cutting-edge features like 6DoF interaction and spatial awareness for developers and power users.

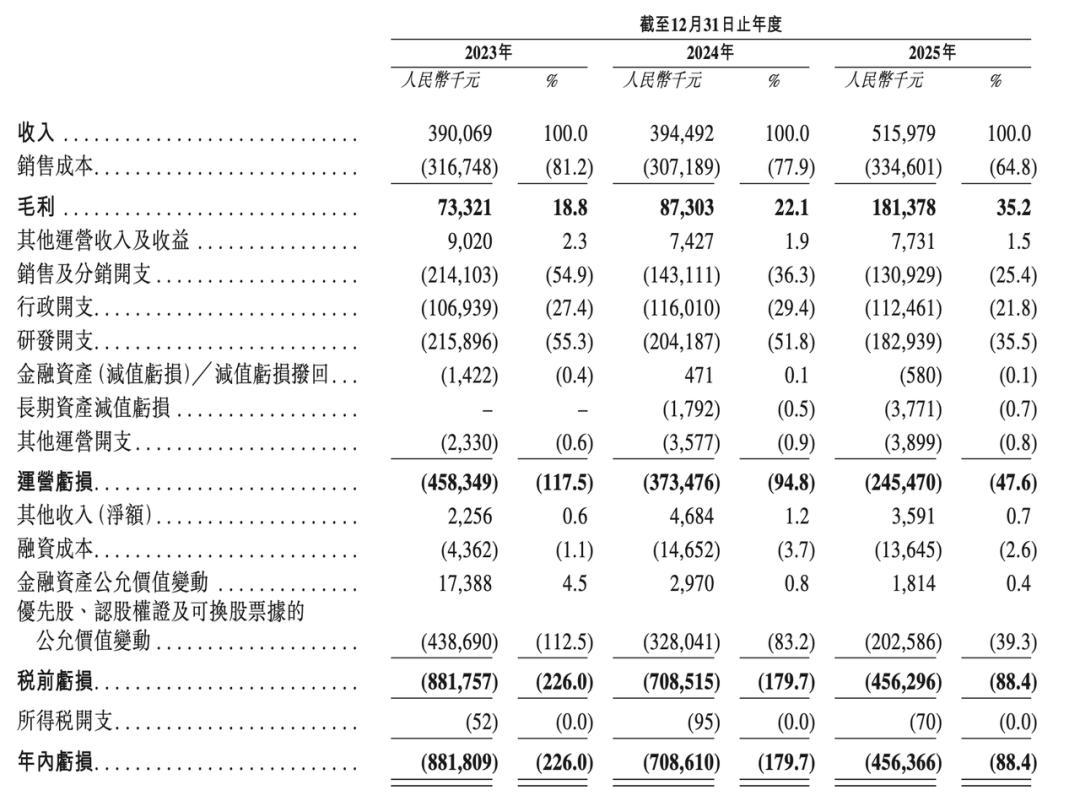

In 2025, XREAL generated 516 million yuan in revenue, up 30.8% year-on-year. While not groundbreaking in the consumer electronics sector, achieving three consecutive years of steady growth is notable for AR glasses—a new category still in the "market education" phase.

A closer look reveals two bright spots in its revenue structure.

1. Product Upgrades Drive Higher ASPs

The One series was the primary growth driver. The One, launched in late 2024, and the One Pro, released in mid-2025, sold a combined 111,000 units at an average price of 3,196 yuan—nearly double the 1,656 yuan ASP of the Air series.

Meanwhile, the Air series served as a volume play. However, its sales dropped from 104,000 units to 17,000 units in 2025 due to inventory clearance ahead of new product launches. Still, it laid the user foundation for XREAL over the past two years.

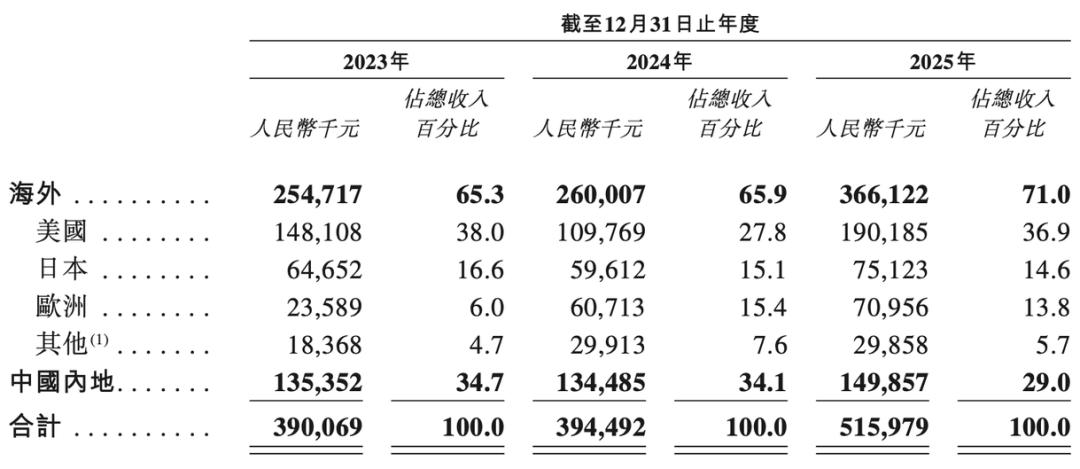

2. Overseas Markets Dominate Revenue

In 2025, overseas markets accounted for 71% of revenue. The U.S. contributed 190 million yuan (up 73%), Europe 70 million yuan, and Japan around 75 million yuan. XREAL has established local sales teams in North America, Japan, and South Korea, with products available in 40 countries and regions.

A high overseas market share is both a strength and a risk. It shields XREAL from domestic price wars but exposes it to geopolitical and tariff uncertainties.

On the profit front, XREAL remains unprofitable, posting a net loss of 456 million yuan in 2025. Excluding changes in the fair value of preferred shares, warrants, and convertible notes, the adjusted net loss was 250 million yuan—down from 437 million yuan in 2023 and 375 million yuan in 2024.

The silver lining: losses are narrowing yearly. However, a 250 million yuan loss for a company with 500 million yuan in annual revenue is still significant.

For startups, losses are expected; the key is whether they have enough cash to sustain operations until profitability.

XREAL lacks endogenous self-financing capabilities. Over three years, operating cash outflows were 470 million yuan in 2023, 174 million yuan in 2024, and 203 million yuan in 2025—showing significant volatility.

The company has relied on repeated financing rounds to stay afloat.

As of December 31, 2025, XREAL held just 63.63 million yuan in cash and equivalents, with current assets insufficient to cover current liabilities—even excluding short-term obligations like preferred shares and convertible notes.

Had it not secured new financing in January 2026, XREAL would be vulnerable if a competitor initiated a price war—a likely scenario in the future.

II. Slower Burn Rate, But Efficiency Remains a Challenge

Turning to expenses, XREAL’s R&D, sales, and administrative costs as a percentage of revenue fell from 137.6% in 2023 to 82.7% in 2025.

The most noticeable change was in sales expenses, which dropped from 214 million yuan in 2023 to 143 million yuan in 2024 and 131 million yuan in 2025—declining for two consecutive years. According to the prospectus, this reflects improved brand awareness and operational efficiency.

However, given the industry’s early stage, awareness gains and future marketing spending could rise sharply.

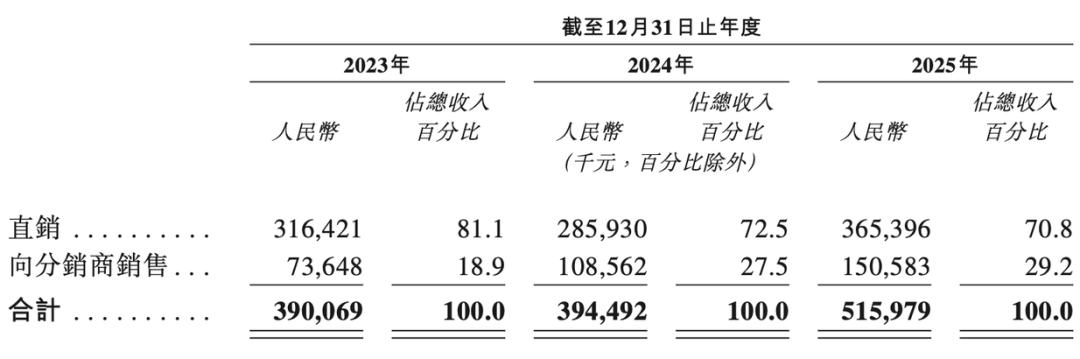

Notably, XREAL adopts a "direct sales + distribution" model, with direct sales accounting for over 70%.

Direct sales occur primarily through official websites and e-commerce flagship stores, offering high gross margins, direct user data access, and strong brand control. The downsides are high customer acquisition costs and limited market coverage.

Distribution channels account for about 30%, with partners including major consumer electronics retailers (e.g., Best Buy) and regional distributors. Distribution enables rapid market penetration but dilutes gross margins.

In 2025, distribution revenue rose from 109 million yuan in 2023 to 151 million yuan, with its share increasing from 27.5% to 29.2%—indicating growing channel penetration.

Returning to expenses, R&D spending also declined from 216 million yuan to 183 million yuan, with its share of revenue dropping from 55.3% to 35.5%. This was mainly due to reduced R&D service fees, team optimizations, and lower material costs.

Yet, an 82.7% expense ratio remains far higher than that of established consumer electronics companies—the core reason for XREAL’s losses. For every 100 yuan earned, 82.7 yuan goes to R&D, sales, and administration.

Admittedly, AR glasses are still in the early investment phase and cannot be directly compared to mature categories. However, the trend must improve: if future expense ratios don’t decline significantly, it will affect the company’s fundamentals and investor patience.

Herein lies the commercial dilemma:

To maintain technological leadership, XREAL must sustain high R&D investment. To expand markets, it needs a global sales team and channel construction. Expenses are hard to slash significantly. The only way out is rapid revenue growth to dilute the expense ratio.

However, AR glasses’ core use cases currently focus on movie-watching, gaming, and mobile productivity, with no breakthrough in high-frequency, rigid-demand scenarios. User adoption faces dual barriers of "price + experience." Even though XREAL’s entry-level products have dropped to around 2,000 yuan, they remain non-essential for average consumers, who demand higher standards for wearable comfort, battery life, and content ecosystems.

XREAL’s average inventory turnover days in 2025, at 187, underscore this point. It takes an average of six months to move inventory from raw materials to finished goods. Compared to leading consumer electronics companies, this figure has significant room for improvement.

Consumer electronics are depreciating assets; the slower the sales, the higher the depreciation risk. In 2023, 2024, and 2025, XREAL’s inventory write-downs were 12.2 million yuan, 13 million yuan, and 8.4 million yuan, respectively.

This indicates that AR glasses remain low-frequency devices with long decision-making cycles and slow adoption.

III. Awaiting the "iPhone Moment" for AR Glasses

In 2025, the global smart glasses market was valued at $2.3 billion. The sector’s limited size also imposes a ceiling on AR glasses companies’ commercial growth.

How can this ceiling be broken? We believe the key lies in the emergence of killer applications for AR glasses. A likely inflection point is the deep integration of AI and AR, enabling real-time translation, navigation, and information prompts—functions beyond smartphones’ capabilities.

Currently, XREAL is essentially a hardware company rather than a "hardware + software + services" platform.

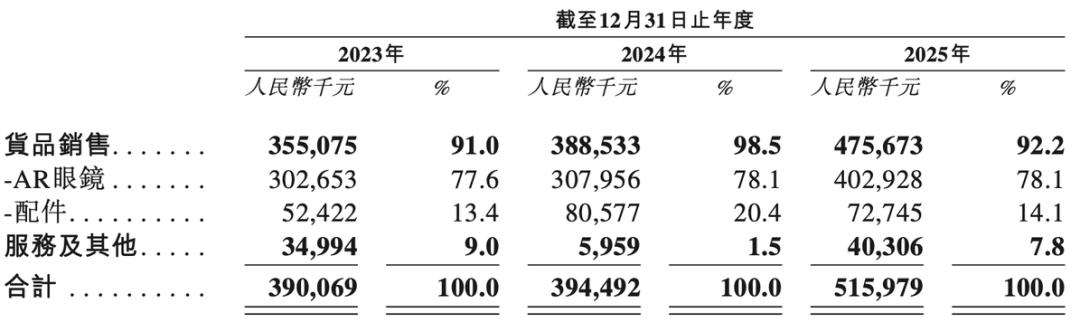

The prospectus shows that in 2025, product sales accounted for 92.2% of XREAL’s revenue, with AR glasses contributing 78.1%, while services and other income made up just 7.8%.

XREAL’s "focus on AR hardware" path contrasts sharply with the "ecosystem-driven" strategies of giants like Apple and Meta.

Apple leverages its iOS ecosystem and vast app library to rapidly build a "hardware + content + services" closed loop through its AR headset. Meta relies on its social ecosystem to gain an edge in VR/AR convergence.

The lack of value-added service revenues like app subscriptions and content payments leaves XREAL’s growth highly dependent on hardware sales. Price wars and homogenization in the hardware market further compress profit margins. This single revenue structure leaves AR commercialization vulnerable to risks and highlights the lag in ecosystem development.

This path divergence suggests that early-stage AR commercialization can pursue either "professional hardware breakthroughs" or "ecosystem-driven success," but ultimately must solve the linkage between "technology - scenarios - ecosystem."

XREAL is aware of this. Its prospectus states that it will launch "Project Aura" in 2026, featuring Google’s Android XR operating system and Gemini AI large model.

This is a smart move: rather than resisting ecosystems, it’s better to integrate into them. However, the risks are clear: Will Google support other hardware makers simultaneously? Just as in the Android smartphone era, Google had Samsung as its "lead" but also nurtured many other brands.

XREAL must prove its irreplaceability, either by establishing absolute leadership in optics and chips or by achieving network effects through user scale.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models