Memory Price Surge Weighs on Smartphone Sales! Global Smartphone Sales in Week 20: Huawei and Apple Buck the Decline, While Others Struggle

06/18 2026

06/18 2026

503

503

Kuaikeji, June 18 – The recent sharp increase in global memory chip prices has set off a ripple effect throughout the smartphone industry downstream, squeezing profit margins for numerous manufacturers and dampening overall shipment figures across the sector.

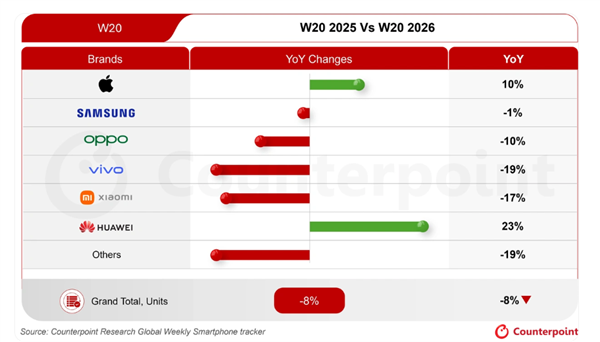

Based on the latest industry report from the esteemed market research firm Counterpoint Research, global smartphone sales for Week 20 of this year experienced an 8% year-on-year decrease, marking the ninth consecutive week of negative growth. The industry is facing mounting downward pressure.

Amidst this general market downturn, there has been a clear divergence in performance among various manufacturers. The majority of brands have been unable to withstand the knock-on effects of rising memory prices, with only Apple and Huawei, the two market leaders, achieving positive year-on-year growth in weekly sales.

Apple saw its weekly sales increase by 10% year-on-year, while Huawei's growth rate surged to 23%, making them stand out in a market that is otherwise experiencing a downturn and widening the gap with their competitors.

In the Android camp, Samsung showed notable resilience, with only a 1% year-on-year decline in weekly sales, effectively maintaining its market position. In contrast, most other Android smartphone brands saw double-digit year-on-year declines in weekly sales, significantly increasing their operational challenges.

The report points out the key factors driving the counter-trend growth of these two brands. Huawei benefits from domestic industrial policy support and a fully localized supply chain system, demonstrating strong resilience in its core domestic consumer market and avoiding being easily affected by sudden fluctuations in overseas supply chains.

In contrast, Apple leverages its long-standing robust control over the supply chain, along with its proven flexible pricing and tiered promotional strategies in the consumer market, to stabilize its sales base during the memory price hike cycle and even capture market share released by competitors.

From an industry-wide perspective, the ongoing volatility in the memory supply side has directly driven up upstream procurement costs for all downstream smartphone manufacturers.

Many manufacturers have faced supply shortages for core components, significantly reducing the pricing flexibility and promotional options that most manufacturers originally had, ultimately further dragging down overall end-user sales performance.

-

![]()

NVIDIA Sparks GPU Revolution, Challenging 5G Base Station Chips: Over 130 Firms Back the Initiative

-

![]()

Memory Price Surge Weighs on Smartphone Sales! Global Smartphone Sales in Week 20: Huawei and Apple Buck the Decline, While Others Struggle

-

![]()

‘CEORION of Cangqiong’ Takes the Dive: Large Models Tackle ‘Manual Labor’ in Marine Environments

-

[In-Depth] Dual-Beam UV-Visible Spectrophotometers: High-Precision Optical Analytical Instruments in a Fiercely Competitive Chinese Market

-

![]()

HDC 2026: Can Huawei Bridge the Tablet-Computer Divide with Multi-Screen Integration?

-

![]()

At HDC 2026, Will Huawei Bridge the Gap Between Tablets and Computers, Pioneering Multi-Screen Integration?

-

Companion Robot: Is It UBTECH’s New Path to Success?

-

![]()

AI Fails to Predict 'Cape Verde' Upset