Can Huawei Facilitate Baojun’s Ascent to the High-End Market?

04/17 2026

04/17 2026

663

663

Lead | Lead

This collaboration promises mutual benefits. For Baojun and Wuling, leveraging Huawei's advanced intelligent electric technology and brand clout offers the swiftest route to elevate their brand positioning and reclaim product pricing power. For Huawei, after solidifying its mid-to-high-end market presence (Note: 'layout' refined to 'presence' for natural English), Wuling presents an optimal gateway into the mainstream consumer market, providing crucial support for the rapid expansion of Harmony Intelligent Mobility.

Published by | Heyan Yueche Studio

Written by | Cai Yan

Edited by | He Zi

Full text: 2,377 characters

Reading time: 4 minutes

On April 7th, the Huajing S—a model of pivotal significance since its unveiling—finally commenced blind pre-orders. Its status as a flagship large six-seater SUV, equipped with standard Huawei ADS Pro enhanced intelligent driving, HarmonyOS cockpit 5.0, and an in-cabin laser vision Lumina system, emerged as its standout features. Based on Huajing S's product positioning, pre-order incentives, and Baojun's ambition to ascend the market ladder, its final pricing is poised to target the fiercely competitive RMB 200,000 segment, directly challenging models like the Geely Galaxy M9 and Chery Fengyun T11. Of course, we cannot dismiss the possibility of Huajing S adopting a pricing strategy akin to the Shangjie H5.

While Baojun Huajing S surpasses the Shangjie H5 in overall mechanical quality and market positioning, under Baojun's enduring 'affordable' and 'newcomer' labels, Huajing S is expected to emphasize 'premium value for money.' It is even foreseeable that Huajing S will emerge as the most cost-effective 'Chinese-branded' option in the new energy large six-seater SUV category.

As Huawei's intelligent driving solutions become more ubiquitous, can its current full-stack intelligent driving technology genuinely assist Wuling in breaking free from the 'low-end dilemma'? Huajing S's foray into the high-end market represents a daring balancing act for Wuling, involving pricing, technology, and timing.

Wuling's Persistent High-End Aspirations

For Wuling, Huajing S is more than just a new model; it symbolizes a crucial battle to penetrate the high-end market as the new energy sector matures.

By late 2018, Baojun had outlined three strategic pillars—'passenger vehicle focus, new four modernizations, internationalization'—formally charting its course towards high-end transformation. In 2019, it introduced a new diamond logo and officially targeted the RMB 100,000–150,000 mid-to-high-end market.

During 2017–2019, Baojun experienced its golden era, with annual sales surpassing 1 million units. Models like the Baojun 730, 510, and 560 dominated their respective segments, forming a diverse portfolio of bestsellers across various markets.

Despite its substantial market presence, Baojun faced dual pressures from the new energy wave, price cuts by joint-venture brands, and internal transition turmoil. It struggled to keep pace with industry shifts, leading to a gradual erosion of its market base and repeated setbacks in its high-end transformation or 'de-Baojunization' efforts.

The Baojun 730, unable to adapt to new energy trends, witnessed a steady decline in sales—falling below 5,000 units/month in 2021 and halving to approximately 2,000 units in 2022 before being discontinued.

As early as 2018, SAIC-GM-Wuling partnered with Huawei on intelligent electric technologies, launching the first Huawei HiCar-equipped model—the New Baojun RC-6—in 2019. Priced starting at RMB 123,800, this mid-size fuel-powered sedan was discontinued around 2021 after the brand failed to sustain its pricing.

Subsequent models like the Baojun Yue, Yunduo, Yunhai, and Xiangjing attempted to carve out a niche in the RMB 150,000 market but followed a pattern of initial enthusiasm and sales followed by rapid cooling—a trend exemplified by the Yue and Yunhai.

Ultimately, Baojun's high-end ambitions relied on gradually building reputation model by model—a viable strategy in the era of internal combustion engine (ICE) vehicles. However, in the new energy era, where the market demands 'cost-effectiveness + intelligence + electrification,' storytelling, pre/post-sales high-end image cultivation, dealer network distribution, and brand soft/hard power have become indispensable for high-end success.

Thus, despite 7–8 years of high-end endeavors (Silver Logo, Baojun), Wuling's 2025 performance indicates that its mainstays remain the Hongguang MINI and Binguo families, even as total sales reach 1.635 million units, new energy vehicles surpass 1 million units, and output value hits RMB 100.02 billion (+24% YoY).

This underscores Wuling's ability to create blockbusters but also highlights its 'low-end trap.' Success in the mass market has, to some extent, hindered its brand ascension.

In essence, for Huajing S, success does not hinge on Baojun's ability to offer the most cost-effective 'Chinese car' but rather on Wuling's capacity to 'de-Baojunize' the model.

SAIC-GM-Wuling Deputy GM Zhao Yifan acknowledges this reality. Wuling's current 'de-Baojunization' strategy for Huajing S focuses on enhancing pre-sales systems while likely retaining existing post-sales networks. Wuling has selected 169 dealers across 122 cities as initial agents—all former Baojun dealers—but will establish dedicated Huajing display zones and personnel.

If Wuling can further refine its post-sales systems to foster a virtuous cycle of 'hype-sales-product reputation-high-end service,' it could significantly elevate Baojun's brand image, avoiding a disconnect between 'high-end technology and low-end service.' Beyond technology, this represents Wuling's most crucial lesson from Huawei. Huawei's 'Mirror Series' exemplifies a full-link high-end experience with independent service networks and dedicated technicians.

How Can Baojun and Huawei Achieve a Win-Win Situation?

Given Wuling's clear self-positioning, how should it manage its relationship with Huawei?

In other words, as the 'Huawei halo' becomes less exclusive in 2026, with more automakers adopting 'Huawei intelligent driving cockpits,' how can Wuling differentiate its high-end positioning among 'Chinese-branded' models?

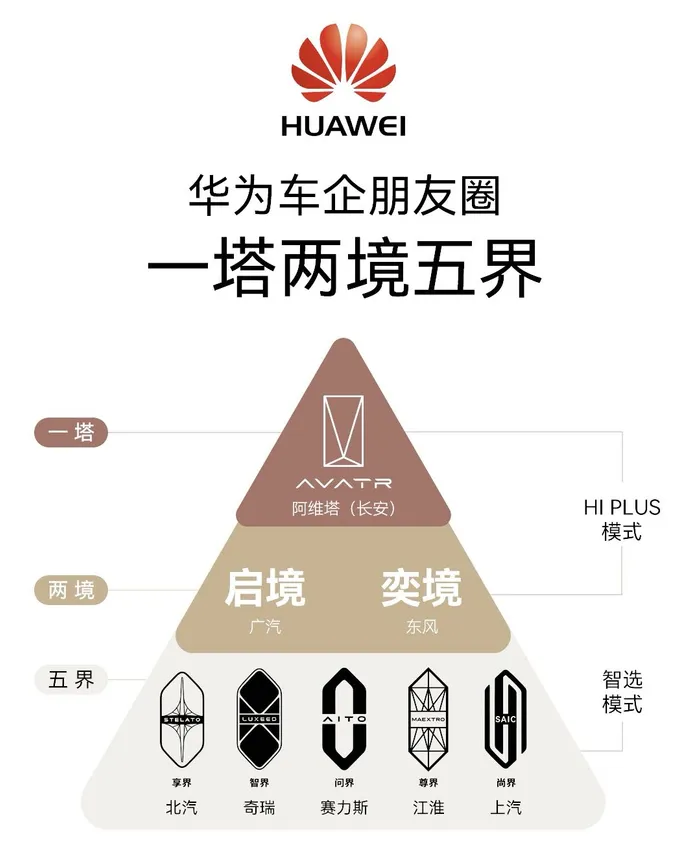

Notably, while online discussions raise questions about 'how Huawei should differentiate intelligent driving for brands with varying positioning,' this appears inconsequential from a supplier's perspective. Internally, Huawei has established a 'Five Realms, Three Spheres, One Tower' ecosystem, granting 'circle of close partners' (Note: 'deep Wechat Moments' refined to 'circle of close partners' for clarity) brands faster launch and customization rights. For others, Huawei functions more as a traditional supplier.

Zhao Chunzhang, Head of Automotive Strategy at Ries Consulting, asserts that the 'traditional automaker + tech company' model will dominate China's auto industry. These tech companies (Tier 1 suppliers) have transitioned from ICE-era transmission/electronic control system providers to intelligent driving/cockpit firms—essentially assuming the same role. Given the rapid tech iteration and user experience demands in the new energy era, collaboration will be more intimate than in the ICE age.

Ultimately, for Huawei, broader adoption of its intelligent electric services signifies market success. For partner automakers, the priority is to 'demonstrate their independent value as an automotive brand beyond Huawei's technological foundation.'

Commentary

When every automaker offers Huawei intelligent driving and cockpits, all 'Jing-series' models return to the same starting line through internal competition. Baojun's high-end success ultimately hinges on its brand essence. What Baojun most urgently needs now is to effectively communicate Huajing's unique value proposition to the market.

(This article is original to Heyan Yueche and cannot be reproduced without authorization.)

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry