Toyota's Fiscal Year 2026: The Top Earner Warns of Tough Times Ahead

05/21 2026

05/21 2026

741

741

On May 8, 2026, Toyota Motor Corporation unveiled its financial results for Fiscal Year 2026 (April 2025 to March 2026, for those familiar with our reporting style). The highlights include:

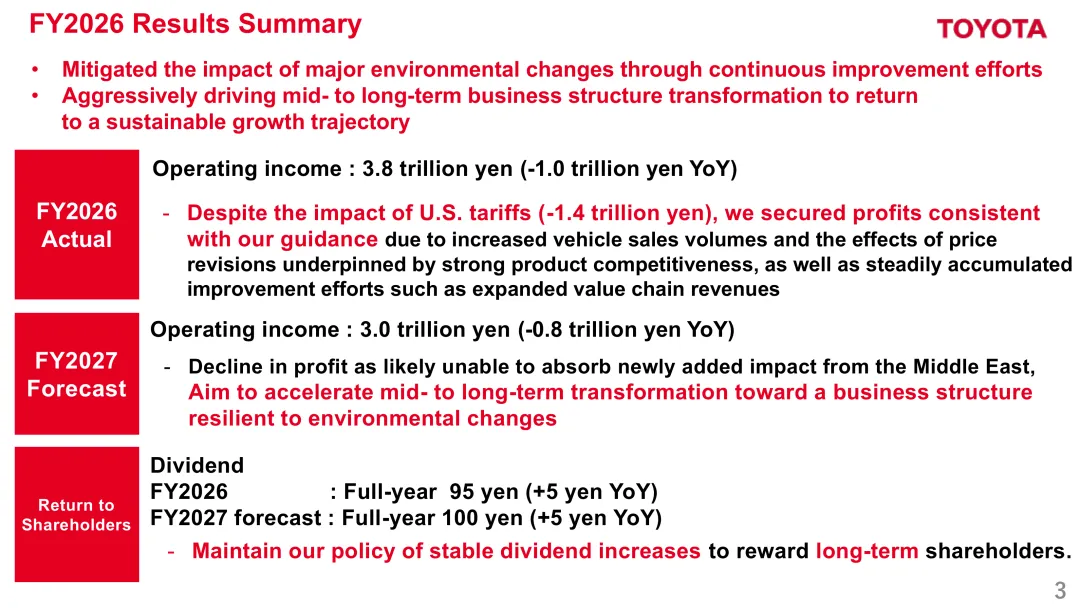

Operating profit: ¥3.77 trillion (~¥161.4 billion RMB), marking the highest profit achieved.

Revenue: ¥50.7 trillion (~¥2.17 trillion RMB), slightly trailing behind Volkswagen Group.

This report card showcases the automaker's continued dominance in vehicle sales, a feat that many envy. However, after reviewing the entire financial results briefing, what stood out most to me was not the financial figures themselves, but the almost self-critical opening remark from Toyota's CFO: "As CFO, I take seriously the fact that operating profit will decline for three consecutive years."

So, what crises lurk behind Toyota's Fiscal Year 2026 financial results, for both Toyota Motor and the entire automotive industry? Why would Toyota voluntarily acknowledge that future operating profit will continue to decline?

1. A Closer Look at the Report Card: Three Years of Profit Decline, but a Solid Foundation Remains

Let's examine several key data points:

Consolidated wholesale volume for FY2026: 9.595 million units, up 2.5% year-on-year (YoY).

Operating profit margin: 7.4%, down 2.6 percentage points YoY.

Impact from U.S. tariffs: -¥1.4 trillion (~-¥59.9 billion RMB).

Toyota's consolidated wholesale volume for FY2026 reached 9.595 million units, a notable 2.5% increase YoY, reflecting impressive growth in the current market environment. Overall retail sales stood at 10.477 million units, up 2% YoY.

Electrified vehicle sales surpassed 5 million units for the first time, reaching 5.04 million units, with an electrification rate of 48.1%. Among these, 4.62 million units were HEV hybrids (non-plug-in hybrids), the absolute mainstay, while BEV sales soared to 243,000 units, a 68.4% increase YoY.

Revenue reached ¥50.68 trillion (~¥2.17 trillion RMB), up approximately 5.5% YoY.

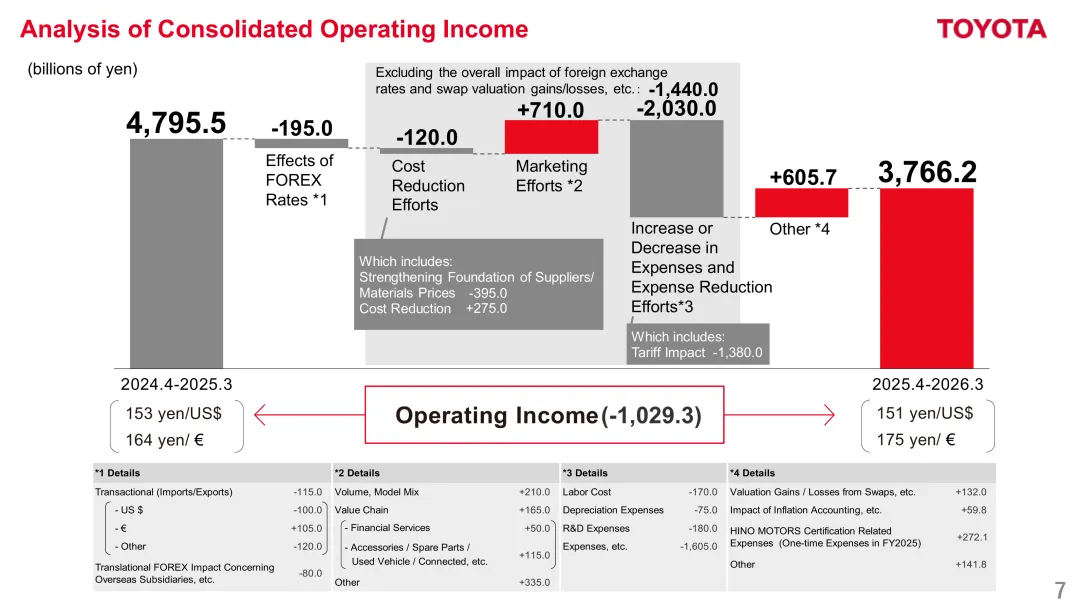

However, operating profit declined significantly by ¥1.03 trillion (~¥44.1 billion RMB) YoY, to ¥3.77 trillion (~¥161.4 billion RMB), with the profit margin dropping from 10% last year to 7.4%. While profit margin declines are a current reality in the automotive industry, Toyota's 7.4% margin is still the envy of its peers.

The fatal blow to Toyota's profit decline came from U.S. tariffs, which alone swallowed ¥1.38 trillion (~¥59.1 billion RMB) of Toyota's operating profit. To put this in perspective, this figure is equivalent to Ford's entire adjusted EBIT for a year and more than half of Volkswagen's 2025 group-wide operating profit. The money Toyota lost to tariffs could have been used to create another mid-sized automaker.

Regarding Toyota's FY2026 revenue details, the chart above clearly illustrates Toyota's revenue mix:

Revenue:

Volume and model mix contributed +¥210 billion (~¥9 billion RMB).

Automotive full lifecycle value chain business contributed +¥165 billion (~¥7.1 billion RMB).

Price adjustments contributed +¥115 billion (~¥4.9 billion RMB).

Expenses:

R&D expenses increased by +¥180 billion (~¥7.7 billion RMB).

Sales expenses increased by +¥1,605 billion (~¥68.7 billion RMB).

Tariffs reduced profit by -¥1,380 billion (~-¥59.1 billion RMB).

This reveals that behind Toyota's 7.4% profit margin, the "improvement dividends" painstakingly squeezed out daily by tens of thousands of employees in factory workshops are being devoured by tariffs.

2. Regional Breakdown: North America Shifts from Profit to Loss, Japan Holds Up Half the Sky

A closer look at Toyota's FY2026 performance by regional markets reveals an even more striking picture:

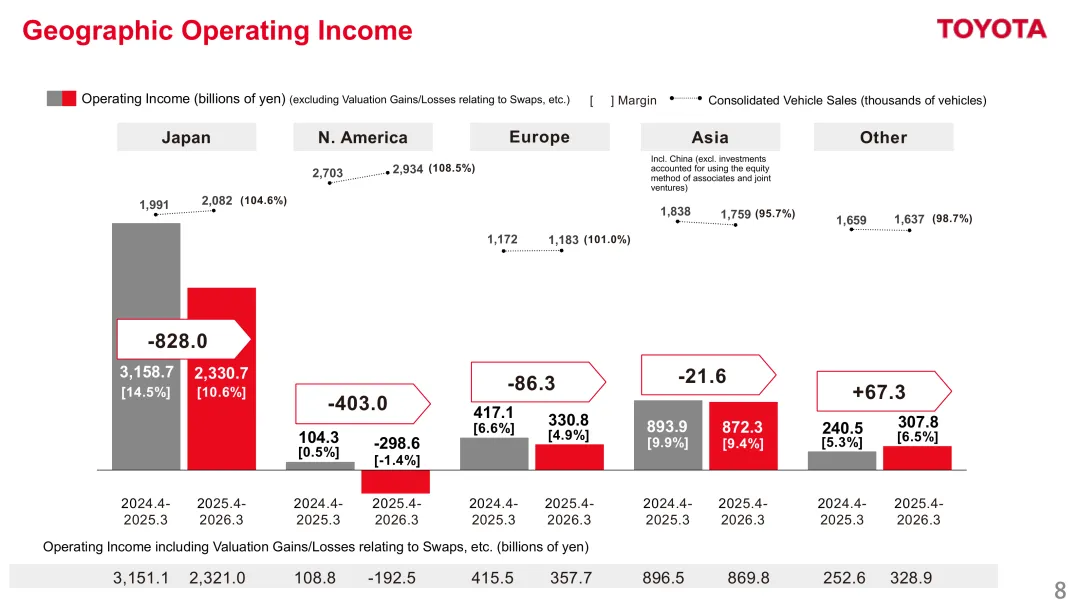

Japan: Domestic sales reached 2.082 million units (+4.6% YoY), with revenue of ¥23,307 billion (~¥99.8 billion RMB). The profit margin declined from 14.5% last year to 10.6%. However, the domestic market remains Toyota's profit foundation and the biggest contributor of cash.

North America: Sales reached 2.934 million units (+8.5% YoY), but profit was -¥2,986 billion (~-¥12.8 billion RMB), with a profit margin of -1.4%. Shifting from profit to loss, tariffs dealt a direct blow—this year, Toyota essentially worked for the U.S.

Europe: Sales reached 1.183 million units (+1% YoY), with revenue of ¥3,308 billion (~¥14.2 billion RMB) and a profit margin of 4.9%. Notably, the euro's appreciation against the yen in 2025 contributed to profits.

Asia (China): Sales reached 1.759 million units (-4.3% YoY), with revenue of ¥8,723 billion (~¥37.3 billion RMB) and a profit margin of 9.4%. Toyota's profits in Asia are truly substantial, even amid fierce competition from Chinese rivals. However, it must be admitted that Toyota's market share in China is under pressure. Additionally, facing Chinese automakers' expansion into Southeast Asia, Toyota's sales in the region are declining.

Central/South America and Middle East Emerging Markets: Sales reached 1.637 million units (-1.3% YoY), with revenue of ¥3,078 billion (~¥13.2 billion RMB) and a profit margin of 6.5%. Price increases in these emerging markets have taken effect, but they still face pressure from Chinese competitors.

The story behind North America's massive loss is that while Toyota has a large-scale localized production presence in the U.S., a significant amount of models and parts imported from Japan and Mexico were hit by tariffs. In the fourth quarter alone, North America posted a loss of ¥292.9 billion (~¥12.5 billion RMB), with a profit margin of -5.9%. This isn't because Toyota isn't selling—sales are still growing YoY—but rather because profits are being entirely intercepted by tariffs.

The Chinese market presents a peculiar combination of "slight sales decline, stable profits."

Toyota/Lexus retail sales in China were 1.764 million units, down 1.4% YoY—remarkably stable amid such intense competition in China.

More surprisingly, profits contributed by equity-method affiliates like GAC Toyota and FAW Toyota still reached ¥108.2 billion (~¥4.6 billion RMB), up 1.3% YoY.

One must admire Toyota's cost-cutting efforts and refined marketing in its Chinese joint ventures—but how long can this "profit margin for volume" approach last in China's hyper-competitive market with BYD and Geely? No one has the answer.

3. FY2027 Guidance: Another ¥800 Billion Decline, but "Proactively Accelerating Transformation"

For the next fiscal year, FY2027 (April 2026 to March 2027), Toyota provided the following guidance:

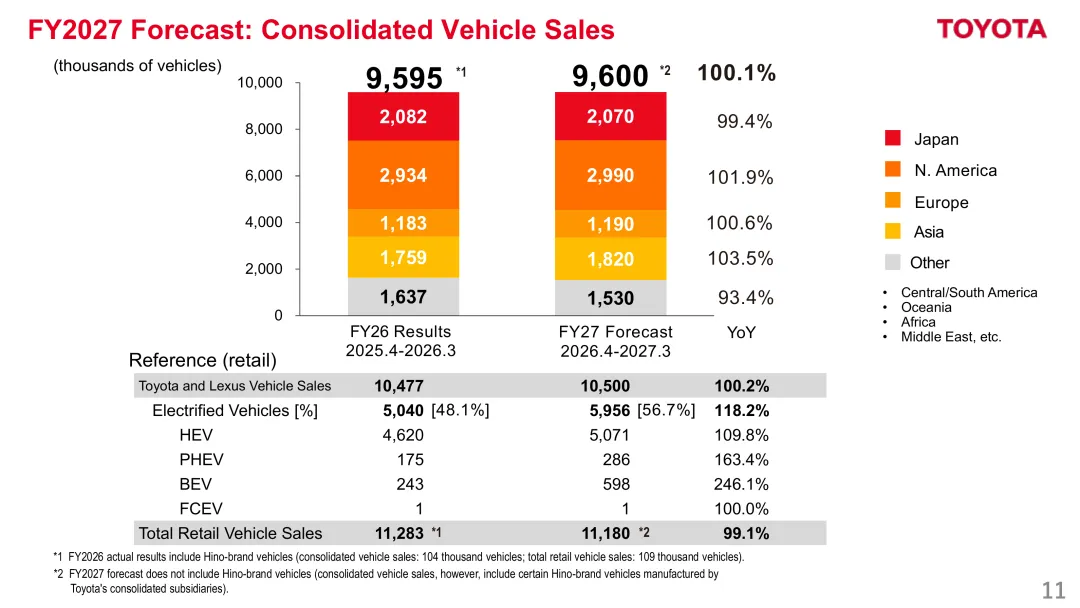

Sales: 9.6 million units, roughly flat YoY.

Revenue: ¥51 trillion (~¥2.18 trillion RMB), up 0.3% YoY.

Operating profit: ¥3 trillion (~¥128.4 billion RMB), down another ¥800 billion (~¥34.2 billion RMB). The profit margin will further decline from 7.4% to 5.9%.

Here, one must admire Japanese companies' pragmatism—directly telling investors that sales and revenue will be flat next year, but profits will decline again. This also reveals that the entire automotive industry's profits are facing restructuring and challenges.

Most surprisingly, Toyota plans to accelerate its electrification goals:

Electrified vehicle sales are expected to reach 5.956 million units, up 18.2% YoY, of which BEVs are expected to reach 598,000 units, up 146.1% YoY.

Yes, Toyota will still heavily focus on HEVs (non-plug-in hybrids), but its BEV annual growth rate is suddenly surging to triple digits. However, with BEVs still below 600,000 units, the scale remains small.

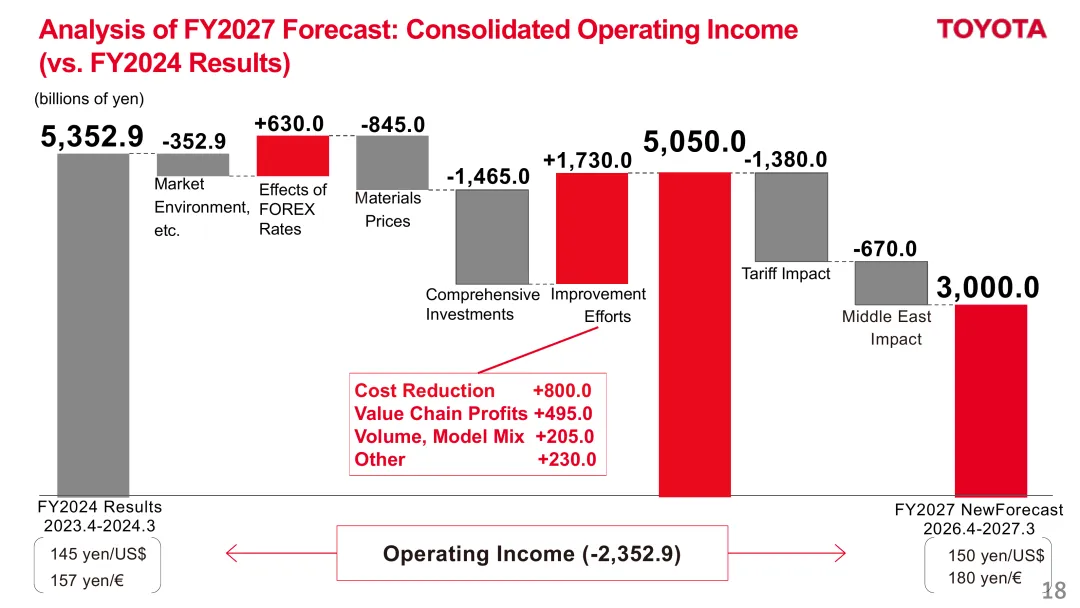

If we look at Toyota's operating profit trend over the past three years, the picture is even more stark:

Toyota FY24→FY27 Operating Profit Changes

FY2024 actual: ¥5.35 trillion / ¥229 billion RMB

FY2025 actual: ¥4.80 trillion / ¥205.3 billion RMB

FY2026 actual: ¥3.77 trillion / ¥161.4 billion RMB

FY2027 guidance: ¥3.00 trillion / ¥128.4 billion RMB

Over three years, tariffs have collectively impacted ¥1.38 trillion (~¥59.1 billion RMB), Middle East disruptions ¥670 billion (~¥28.7 billion RMB), material price hikes ¥845 billion (~¥36.2 billion RMB), and comprehensive investments ¥1.46 trillion (~¥62.5 billion RMB)—four blades striking simultaneously.

Yet Toyota still used "improvement efforts" to squeeze out ¥1.73 trillion (~¥74 billion RMB) in offsets, including cost cuts of ¥800 billion (~¥34.2 billion RMB), value chain business of ¥495 billion (~¥21.2 billion RMB), and volume/model mix contributions of ¥205 billion (~¥8.8 billion RMB).

This is what makes Toyota both admired and feared by global peers—while others respond to tariffs with price cuts, layoffs, or production halts, Toyota reacts with production efficiency improvements, cost reductions, supply chain optimizations, and product value expansions—a series of operational optimization measures that have roughly 380,000 employees across the company cutting costs and compressing production line rhythms once again.

In FY2026 alone, cost cuts reached ¥275 billion (~¥11.8 billion RMB), with a FY2027 target of another ¥205 billion (~¥8.8 billion RMB) in cuts. This "gemba (on-site) improvement" lean manufacturing industrial DNA is unmatched by any automaker's strategy. p>4. Business Structure Reform: Two Pillars, an Ambition for 20% ROE (Return On Equity)

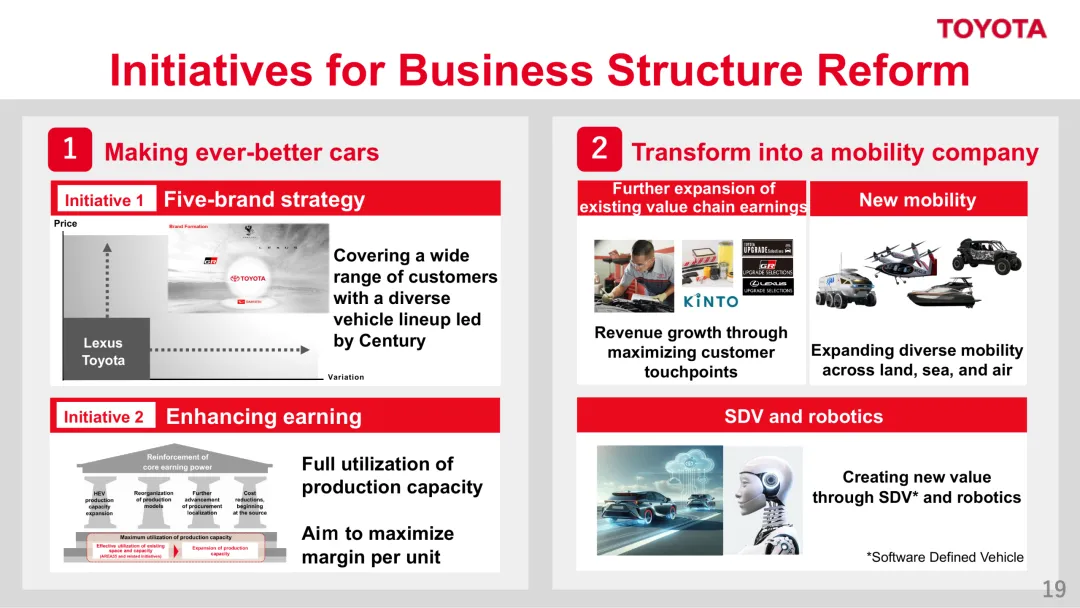

So how to secure future development? Toyota's CFO Yoichi Miyazaki broke down the reform path into two pillars in his speech—at this moment, Toyota's tone in discussing strategy is no different in essence from Volkswagen or Kia:

① Pillar 1: Build Ever-Better Cars

A five-brand strategy (Century/Lexus/Toyota/GR/Daihatsu) covering all price points; strengthening four pillars of profitability:

HEV capacity expansion, production model restructuring, deeper procurement localization, and source cost reductions. This maximizes unit contribution profit per vehicle.

② Pillar 2: Transform into a Mobility Company

Expand automotive full lifecycle value chain businesses (KINTO subscriptions, UPGRADE Selections, EW warranties, PPM prepaid maintenance), add diversified mobility businesses across land, sea, and air (including flying cars and vessels), and create new value with SDV and robotics technologies.

The data on automotive full lifecycle value chain businesses speaks volumes:

In 2021, operating profit under management scope was ~¥1.4 trillion (~¥59.9 billion RMB).

Rising to ¥2.1 trillion (~¥89.9 billion RMB) in 2025, with annual growth of ~¥150 billion (~¥6.4 billion RMB).

This means Toyota's automotive full lifecycle value chain business now exceeds Volkswagen Group's entire annual operating profit in scale.

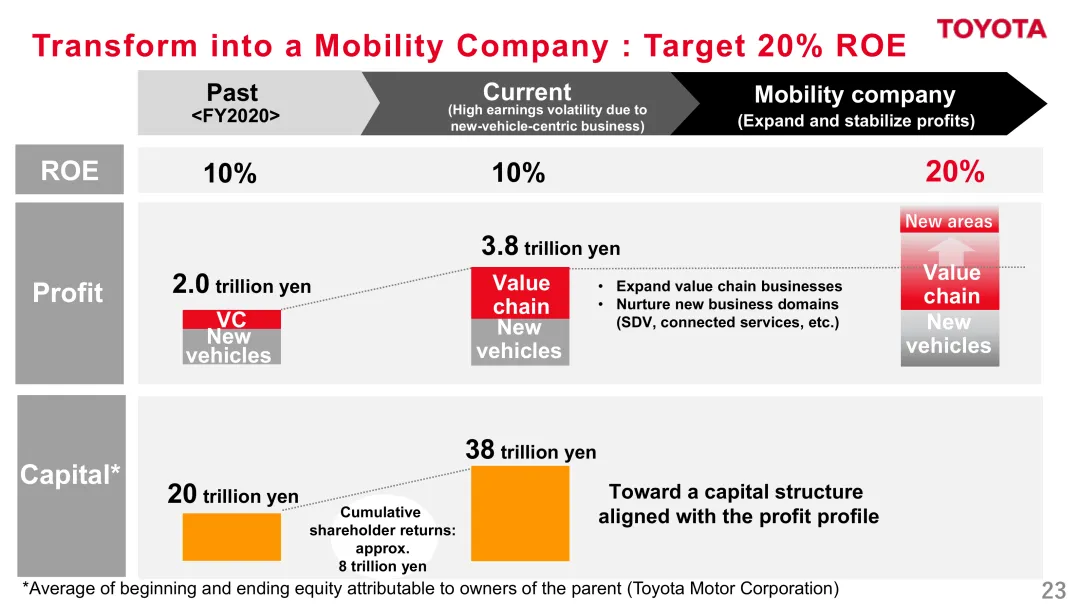

The most ambitious figure is hidden in the final PPT slide: Toyota explicitly sets an ROE target to double from the current 10% to 20%. The profit structure will shift from the high-volatility "new vehicle-heavy" business to a more stable structure where "value chain + new businesses" account for a larger proportion. Capital will grow from ¥20 trillion (~¥856 billion RMB) to ¥38 trillion (~¥1.63 trillion RMB), aligning this ¥38 trillion capital structure with future profit profiles.

In plain terms: Toyota used to earn money by selling one car at a time. In the future, it aims to earn continuously from "full lifecycle data + software subscriptions + derivative services" behind each vehicle. This is the logic of Ford Pro, Tesla FSD, and Kia PBV—now it's Toyota's logic too. The difference is—Toyota sells 10 million vehicles a year

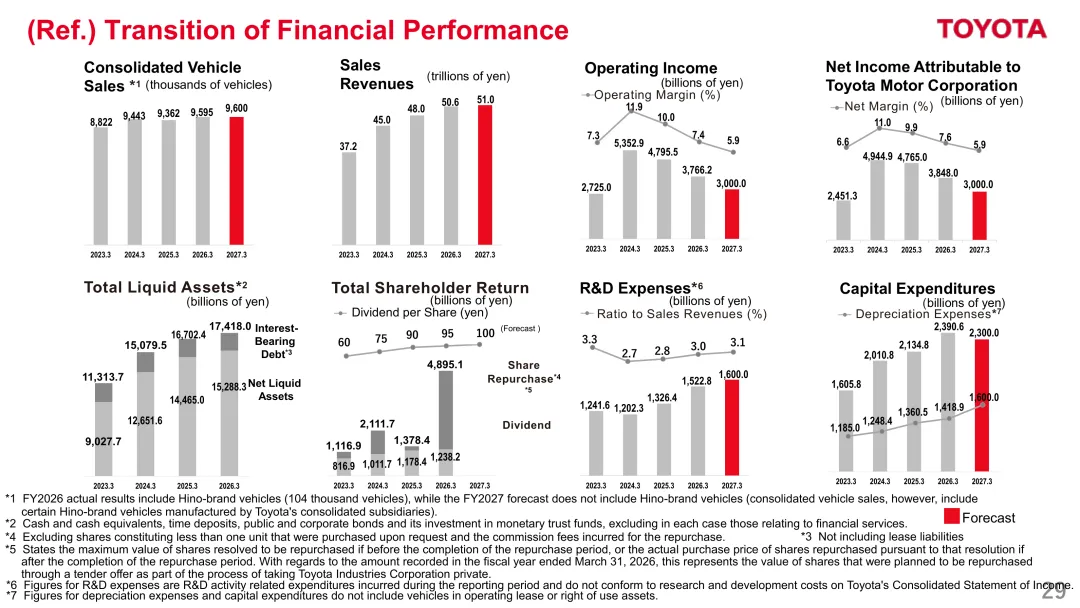

Over the past five years, sales have plateaued while profits have taken a downturn. In contrast, dividends and share buybacks have surged—in FY2026 alone, share buybacks soared to 3.66 trillion yen (approximately RMB 156.6 billion, inclusive of Toyota Industries' privatization offer), complemented by dividends of 1.24 trillion yen (approximately RMB 53 billion). This brought the total shareholder returns for the year to a record-breaking 4.9 trillion yen (approximately RMB 209.7 billion). This scenario is a classic indicator of a company reaching maturity: as growth margins diminish, funds gradually transition from 'investing in the future' to 'rewarding shareholders'.

However, Toyota is clearly not ready to fully embrace this trajectory. The company has continued to ramp up its R&D investment, increasing it from 1.2 trillion yen (approximately RMB 51.4 billion) to 1.6 trillion yen (approximately RMB 68.5 billion). Simultaneously, capital expenditures have also climbed from 1.6 trillion yen (approximately RMB 68.5 billion) to 2.3 trillion yen (approximately RMB 98.4 billion). Toyota is still making substantial financial commitments to propel its next phase of growth in SDV (Software-Defined Vehicles), robotics, electrification, and the Woven City project.

'The purpose of brakes is to enable you to drive faster. Without reliable brakes, you wouldn't dare to step on the accelerator. For me, acceleration means not easing up on investment in growth and seeing it through to fruition.'

—Toyota's new CEO, Koji Sato, echoing the sentiments of his mentor, Akio Toyoda

7 Key Insights for the Auto Industry

After examining Toyota's FY2026 financial report, which consistently places the company at the pinnacle of global automotive sales, several insights emerge for the burgeoning Chinese automotive industry:

Insight 1: Scale Does Not Automatically Equate to Advantage

Toyota sells nearly 10 million vehicles annually and should, in theory, enjoy a significant cost advantage. However, a 1.4 trillion yen (approximately RMB 59.9 billion) tariff reduction instantly reveals that scale can be vulnerable in the face of geopolitical shifts. BYD, selling 4.6 million vehicles a year, boasts double Toyota's gross margin—Chinese automakers are rewriting the relationship between scale and efficiency.

Insight 2: Self-Reflection Holds More Value Than Performance Alone

The CFO openly acknowledged, 'There have been too many short-term responses and too slow structural reforms'—such transparency is a rarity among traditional automakers. Volkswagen's 'Vision 2030' and Toyota's '20% ROE Vision' both underscore a common reality: the traditional business model has hit its limits.

Insight 3: Value Chain Businesses Will Shape the Winners of the Next Decade

Toyota's value chain businesses have expanded by 150 billion yen (approximately RMB 6.4 billion) annually, with KINTO subscriptions, extended warranties, used car businesses, and connected services accelerating their integration. This mirrors the strategies of Ford Pro's service subscriptions (+30%) and Kia's PBV One-Billing system. Earning money from one-time car sales is becoming less lucrative; selling a full lifecycle of services is emerging as the new profit frontier.

Insight 4: Never Underestimate the Cumulative Power of 'Continuous Improvement'

Amidst tariffs, Middle East conflicts, and material price hikes, Toyota managed to achieve cost reductions of 800 billion yen (approximately RMB 34.2 billion) through frontline employee improvements. This industrial ethos cannot be imparted through PowerPoint presentations or purchased with money—it is Toyota's deepest competitive advantage over the past 70 years and its most fundamental response to all crises.

In Closing

Toyota's FY2026 report serves as a multifaceted scorecard for its global peers. It remains one of the most profitable, stable, and technologically advanced automakers worldwide; yet, it is also the company that has incurred a 1.4 trillion yen (approximately RMB 59.9 billion) loss due to tariffs, witnessed profits decline for three consecutive years, and had to openly concede that 'reform has been too slow'.

From the 'product + region' dual-axis management system established during Akio Toyoda's 17-year tenure to the new framework of 'five brands + multi-technology pathways + mobility company' under Koji Sato's leadership, Toyota is undergoing another historic transformation from a traditional 'automaker' to a new entity. This time, the adversary is not General Motors, Volkswagen, or Ford—but itself.

When the world's most profitable automaker starts anxiously discussing 'returning to sustainable growth,' the entire automotive industry should take heed. In the next decade, no automaker can continue to thrive by simply 'having performed well in the past.' Not even Toyota.

Exchange Rate Note: All yen figures in this article are accompanied by (RMB conversion) based on the real-time exchange rate of 1 yen ≈ 0.0428 RMB (i.e., 100 yen ≈ 4.28 RMB) as of May 20, 2026.

References and Images

Toyota Motor FY2026 Financial Report PDF

Toyota Motor FY2026 Annual Report Presentation

*Unauthorized reproduction or excerpting is strictly prohibited.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry