A Monumental Global Shift Unfolds: The Strategic Moves of BYD, Geely, and Chery

05/21 2026

05/21 2026

531

531

Written by | Guanchejun

A Monumental Shift in Production Capacity Among Chinese Automakers Is Underway!

This could mark the most significant capacity shift in a century of automotive history.

The narrative unfolds with a series of news reports emerging in May 2026.

Recently, Li Ke, Executive Vice President of BYD, disclosed to the media that the company is engaged in discussions with Stellantis and other European automakers regarding the acquisition of idle or underutilized factories across Europe.

Almost concurrently, Geely announced on the Hong Kong Stock Exchange its complete acquisition of Radar Automotive and its Thai distribution entity for RMB 218 million.

Delving deeper into the past, Chery inked a deal for Nissan's Rosslyn plant in South Africa, while persistent rumors have swirled around Geely and Ford's negotiations concerning the Valencia production line in Spain.

Mexico is witnessing heightened activity, with BYD, Geely, and GAC, alongside Vietnam's VinFast, competing for Nissan's COMPAS plant...

Chinese automakers are embarking on a global acquisition spree—what does this portend? From Guanchejun's perspective, the most immediate catalyst is tariffs.

Commencing in 2024, the EU imposed additional anti-subsidy tariffs on Chinese electric vehicles, augmenting the existing 10% import duty and thereby diminishing the price competitiveness of Chinese EVs post-taxation.

The sole means to circumvent this barrier is through localized production. However, constructing a new factory from the ground up, encompassing land acquisition to production commencement, necessitates a minimum of three to five years.

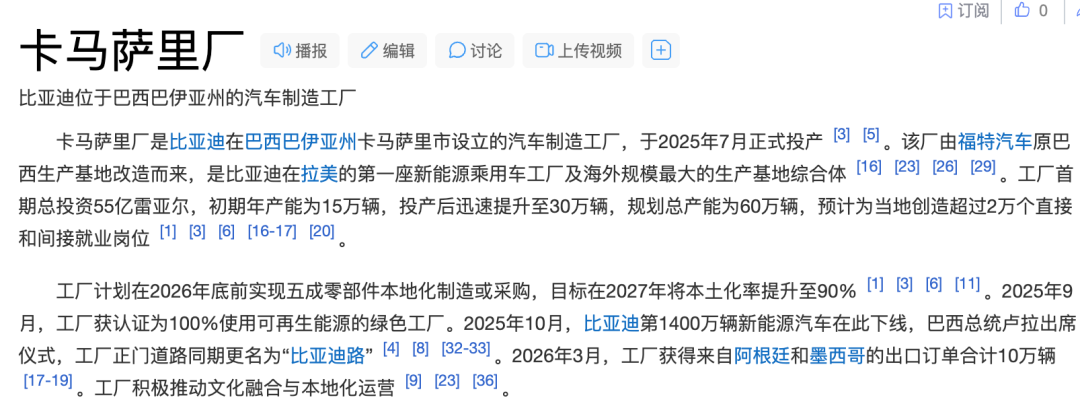

Conversely, renovating an existing facility can expedite the process, with the first vehicle rolling off the line in under a year. This strategy was exemplified by BYD in Brazil: acquiring Ford's Camaçari plant in July 2023, launching its inaugural vehicle 16 months subsequent, and by April of the current year, the factory was already operating on a 24-hour, three-shift schedule.

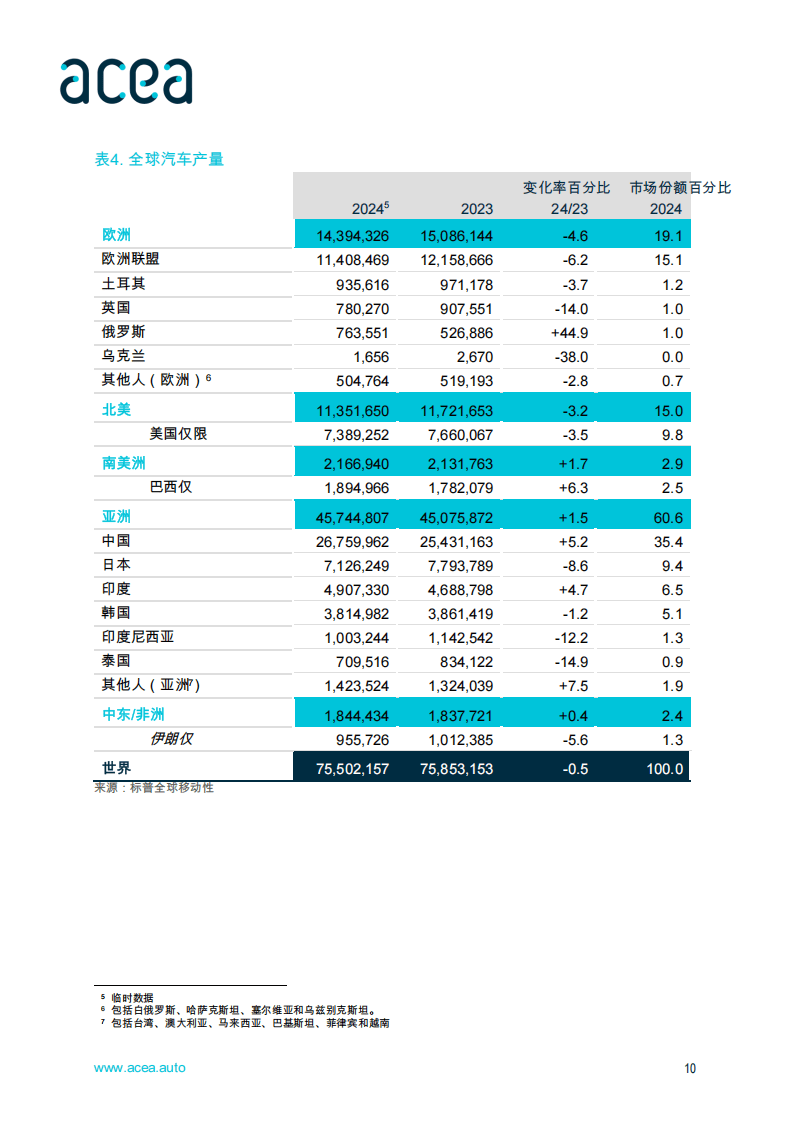

So, why are Europeans inclined to sell? The answer lies in their declining production.

According to IndustriALL, a union organization, Europe's annual auto production plummeted from 16 million units in 2018 to 11.4 million in 2024, representing a nearly 30% decline.

Legacy automotive behemoths like Volkswagen and Stellantis have been compelled to "streamline" for electrification, resulting in numerous factories operating at less than half capacity, transforming into financial burdens that are prohibitively expensive to shut down.

Volkswagen's Dresden plant serves as a quintessential example. Slated to be the first factory in Volkswagen's 88-year history to cease operations in its home market, it will halt production by the end of 2025 and has already garnered interest from several Chinese companies.

Industry insiders characterize these acquisitions as "move-in ready," with mature production lines, skilled labor, supplier networks, and certifications already in place. Chinese automakers introduce technology and more efficient production methodologies, while Europe preserves jobs and tax revenue.

Both parties stand to gain from this transaction.

According to AlixPartners, Chinese automakers and suppliers intend to escalate overseas production from 1.2 million units in 2025 to 3.4 million by 2030, establishing production bases in no fewer than 16 countries.

If Great Wall's comprehensive acquisition of GM's Rayong vehicle and powertrain plants in Thailand in 2020 signified the inception of Chinese automakers' "globalization," today's approach transcends mere "testing the waters" and instead involves "diving in" to construct a comprehensive global manufacturing system concurrently.

This scenario evokes memories of over two decades ago when Volkswagen, GM, and Toyota established joint ventures in China under the "market-for-technology" paradigm. The foreign entities supplied brands and technology, while the Chinese side contributed land and labor, with production lines merely replicated.

Two decades prior, Li Shufu was dismantling Toyota engines to decipher car construction; two decades later, century-old Ford is contemplating the utilization of Chinese automakers' vehicle architectures. Reports indicate that Ford may introduce collaborative models based on Geely's GEA architecture in the future.

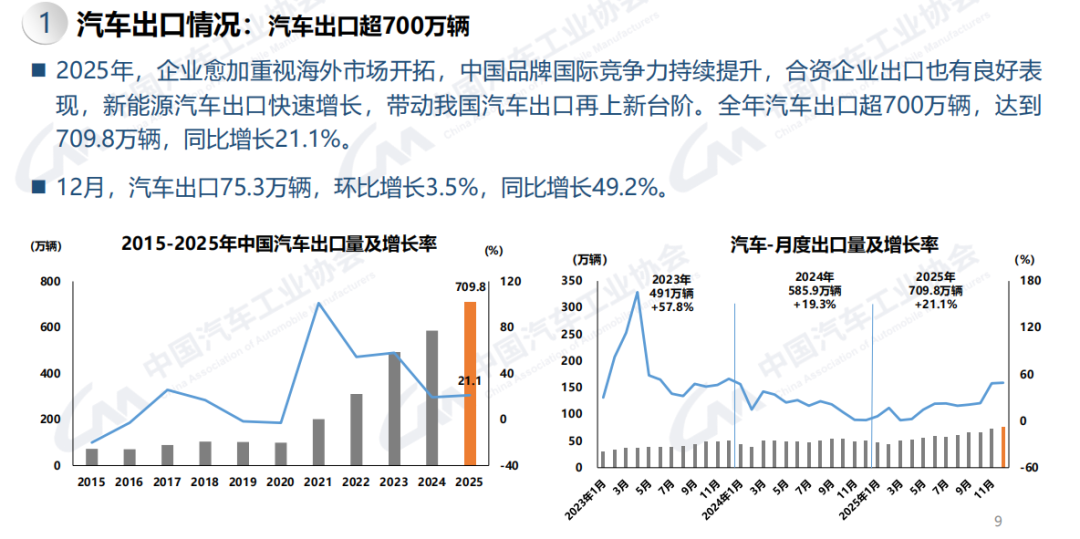

In 2025, China exported 7.098 million vehicles, marking a 21.1% year-on-year increase and securing the top global position for three consecutive years.

During the first quarter of 2026, exports reached 2.34 million units, reflecting a 53% year-on-year surge. Although China's global share of new energy passenger vehicles experienced a slight decline in the first quarter, it still stood at 61%.

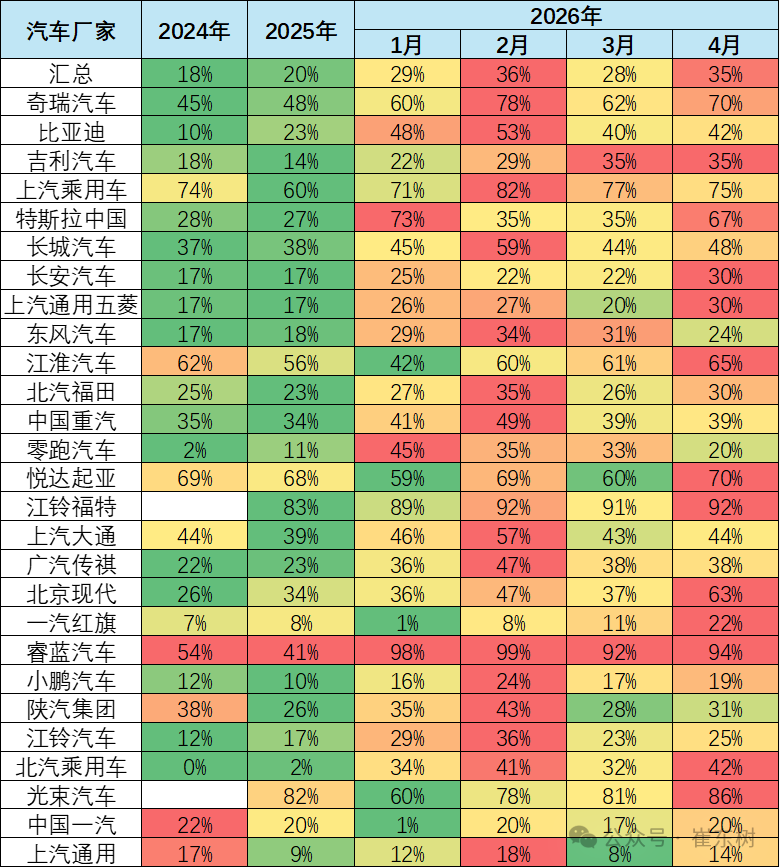

In April just gone by, exports constituted 35% of total sales for Chinese automakers, in contrast to a mere 20% in 2025.

In essence, the epicenter of industrial might is shifting, yet the traditional "cost-effectiveness" ticket is gradually being discarded.

From Guanchejun's vantage point, the focus of competition in the forthcoming phase has transitioned to defining charging interface standards, mastering data protocols for intelligent driving, and establishing rule systems for energy networks—this constitutes the ultimate rationale behind the global acquisition spree by major automakers.

Unless specified otherwise, all charts in this article are derived from public disclosures across various channels. Special acknowledgment is extended for this. The viewpoints expressed herein are for reference only and do not constitute investment advice.

This article represents original content from Leverage Auto Insights. Unauthorized reproduction is strictly prohibited. For reprints, please obtain authorization. Additionally, when reprinting with authorization, kindly indicate the source and author at the commencement of the article. Thank you!

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry