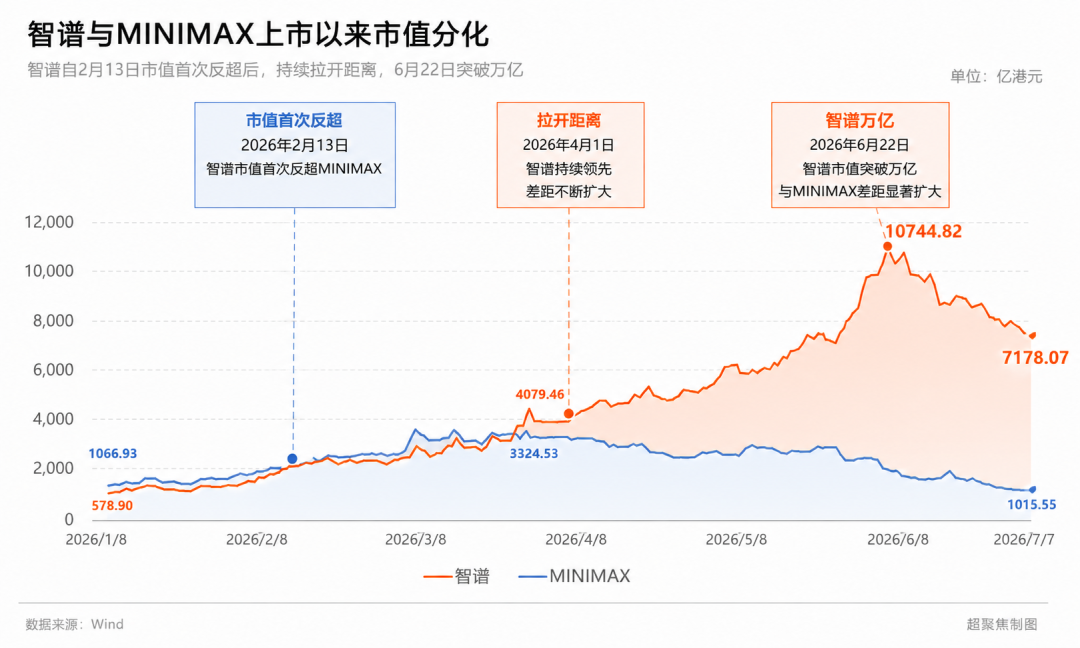

In Less Than Half a Year, The Market Cap Gap Between MiniMax and Zhipu Has Reached HK$600 Billion

07/09 2026

07/09 2026

554

554

While You Were Engrossed in AI Chat, Smart Money Quietly Shifted Tracks

The two domestic large model giants that went public around the same time now find themselves with vastly different valuations.

On January 8, Zhipu debuted at HK$116.20 per share. Over the next six months, its stock price surged, peaking at HK$2,980—a more than 24-fold increase from its IPO price.

In contrast, MiniMax, which went public the next day, experienced a wild ride. After initially soaring sevenfold to a high of HK$1,330, its stock price quickly reversed course. By the close on July 7, it had retreated to HK$323.8, representing just a twofold increase from its IPO price. Meanwhile, Zhipu still boasted a nearly 13-fold gain.

The market cap gap between the two companies has widened from negligible at listing to over HK$600 billion today.

Both are part of the 'AI Six Little Tigers' and develop large models, yet they went public almost simultaneously. Why is the capital market's verdict on them becoming increasingly divergent? Why has Zhipu 'won big' while MiniMax has 'stumbled'?

01 Entertainment Narrative Pales in Comparison to Coding

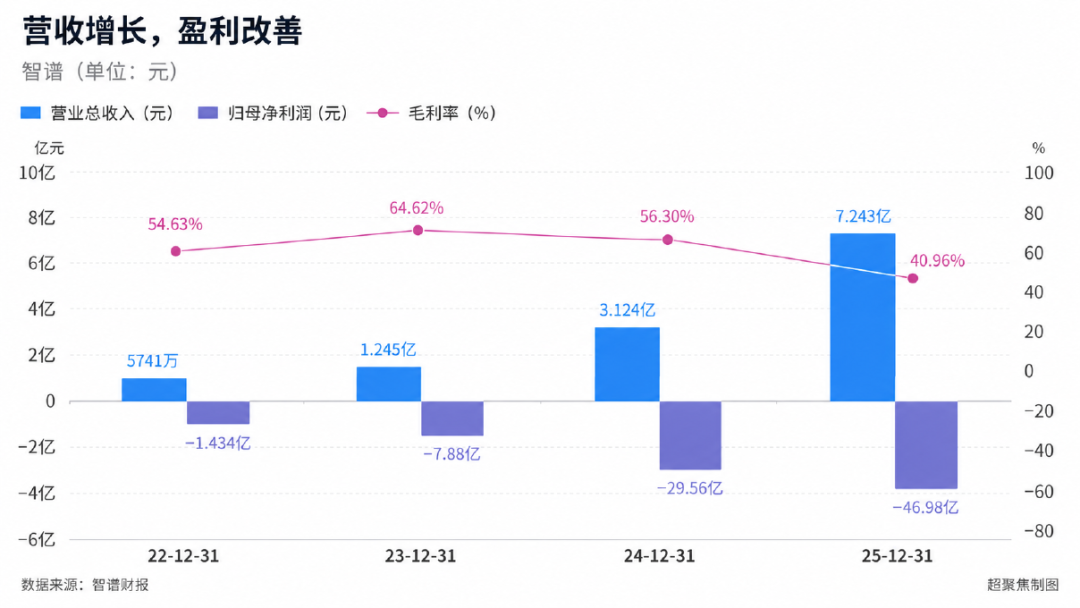

Financial data alone struggles to explain the gap between Zhipu and MiniMax today, as both companies have followed similar paths in recent years: rapid revenue growth accompanied by escalating losses.

From 2022 to 2025, Zhipu's revenue surged from RMB 57.41 million to RMB 724 million, expanding more than 11-fold in three years. Over the same period, its net loss attributable to the parent company widened from RMB 143 million to RMB 4.698 billion.

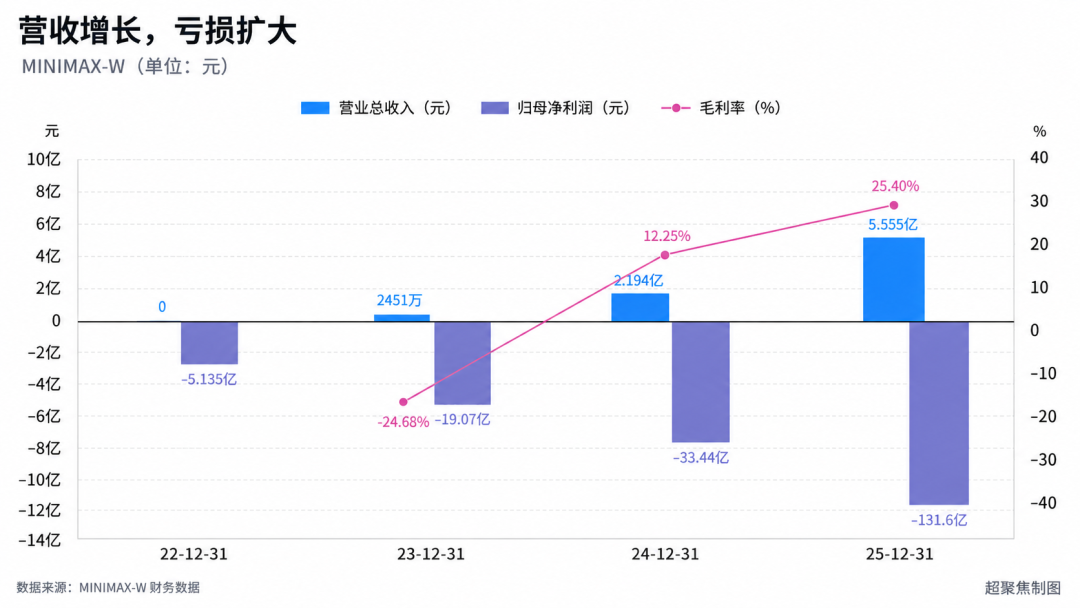

MiniMax followed a similar trajectory. Its revenue grew from RMB 24.51 million in 2023 to RMB 556 million in 2025, while its net loss attributable to the parent company ballooned from RMB 1.907 billion to RMB 13.16 billion (including a RMB 1.59 billion fair value loss on financial liabilities).

This is not surprising. Training foundational models, procuring computing power, attracting top talent, along with inference costs and product subsidies, mean that large model companies at this stage are inherently businesses that exchange massive losses for growth. Neither Zhipu nor MiniMax is profitable.

By some financial metrics, MiniMax even appears to have an edge.

From 2024 to 2025, MiniMax's revenue grew from RMB 219 million to RMB 556 million, a more than 150% increase, while its gross margin improved from 12.25% to 25.40%. Over the same period, Zhipu's revenue rose from RMB 312 million to RMB 724 million, a more than 130% increase, but its gross margin declined from 56.30% to 40.96%.

After excluding the fair value loss on financial liabilities, MiniMax's net loss in 2025 was US$250 million, up just 2.7% year-on-year—far below Zhipu's.

One company is growing revenue faster, improving gross margins, and keeping loss expansion relatively contained after excluding massive fair value fluctuations. The other, while larger in revenue scale, is seeing gross margins decline sharply and losses continue to widen.

At least based on the income statement, it's hard to justify Zhipu's stock price surging more than tenfold from its IPO price while MiniMax has fallen three-quarters from its peak.

The real gap may not lie in who is losing less, but in which company's losses the market is willing to bet on.

On July 2, JPMorgan noted that the relative preference for 'Zhipu over MiniMax' had gained clear traction among U.S. investors. More importantly, discussions around the two companies had shifted from model quality to business sustainability.

This statement matters far more than 'whose model is stronger.'

In JPMorgan's description, U.S. investors now demand not just frameworks but 'proof with dates.' The report specifically highlighted that cloud margins, AI KPIs, unit economics, revenue disclosure, and post-lockup market performance matter more than grand industry narratives.

In other words, large model companies can continue to lose money, but they must prove that the cash burned today is translating into verifiable commercial results tomorrow.

In their view, Zhipu aligns more closely with this logic.

The report cited investor preference for Zhipu not just due to model quality but also pricing power, capital access, and financing momentum. However, JPMorgan cautioned that Zhipu's bullish narrative should not rest solely on 'leading in general-purpose foundational models' but on Coding—a 'defensible workflow'—ultimately proving four things: paid demand, pricing power, retention, and enterprise value capture.

'Defensibility' hinges not on which model programmers find smarter today, but on whether, once integrated into IDEs, code repositories, testing deployments, and enterprise development workflows, the model competes for a position within the workflow rather than just a single API call. Only if enterprises keep paying and stay even after price hikes does model capability truly become a business.

This means Zhipu's challenge is 'can it execute well,' while MiniMax faces the question 'does it have the capability to execute.'

JPMorgan called MiniMax the most negatively viewed among the discussed targets, with investors focusing on its past pricing failures, the price floor set by DeepSeek, Zhipu's capital advantages, and whether scarcity can sustain valuations post-lockup.

The most noteworthy point here is not the lockup expiration but 'pricing failures' and the 'price floor.'

This strikes at the heart of consumer entertainment narratives: users may be plentiful, and products may be popular, but if switching costs are low, traffic may not translate into pricing power. Users may find an AI companion amusing today but switch to another tomorrow; a video model may impress now, but its edge could vanish with the next update.

This is not to say MiniMax lacks Coding capabilities, but rather that the capital market sees different dominant narratives for the two companies.

Zhipu is being asked to prove whether Coding can drive paid conversions, retention, and enterprise value. MiniMax must still answer whether entertainment and consumer traffic can escape the novelty cycle and retain pricing power after DeepSeek keeps driving industry prices lower.

Compounding the issue, JPMorgan warned that as more AI assets like Kimi and DeepSeek go public or become investable, the premium once enjoyed by 'scarce listed large model companies' may shrink further. By then, leading model rankings will only be a prerequisite; the real test will be retaining users, defending prices, and capturing enterprise value within specific workflows.

The gap between the two companies may not lie in who is losing more but in which company's losses the capital market believes will eventually yield pricing power. Entertainment competes for attention; Coding competes for workflows. The former must constantly prove users still find it novel; the latter only needs to prove users can't live without it.

Thus, as the market shifts from 'whose model is stronger' to 'whose business model is more sustainable,' entertainment narratives become increasingly devalued against Coding.

02 Massive Lockup Expiration: Will MiniMax Follow SenseTime's Path?

If commercial narratives determine which company the capital market is willing to value higher, the upcoming lockup expirations further widen the gap between the two.

On July 8, Zhipu faced its first post-IPO lockup expiration; MiniMax followed a day later. But the scale of these expirations could not be more different: Reuters estimated that Zhipu had approximately 25.6 million shares (nearly 6% of total shares) released from a six-month lockup, while MiniMax saw about 45% of its total shares become eligible for sale.

The real trouble lies beyond the 45% figure.

Prior to this, only about 5% of MiniMax's shares were freely tradable. This means its market cap, which had soared into the hundreds of billions of Hong Kong dollars over the past six months, rested on an extremely thin free float. A small amount of capital chasing a small number of shares could quickly drive the stock from its IPO price of HK$165 to HK$1,330. But when a large number of existing shares suddenly become eligible for sale, the scarcity premium built on 'unavailability' quickly erodes.

This implies that MiniMax's potentially tradable shares could expand nearly tenfold compared to its original free float.

A company may command a premium due to scarcity, but it cannot rely on scarcity indefinitely to maintain high valuations—especially not when MiniMax's lockup expiration coincides with an extremely awkward timing.

Since early June, MiniMax's stock price has plummeted. On July 2, JPMorgan's report highlighted U.S. investor concerns over its pricing failures, the price floor set by DeepSeek, and whether its scarcity premium could hold post-lockup. By July 7, MiniMax closed at HK$323.8—down three-quarters from its HK$1,330 peak but still nearly double its HK$165 IPO price.

For secondary market investors, this represents a massive retracement. But for early investors who bought in at prices far below the IPO price and have waited years, it may still offer a profitable exit.

Of course, lockup expiration does not equal selling, nor will 45% of shares flood the market in a single day. Existing shareholders may hold, industrial capital may stay invested, and some core shareholders remain bound by longer lockup periods.

But capital markets trade not just on actual sales but on 'who could sell anytime.' This evokes memories of SenseTime four years ago.

On June 30, 2022, SenseTime faced a massive lockup expiration involving approximately 23.3 billion shares (about 73% of total shares). That day, management temporarily extended lockups for some shares, but panic ensued. The stock plummeted nearly 48% intraday before closing down 46.77%, breaking below its HK$3.85 IPO price for the first time.

SenseTime did not collapse nearly 50% solely because of 'lockup expiration.' The expiration merely exposed issues hidden by its extremely low free float: when large blocks of existing shares gain exit rights, the secondary market must reassess the company's true value and whether sufficient new capital exists to absorb years-old shares waiting to be sold.

Now, the same question confronts MiniMax.

Over the past six months, it enjoyed both the scarcity premium of a large model company and the price elasticity from an extremely thin free float. On its debut, MiniMax surged 78%; it later peaked at HK$1,330. But today, with more large model companies entering the market, commercial feedback on its M3 release under scrutiny, and a massive number of shares becoming eligible for sale, the three pillars supporting its valuation are crumbling simultaneously.

Conversely, Zhipu faces the opposite scenario.

It also encountered its six-month IPO lockup expiration on July 8, with approximately 25.6 million cornerstone investor shares (nearly 6% of total shares) released. At the July 7 closing price, this corresponded to a market cap of hundreds of billions of Hong Kong dollars—no negligible sum.

However, ahead of the expiration, reports emerged that multiple institutional investors explicitly stated their intention to hold long-term, with these institutions collectively owning nearly 70% of the expiring cornerstone shares. While such statements lack legally binding lockup commitments, they at least provided the market with a vastly different expectation emotionally.

On July 8, Zhipu's stock surged over 18% on its first lockup expiration day.

For lockup expirations, one side fears a stampede of exiting shareholders; the other bets on institutions remaining locked in. The difference again hinges on whether the capital market continues to believe in your story.

Whether MiniMax will repeat SenseTime's fate remains undetermined. SenseTime's 73% lockup expiration was higher, and its market environment and fundamentals differ entirely. Equating the two companies oversimplifies the issue.

But MiniMax now faces dual tests: on the business side, whether its entertainment and consumer narrative can ultimately translate into paid conversions, retention, and pricing power; on the capital side, how much of its scarcity premium, built on an extremely thin free float, remains after 45% of shares become eligible for sale.

Zhipu, meanwhile, sees its Coding narrative strengthening and its capital-raising ability remaining favored. Even with its first lockup expiration, the market still believes its scarcity has not ended.

This may be the true reason the two companies are drifting further apart.

MiniMax is being asked to prove its worth without scarcity, while Zhipu still operates in a world where the market fears missing out.

- END -

-

![]()

Explosion of AI Upstream Materials

-

![]()

Has Baidu Finally Made the Right Bet in the AI Era?

-

![]()

The Perplexing State of AI Commercialization for Large Enterprises

-

![]()

Unitree and UBTECH: Two Commercial Experiments of Chinese Humanoid Robots in 2026

-

![]()

Flood Dividends vs. Drops in the Ocean of AI: A Deep Dive into OPPO's Ostrich-Style Survival Strategy

-

![]()

Shenzhen’s Longgang District Unveils New Rules for Autonomous Vehicles: Initial Deployment of 30 Vehicles, 5% Inspection Rate, and Nationwide Cross-Regional Recognition

-

![]()

Overestimated 'NIO, Xpeng, and Li Auto': Underestimated 'BYD, Geely, and Chery'

-

Are Shovel Buyers Running Low on Cash? Has the Storage Market Hit Its Peak?