X.D. Network Inc.: TapTap Still Faces Challenges to Justify Its Premium Valuation

04/03 2026

04/03 2026

422

422

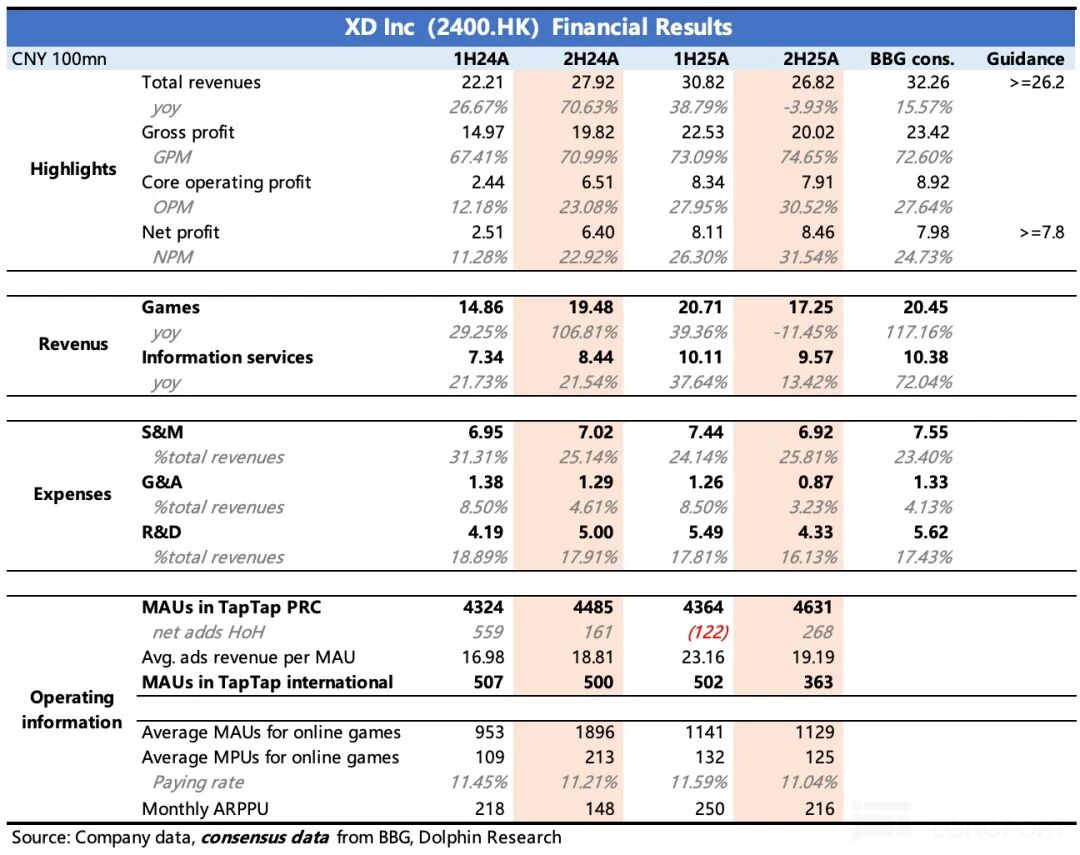

At noon on March 27, Beijing Time, X.D. Network Inc. released its full-year financial results for 2025. Following an earnings preview released in early March, the overall performance exceeded profit guidance.

Bloomberg's consensus expectations lagged behind (failing to account for institutional adjustments post-preview), though the absolute difference in projections was minor. From a profit margin perspective, the company outperformed expectations, largely due to cost and expense optimization measures.

However, Dolphin Research remains cautious about TapTap's significantly slowed growth momentum in the second half of the year. After all, TapTap's performance is pivotal to sustaining its current valuation premium (post-tax operating profit PE ratio stands at 16x, higher than Hong Kong-listed gaming peers, suggesting the TapTap premium is already priced in). While second-half profits benefited from cost reductions and efficiency gains, this alone is insufficient to drive a strong valuation rebound.

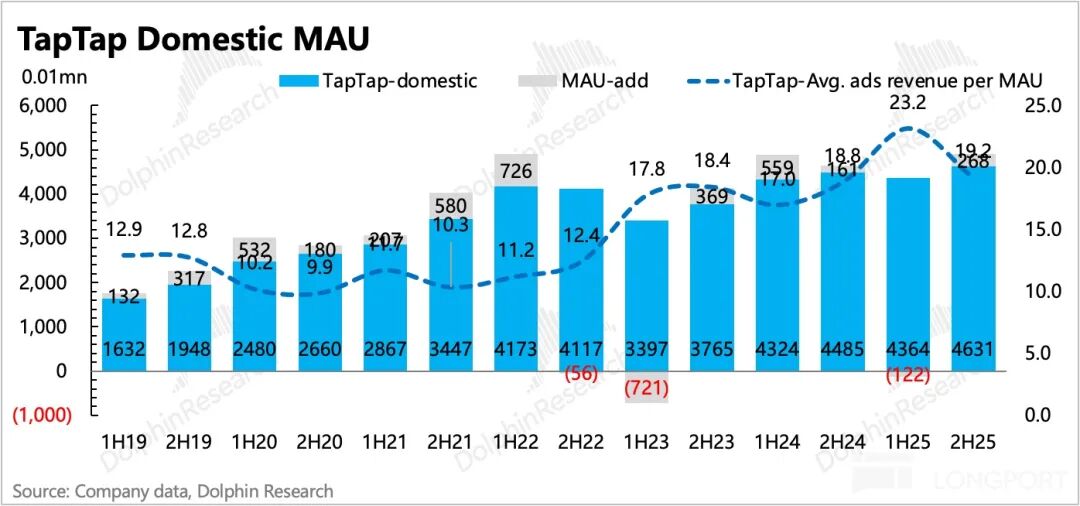

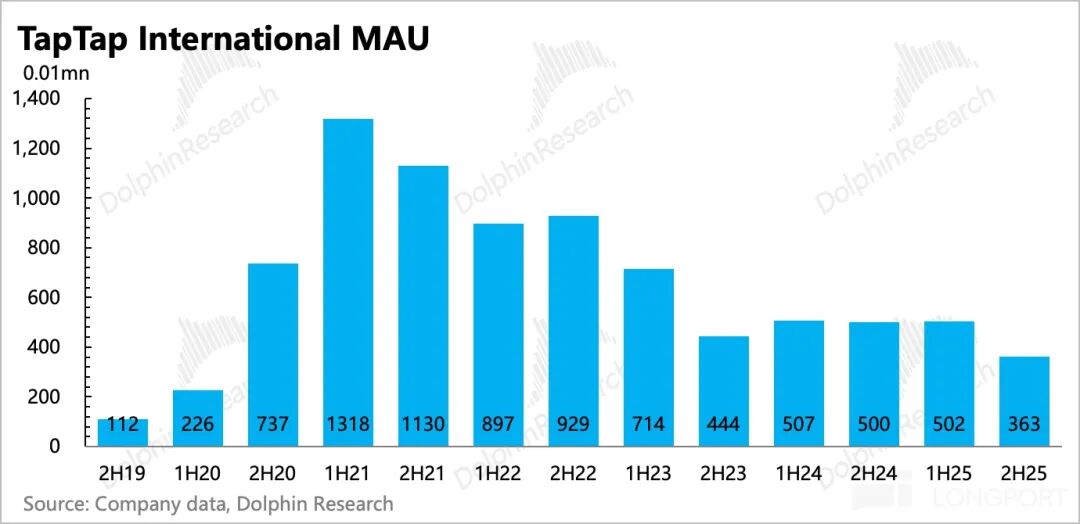

TapTap's user growth decelerated notably this year, likely due to the absence of major self-developed or exclusive high-DAU titles like last year's Heartbeat Town to fuel expansion. The sequential slowdown in advertising revenue growth in the second half raises concerns: Has the monetization potential in advertising reached a plateau?

To revitalize growth, subsequent strategies must focus on either launching more games to boost platform engagement or exploring new revenue streams beyond advertising. For these changes to significantly lift valuations, several factors must align:

1) Two self-developed titles are in the pipeline for launch, likely including Ragnarok Online: Guardians of Love 2. As a long-running IP sequel, it is expected to re-engage some users. Additionally, the deepening operation of Heartbeat Town's international service will sustain user retention. However, for MAU scale to achieve sustained and meaningful growth, breakthroughs from new titles—similar to 2024's successes—remain essential.

2) On the monetization front, TapTap launched an AI-powered game creation tool, TapTap Maker, in January this year, currently in invite-only testing. Short-term user feedback and the visibility of incremental monetization will be critical.

Regarding shareholder returns, the company opted not to pay dividends this year (last year's dividend was HK$0.4 per share, totaling nearly HK$200 million), likely due to the announcement of a HK$400 million share repurchase plan over six months earlier in the year. Assuming repurchase intensity remains steady (with RMB 3.8 billion in net cash on hand, the company can sustain it), this implies an annual shareholder return rate of 2.5%—modest but preferable to nothing for small- and mid-cap investors.

Key Details:

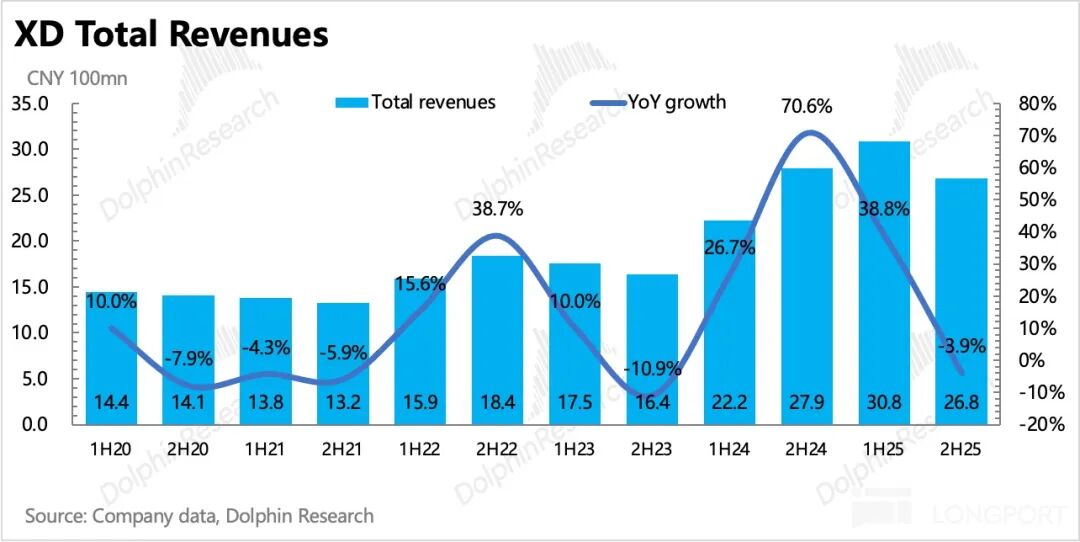

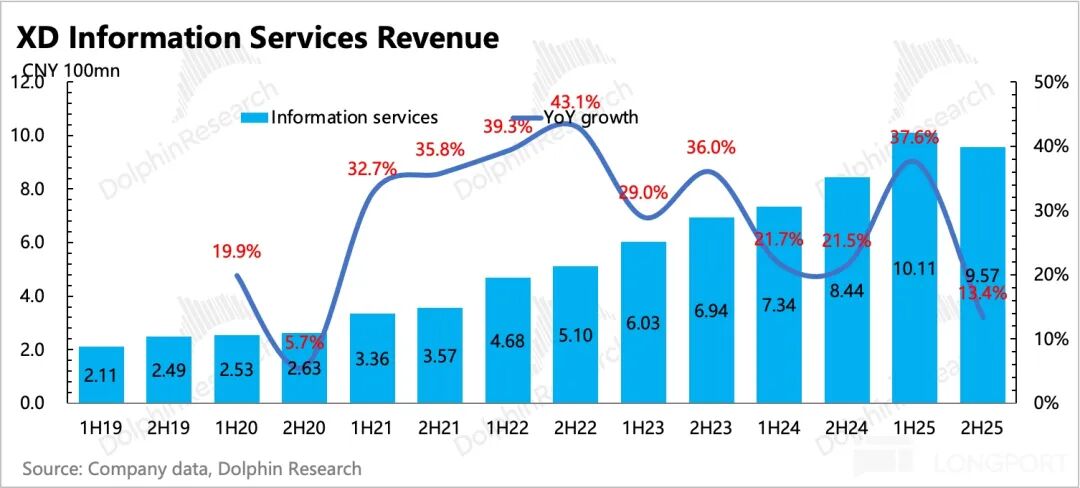

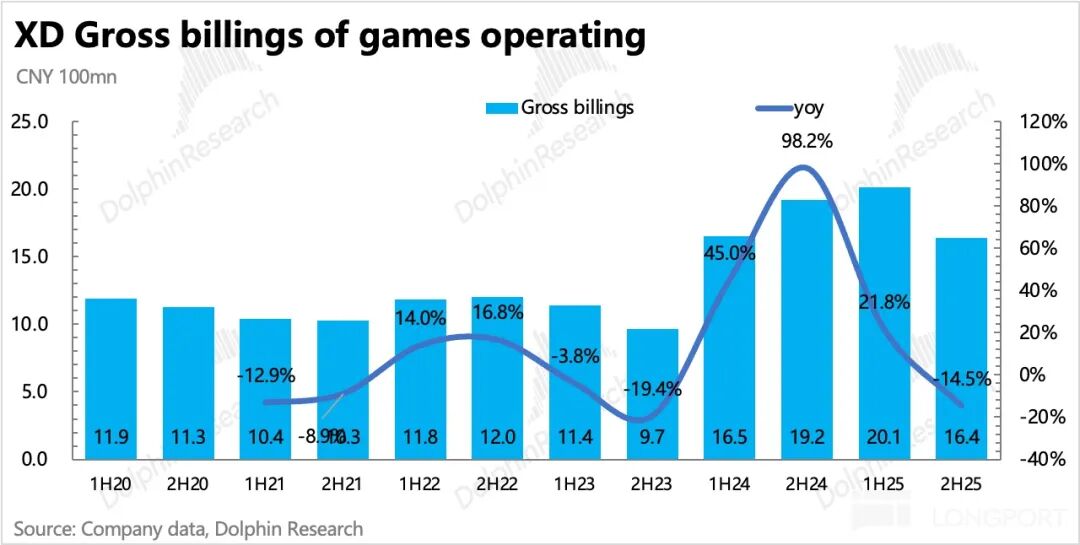

1. TapTap Growth Slowdown: In the second half, TapTap's domestic MAUs saw modest growth, but revenue performance in the peak third quarter lagged the first half, with growth slowing from 38% to 13%. This may reflect slower user growth earlier in the year, reduced advertising budgets from some clients, and intensified competition in advertising channels.

However, MAUs are expected to post significant net growth in the second half (back-calculated from the annual average), likely driven by the July 2025 launch of TapTap mini-games. This year, the performance of new titles like Heartbeat Town International and Ragnarok Online: Guardians of Love 2 will determine whether user scale can continue expanding, thereby reinforcing TapTap's potential as a distribution and publicity platform.

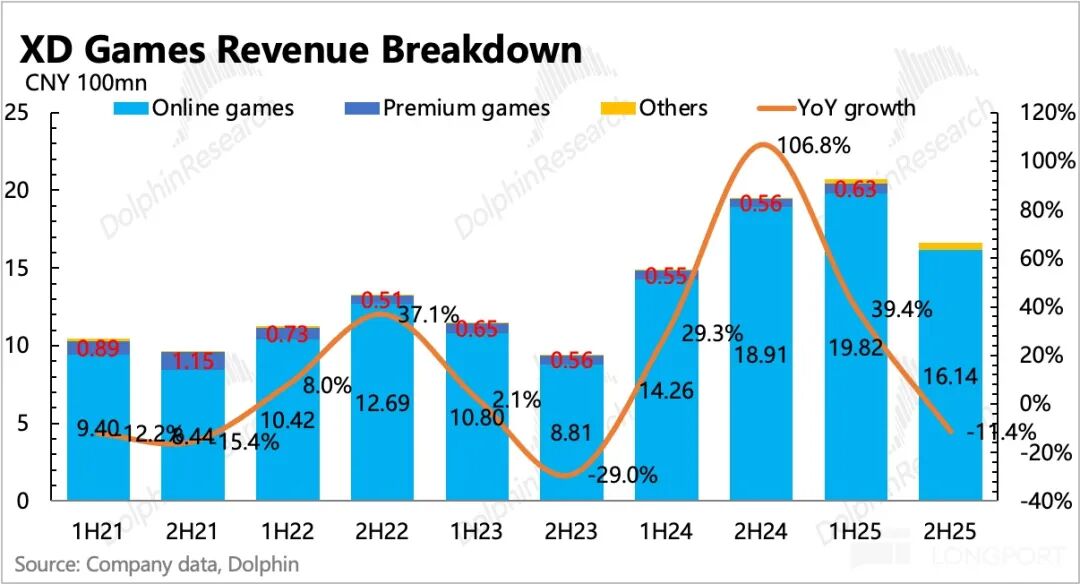

2. Game Revenue Decline YoY Amid High Base: Game revenue fell 11% YoY in the second half, primarily due to a decline in player numbers. New launches included Ether in China, which initially generated high market expectations. Despite a strong launch, its user base declined rapidly, likely due to intense competition from similar titles. The company now considers Ether's operational status mature.

The 2026 pipeline includes Heartbeat Town International and Ragnarok Online: Guardians of Love 2, with another title in development. Heartbeat Town International launched in January. As a high-quality IP sequel operated by X.D. Network for years, Ragnarok Online, a 3D open-world MMO, is expected to generate over RMB 2 billion in first-year TTM revenue. Its first test occurred late last year, and based on typical testing cycles, the official launch may not occur until mid-2026.

Among existing titles, Torchlight, a seasonal competitive game, may see stable or rebounding revenue, especially after acquiring the IP, which facilitates synchronized global promotion and strengthens its influence.

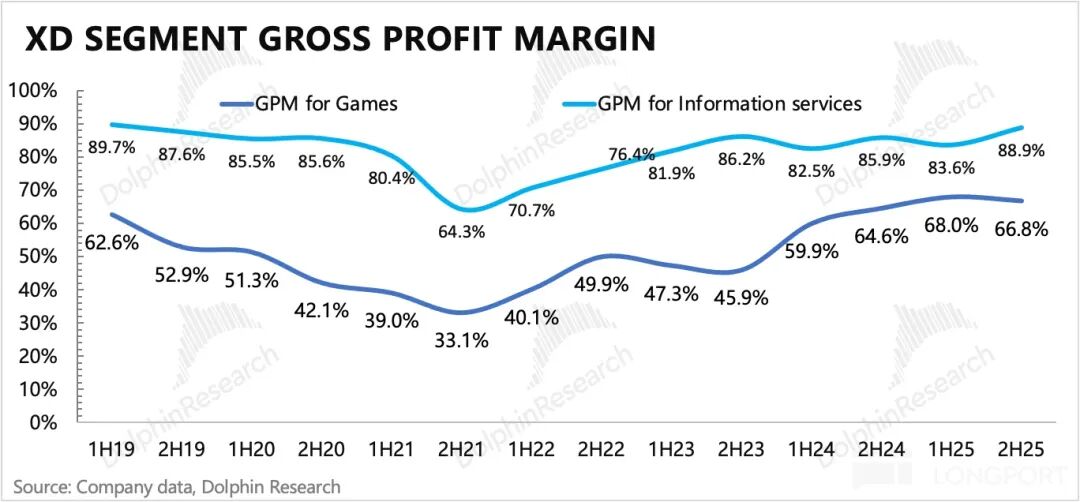

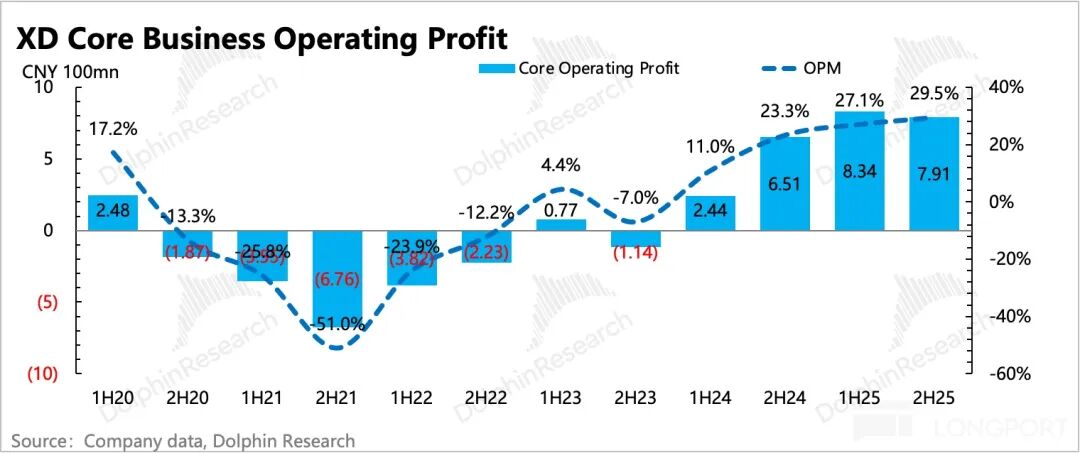

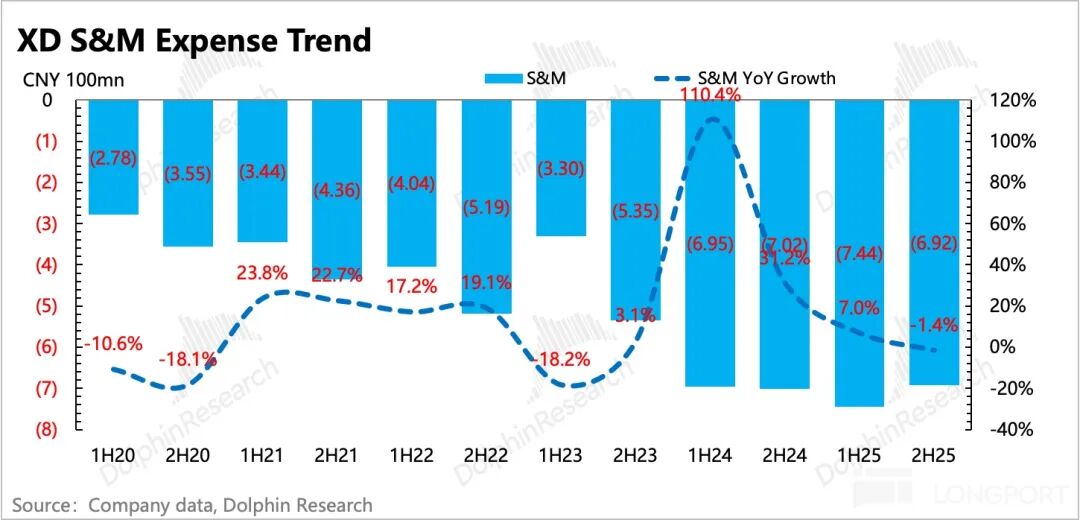

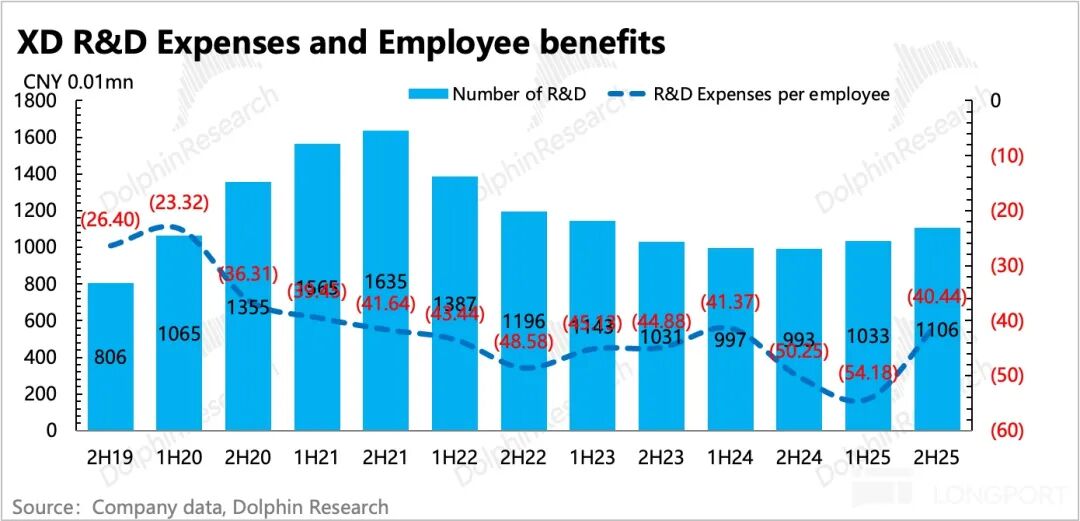

3. "Cost Reduction and Efficiency Improvement" Exceeds Expectations: Profitability was the financial report's highlight, with the second-half core business operating profit margin reaching 31%, up 3 percentage points from the first half. Gross margin contributed 1 percentage point, primarily due to increased revenue share from high-margin TapTap. Operating expenses were optimized by 2 percentage points overall, mainly reflecting a 32% YoY decline in administrative expenses (optimizing by 5 percentage points due to reduced compensation incentives for some management).

This year, game gross margins are expected to improve slightly further, driven by Apple tax adjustments (X.D. Network's exclusive/self-developed games have a lower distribution share on iOS compared to the industry, largely due to significant distribution on TapTap). Additionally, acquiring the Torchlight IP reduced revenue sharing, offsetting domestic revenue sharing from Ragnarok Online: Guardians of Love 2.

4. Performance Metrics vs. Market Expectations

(BBG expectations in the chart below are relatively lagged; institutional expectations were already adjusted after the early March performance preview.)

Financial Indicator Charts:

End of Content

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting requires authorization.

// Disclaimer and General Disclosure

This report is intended for general informational purposes only, providing comprehensive data for readers and users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, preferences, risk tolerance, financial status, or unique needs of any individual recipient. Investors must consult independent professional advisors before making investment decisions based on this report. Any person acting on or referring to the content or information herein assumes all associated risks. Dolphin Research disclaims liability for any direct or indirect consequences or losses arising from the use of this report's data. The information and data herein are derived from publicly available sources and are for reference only. Dolphin Research strives to ensure, but does not guarantee, their reliability, accuracy, or completeness.

The information or viewpoints expressed in this report shall not, under any jurisdiction, be construed as an offer to sell securities, an invitation to buy or sell securities, or as recommendations, solicitations, or endorsements of specific securities or related financial instruments. The information, tools, and materials herein are not intended for distribution to or use by individuals or residents of jurisdictions where such distribution, publication, provision, or use would violate applicable laws or regulations or require Dolphin Research and/or its subsidiaries or affiliates to comply with registration or licensing requirements in those jurisdictions.

This report reflects the personal viewpoints, insights, and analytical methods of its creators and does not represent the official stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright solely owned by Dolphin Research. Without prior written consent from Dolphin Research, no institution or individual may (i) reproduce, copy, duplicate, forward, or distribute any copies or reproductions in any form, and/or (ii) directly or indirectly redistribute or transfer them to unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models