Imported Cars: Once Dominant, Now in Decline

05/20 2026

05/20 2026

664

664

Lead

Introduction

The heyday of imported cars in China has unequivocally ended, with no hope of returning to their former prominence.

When people think of imported cars, they often associate them with high prices, marked-up costs, and long waiting times. However, the landscape has shifted dramatically over the past two years.

Judging by the performance of imported cars in the first quarter of this year, from January to March, China's imported car sales reached 100,000 units. In March alone, only 28,000 imported cars were sold, marking a 12.6% month-on-month decline and a 28.9% year-on-year decrease. The import value also fell in tandem, with a monthly import quota of USD 1.17 billion, a year-on-year drop of nearly 40%. This dual decline in both sales volume and price has become the new norm for imported cars.

Extending the timeline, the downward trajectory of imported cars becomes even more apparent and irreversible.

Twelve years ago, in 2014, imported cars peaked in China, with annual sales reaching 1.43 million units, a record that remains unbroken in the industry. Since then, market enthusiasm has waned, with imports shrinking to 700,000 units in 2024 and further dropping to 480,000 units in 2025, a 32% year-on-year decline. Today's volume of imported cars is merely one-third of its peak.

In addition to declining sales, imported cars also exhibit the characteristic of "increasing volume but decreasing prices," with the average price of imported cars continuing to fall. Models that once relied on high-end positioning and brand premiums to maintain their market position have had to adapt to the more affordable market, with the overall market value steadily declining.

In contrast, while imported cars continue to slump, domestic cars are making significant strides overseas.

In the first quarter of this year, China's automobile exports surged to 2.34 million units, a 53% year-on-year increase. In March alone, 790,000 units were exported, maintaining a stable year-on-year growth rate of 39%. A simple calculation reveals that the scale of automobile exports in March was more than 27 times that of imports.

These stark figures reflect not just short-term market fluctuations but long-term industrial trends. The contrast between the cold market for imported cars and the hot market for domestic cars signifies that China's automobile industry has undergone a complete transformation, officially bidding farewell to the era of import dependence and entering a new phase of independent global expansion.

01 From Price Hikes and Long Waits to Neglect

A decade ago, imported cars were undoubtedly the coveted assets of the domestic auto market and a subtle indicator of social status. At that time, the domestic automotive industry was still in its infancy, with shortcomings in chassis tuning, overall craftsmanship, and brand heritage. German and Japanese imported cars firmly occupied the top tier of the market.

Against this backdrop, popular luxury imported cars were often in short supply, frequently requiring price hikes of hundreds of thousands of yuan and months of waiting for delivery. Even if an imported SUV had a price hike of 500,000 yuan, there was no shortage of willing buyers. Consumers were willing to pay a premium for the imported status, overseas manufacturing processes, and brand value, and imported car companies easily profited in the Chinese market with their inherent advantages.

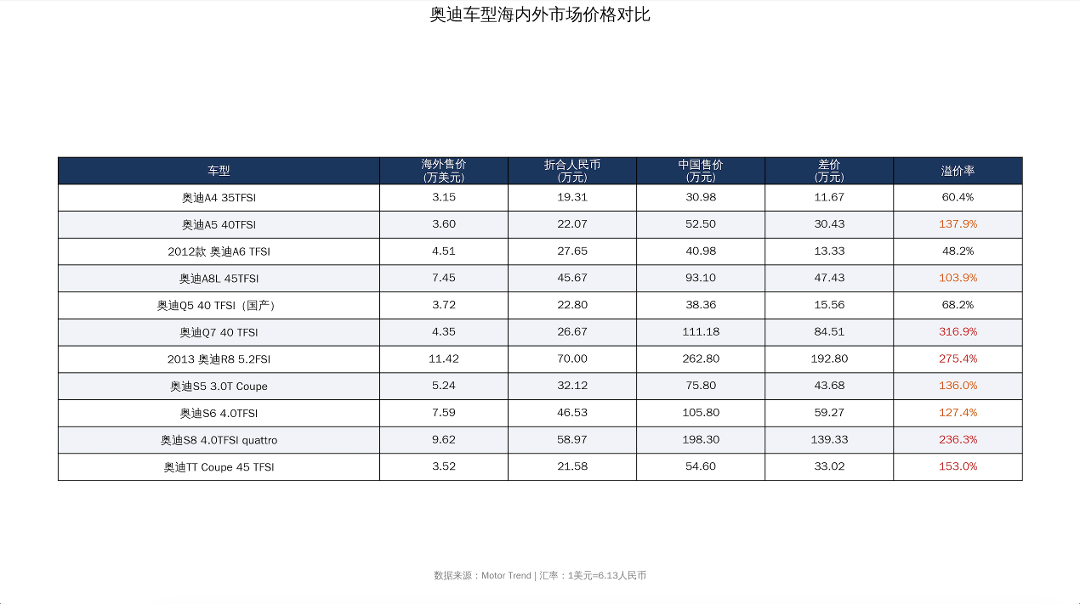

For example, in 2014, the Range Rover was priced at the equivalent of RMB 540,000 in the United States, while in China, it sold for as high as RMB 2.1 million. Some Audi models, identical in product specifications, sold for up to RMB 700,000 abroad, but reached RMB 2.62 million in China. The price difference far exceeded threefold; the model with the highest price hike was the Lexus LM, which even saw price hikes exceeding RMB 1 million at its peak, with some versions reaching RMB 1.7 million, far surpassing the official guide price.

Times have changed, and the rapid development of the new energy vehicle sector has reshaped the competitive landscape of the domestic auto market.

Domestic new energy vehicles have risen rapidly, precisely meeting the needs of domestic users with intelligent configurations, superior materials, and reasonable pricing. They have broken the long-term monopoly of imported luxury cars in the high-end market and launched a "pincer attack" on imported cars across different market segments.

For instance, the full-size SUV segment, once firmly controlled by imported models, has undergone a reshuffle. Domestic high-end models such as the NIO ES8, Zeekr 9X, AITO M8, and M9 have made significant breakthroughs, with product strength comprehensively surpassing imported fuel-powered cars at the same price point through intelligent cockpits, advanced driver-assistance systems, and comfortable driving experiences.

In the even higher-end D-segment executive sedan market, the Zunjie S800 has successfully reached the top, dominating the luxury sedan sales chart above RMB 700,000 for an extended period, leaving established imported luxury cars such as the Porsche Panamera, Mercedes-Benz S-Class, BMW 7 Series, Maybach S-Class, and Audi A8 far behind.

Under the strong pressure from domestic high-end models, a number of imported luxury and ultra-luxury brands are facing significant pressure, generally experiencing declining sales.

In 2025, BMW's imported model sales plummeted by more than 60%, Mercedes-Benz's imported cars fell by nearly 40% year-on-year, and Audi's imported cars also declined by about 40%. Porsche's annual sales in China reached 42,000 units, a 26% year-on-year decline. The ultra-luxury segment also fared poorly, with Bentley's annual sales declining by 13%, and niche supercars such as Ferrari and Lamborghini also continuing to decline.

The most embarrassing situation is undoubtedly that of Maserati, which, affected by sluggish sales, replaced its China region head three times within two years, struggling to gain a foothold in the Chinese market. To revitalize the market and clear inventory, imported luxury cars have one after another lowered their stance and engaged in price wars, with the Maserati Grecale seeing a maximum price reduction of 40%. Once aloof luxury imported cars now can only rely on price reductions to boost sales.

Interestingly, amid the overall industry downturn, Lexus has become the only bright spot in the imported luxury market.

Against the backdrop of a 32% overall decline in the domestic imported car market in 2025, Lexus achieved a 2% year-on-year sales increase, selling 184,000 units for the year, topping the imported luxury brand sales chart. However, this resilience is not unbreakable, as Lexus has also been forced to join the price war, completely breaking the previous market rule of stable pricing and value retention. The industry myth of price hikes and short supply has come to a complete end.

02 Stop Blaming High Tariffs

Faced with the continuous declining sales of imported cars, many people simply attribute the reason to high import tariffs, believing that tariffs raise prices and weaken competitiveness. However, this argument is one-sided and does not hold up to scrutiny.

In 2014, when imported cars were at their industry peak, the domestic complete vehicle import tariff was also maintained at 25%, with a 17% value-added tax, and other consumption taxes varying according to engine displacement. These fees accounted for a maximum of 30% of the final on-road price. In other words, even with taxes and fees factored in, there was still significant room for pricing in the domestic market. Yet, imported cars at that time still saw price hikes and were in short supply.

Moreover, many advantageous domestic industries have long faced high overseas tariff barriers and technological blockades, yet few people speak out against this; only imported car tariffs are repeatedly used as an excuse for declining sales. This double standard is clearly not objective or rational.

What I want to express is that rather than saying the decline of imported cars is essentially due to tariffs, it is more accurate to say that it is due to the catch-up of domestic automobile strength and the transformation of national consumption concepts.

Today, the domestic automotive electrification transformation is basically complete, with the penetration rate of new energy vehicles in China exceeding 60% in April this year. Domestic automakers have deeply cultivated core technologies, achieving generational advantages over imported cars at the same price point in areas such as battery technology, 800V high-voltage platforms, intelligent driver-assistance systems, and intelligent cockpits. The barriers once erected by imported cars based on craftsmanship, chassis, and brand have been one by one broken by domestic brands, and consumers are now abandoning blind belief in imported status and instead focusing on the product strength and user experience of the vehicles themselves.

Don't think that the rise of domestic cars is just "self-entertainment" in the domestic market; overseas performance is the most powerful evidence.

Data shows that in 2025, China's automobile exports reached 7.098 million units, a 21.1% year-on-year increase, ranking first globally for the third consecutive year. In the first quarter of 2026, export data surged again, with 2.34 million units exported and a 53% year-on-year growth rate, continuously breaking industry records.

At this stage, leading automakers such as BYD, Chery, and SAIC have initiated a full-industry-chain global expansion mode, achieving not only increasing sales in major global markets but also investing in factory construction to realize localized production, research and development, and sales.

Based on this positive momentum, industry institutions predict that China's automobile exports are expected to exceed 8 million units in 2026, with new energy vehicle exports reaching 3.5 million units. The technological strength and product quality of Chinese automobiles are gaining recognition in the global market.

As for the future of imported cars, the industry has already given a clear prediction.

Some industry insiders say that imported cars will continue to gently decline over the next 3 to 5 years, with the rate of decline gradually slowing and eventually stabilizing at a volume of around 200,000 units, with market share compressed to 1%-2%. In the long run, imported cars will not completely disappear but will thoroughly retreat to niche segments, retaining only ultra-luxury custom and classic nostalgia models to serve a very small portion of high-end circles.

From a peak of 1.43 million units to less than 500,000 units today, and then to a niche scale of 200,000 units in the future, the golden age of imported cars in China has unequivocally ended. Correspondingly, the golden age for Chinese automobiles is just unfolding.

Editor-in-Chief: Shi Jie Editor: He Zengrong

THE END

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry