Global Server Market Resonance: When Will Inspur Information Seize Its Moment?

06/03 2026

06/03 2026

441

441

From May 21 to the present, in fewer than ten trading days, Dell's stock price has skyrocketed by nearly 80%, buoyed by significant tailwinds in the server sector. Financial reports reveal that Dell's AI server revenue surged to $16.1 billion in the first quarter, marking a more than sevenfold increase. The company also reported a backlog of $51.3 billion in orders and secured $24.4 billion in new orders within a single quarter.

Dell has emerged as a key beneficiary of the increased capital expenditures by AI giants, akin to the memory and upstream materials sectors. Concurrently, companies in the industrial chain, such as Foxconn Industrial Internet, have recently reached all-time highs in their stock prices, underscoring the expanding impact of sector growth.

The server industry, once considered somewhat 'ancient,' has found renewed vitality in the AI era. However, Inspur Information, another major player that reached new heights last year, is still on the path to reclaiming lost ground. Given the industry's surging popularity, how close is it to catching the next 'wave'?

I. The Rise and Fall of a Seller's Market

Over the past two years, the AI server industry has gradually entered a distinctive 'seller's market' phase.

In the initial stages, around 2023, servers were still grappling with a prolonged period of overcapacity. While ChatGPT had gained traction, the market had not yet witnessed significant increases in capital expenditures or large-scale applications.

By 2024, the landscape had transformed dramatically. IDC data for that year indicated that global server shipments reached 3.5837 million units in the second quarter of 2024, marking a 16.68% year-on-year increase, while the global server market size surged by 64.06%. Brand-name server manufacturers excelled, with shipments reaching 2.2781 million units, a 20.82% year-on-year increase.

Such growth was clearly not driven by traditional internet businesses alone. AI began to influence the development of numerous enterprises, fueling this sudden surge.

During this phase, the market's defining characteristic was its 'chip-centric' nature. NVIDIA's flagship GPUs were in short supply, with delivery cycles extending to six months or longer. Customers were willing to pay substantial deposits in advance, accept price premiums, and endure long waits to secure capacity. At this juncture, server manufacturers' primary capability revolved around obtaining chips and ensuring product delivery.

For major global AI server manufacturers between 2024 and 2025, performance was almost entirely dictated by their respective supply chain capabilities. While product design, system optimization, and customer service were also valuable, they did not alter the primary battleground amid the chip shortage.

From a financial perspective, despite rapid scale expansion, the inherent nature of servers meant that manufacturers still faced profit margin compression. Especially with rising chip prices and more price-conscious major clients, server manufacturers had to navigate both favorable and unfavorable market conditions simultaneously.

Take Inspur Information as an example. In 2025, Inspur Information reported revenue of 164.7 billion yuan and net profit of 2.4 billion yuan, with a net profit margin of 1.46%, reflecting the characteristic of a large market with thin profits. However, as the market evolved, clearer signals emerged.

The first change was an improvement in the supply side. As NVIDIA continued to drive chip updates and capacity expansion, major manufacturers became more confident in increasing capital expenditures to acquire computing power facilities. Moreover, China witnessed the rise of domestic chips.

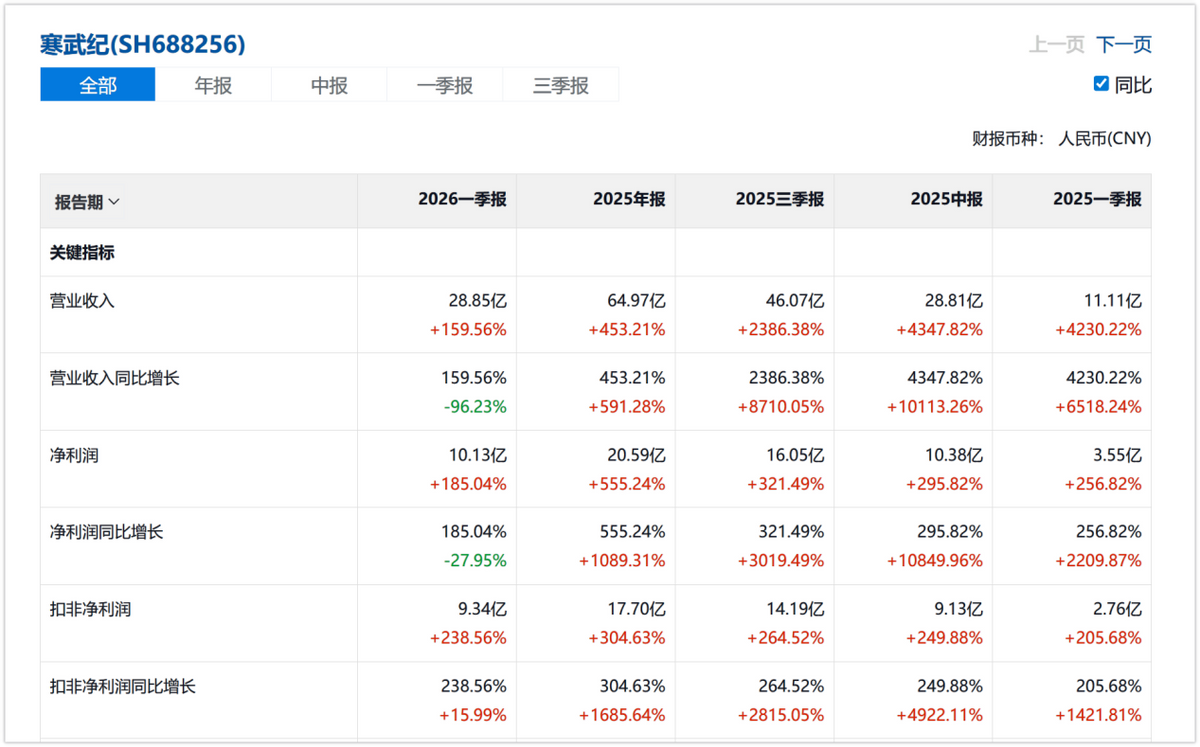

According to IDC data, China's AI chip shipments increased by 47% year-on-year in 2025, reaching 4 million units, with the domestic chip share rising from 30% in 2024 to 41%. Signals such as Cambricon's contract liabilities surging from 6,000 yuan to 396 million yuan in the first quarter and inventory maintaining a high level of 4.5 billion yuan frequently emerged, indicating that domestic chips had entered the server supply chain on a large scale.

The second change was a differentiation in demand structure. Early AI server buyers were primarily leading cloud providers and a few AI companies, characterized by large purchase volumes and strong bargaining power. However, the popularization of open-source models like DeepSeek, the explosion of Agent applications, and the large-scale deployment of AI by small and medium-sized enterprises (SMEs) and industry clients created a unique force, causing demand to disperse to more medium-sized or smaller enterprises.

From a demand perspective, different types of enterprises have vastly different server requirements: large cloud providers prioritize ultimate performance, SMEs value ease of use and cost-effectiveness, while industry clients in finance and healthcare prioritize security and compliance. The era of single standardized products is fading.

Change brings opportunity, and server manufacturers have encountered their window of fortune.

II. The Interplay of Seller's and Buyer's Markets Creates New Rules

When chips are no longer scarce and demand becomes dispersed, customers are eager to make purchases but also highly emphasize 'making the right choice.' A fascinating phenomenon has emerged: servers tend toward a seller's market due to supply constraints while also exhibiting characteristics of a buyer's market due to intense competition and specialized demand.

Amid this trend of symbiotic competition, three rules are gaining increasing influence.

The first new rule is the shift from 'chip acquisition capability' to 'adaptability.'

In the past, securing sufficient chips and ensuring delivery seemed sufficient to gain customer recognition. However, at this stage, chips are no longer the sole critical issue; the question is what solutions customers need.

Different chip platforms vary in performance characteristics, software ecosystems, and supply chain maturity. Server manufacturers must consider variables like Huawei's Ascend rather than being tied to a single platform. Adaptability determines which clients you can acquire, which scenarios you can excel in, and how much competitive space you can occupy.

The second new rule is the transition from 'standardized hardware' to 'scenario-based solutions.'

Previously, seller-friendly markets often involved selling the same configuration to everyone. However, when customers have choices, they focus more on whether servers can solve specific business problems. For example, financial clients may prioritize data security and compliance, manufacturing enterprises care about stability and long-term operational costs, while SMEs are concerned about deployment thresholds and ease of use.

Manufacturers capable of providing customized solutions, bundled software, and services for different scenarios hold pricing power.

Earlier this year, when 'Lobster' (a reference to a popular AI model or application) sparked interest in intelligent agents, many enterprises sought solutions tailored to enterprise-level needs. Inspur timely launched its 'QiQianXia' solution for deploying OpenClaw intelligent agents in enterprises. It is not just a server but a complete system integrating scheduling, security, and monitoring. When customers no longer buy hardware but 'runnable intelligent agents,' profit margins can potentially improve.

Finally, another notable rule is that the industry's service focus is expanding from front-end sales to full-cycle services. In traditional markets, the server sale marked the end of the transaction, with some standard operational maintenance provided. Today, customers care more about full-lifecycle outputs, requiring manufacturers to proactively build long-term customer relationships, especially in conjunction with specific scenarios.

III. Chinese Enterprises at the Transition Node

Understanding this industry transition provides new insights into several key phenomena in the server sector.

Why has Dell's market value surged 150% from its lows? Primarily due to improved market expectations. The reasons for Dell's higher valuation lie not in its simple assembly and manufacturing capabilities but in its stronger competitive advantages in the market: a global sales network, deeply entrenched enterprise customer relationships, and end-to-end IT service capabilities.

These capabilities were unremarkable in the traditional server and PC markets, characterized by intense homogenized competition. However, at this stage, they represent the ability to influence the new competitive landscape.

Correspondingly, theoretically, companies like Inspur Information should also benefit. However, in May, Goldman Sachs downgraded Inspur's rating in a research report.

Goldman Sachs remains optimistic about Inspur's growth over the next three years but believes that with the substitution of domestic chips and a decline in average server prices, manufacturers' gross margins will face pressure. Goldman Sachs apparently views the server sector from a traditional perspective. It also upgraded Cambricon's rating, suggesting a certain 'see-saw' relationship between chips and servers. Therefore, if the core value of servers lies in assembly, then as chip prices fall and volumes increase, servers must inevitably follow suit.

However, in reality, given the diverse and potentially 'quirky' tendencies in demand, as AI applications continue to explode and intelligent agents evolve, the rules governing what the market needs in servers are not set in stone. In the future, another possibility exists: if the value of server companies no longer comes from assembling chips but from providing solution capabilities, then the notions of declining average prices and profit margin compression become less tenable. The key lies in whether companies can establish new value-adds in system software, solution integration, and service delivery.

In the first quarter of 2026, Inspur Information reported revenue of 35.4 billion yuan, with gross margins recovering from 4.88% to 6.64% and net margins from 0.98% to 1.71%. This indicates that Inspur is actively shedding low-margin orders and focusing on high-value clients and solution-oriented products. Combined with our speculation, this represents a rational strategic choice.

When enterprises realize that scale expansion is merely a foundational growth method, adjusting order structures and improving unit output quality become more pragmatic directions. Currently, Inspur Information's YuanBrain servers and workstations are being continuously promoted and applied.

From a product form perspective, this direction is correct. They are not just hardware products but system-level solutions integrating deployment, scheduling, security, and monitoring. This aligns with the market's competitive logic—providing complete solutions that 'directly solve problems' rather than just basic hardware components.

Thus, Inspur Information currently occupies a unique position. Its supply chain scale and product line completeness give it a leading advantage among Chinese server manufacturers, with broad adaptability across the entire market. However, its new model is still in the accumulation phase, currently in a window of transition between old and new paradigms. This transformation does not happen overnight. Loosening on the supply side, decentralization on the demand side, and evolution in product forms are all continuously driving this process.

For server manufacturers, the key question is not whether gross margins are higher or lower this quarter compared to the last but where your competitive barriers lie when customers have more choices. The winners and losers in the AI server industry will emerge from this competition.

-

![]()

Agent Hardware Boom! What Exactly Is Qualcomm's 'Computing Continuum'?

-

![]()

A New Chapter in Computing Power Revolution: Cerebras Surges 51% in Market Debut, Leveraging OpenAI to Challenge NVIDIA's Computing Dominance

-

![]()

Chinese Startup Raising 5 Billion in Three Months Outperforms NVIDIA in North America

-

![]()

Global Server Market Resonance: When Will Inspur Information Seize Its Moment?

-

![]()

When Google I/O Comes to Douyin, Cutting-Edge Tech Finds a New Stage

-

![]()

Anthropic Secretly Files for IPO: Nearing a Trillion-Dollar Valuation, Initiating the First AI Listing

-

![]()

Huawei Reclaims Leadership, Honor Faces Challenges in Fierce Smartphone Market

-

![]()

"Mass Production in Approximately 18 Months": Dreame Technology Faces Time Constraints in Car Manufacturing