Can Chinese Automakers Sidestep the Global Expansion Pitfalls Faced by Japanese Brands?

04/02 2026

04/02 2026

677

677

Introduction

History has a curious way of repeating itself, often in unexpected manners.

Last year marked a significant milestone for Chinese automakers, as they surpassed Japan for the first time, achieving nearly 27 million global vehicle sales and claiming the top spot in worldwide auto sales. This achievement was built on the foundation of eight consecutive years as the global leader in new energy vehicle (NEV) production and sales, signaling a qualitative transformation in China's automotive industry.

However, as the industry is keenly aware, being a major automotive producer does not automatically translate into being a global powerhouse. Thus, while claiming the sales crown is noteworthy, it does not instantly make China a brand superpower. With the EU imposing anti-subsidy tariffs, international oil prices surging and creating a window of opportunity for NEVs, and global trade protectionism on the rise, the true test for Chinese automakers lies in their ability to sustain global leadership.

For Chinese automotive brands, the looming question is: How should they navigate the complexities of globalization? Perhaps history can offer some insights. Looking back, Japanese automakers faced similar challenges in the latter half of the 20th century—trade frictions, technological skepticism, and market barriers—before ultimately becoming global leaders through lean management and technological breakthroughs.

Take Toyota as a case in point. Its eight-decade journey, from the Crown sedan's failed U.S. debut to the Corolla becoming the world's best-selling model, provides a compelling case study for Chinese automakers. Can China's automakers learn from Japan's globalization path and forge a new route in the era of smart electric vehicles?

01 How Did Toyota Go Global?

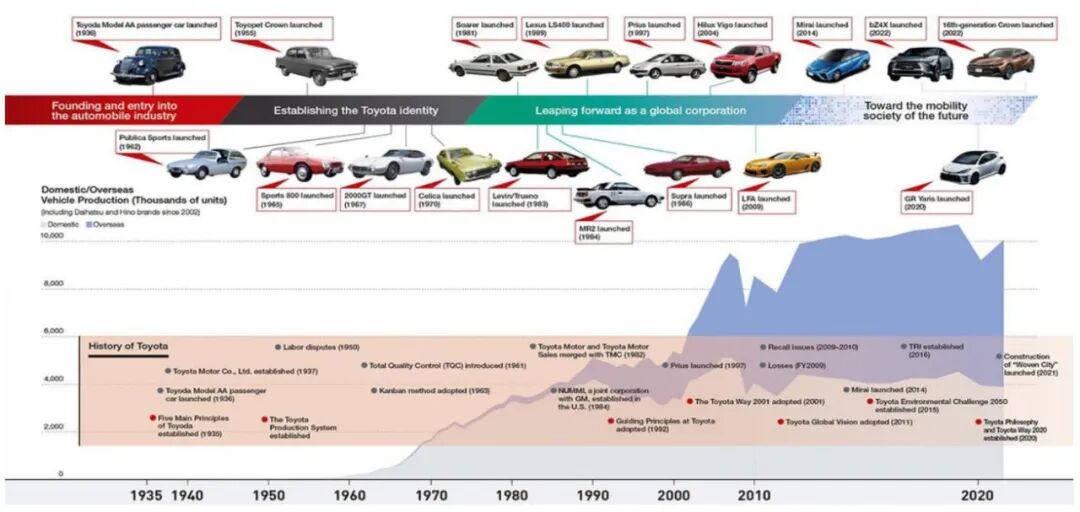

Toyota's globalization journey began with setbacks in the 1950s. In 1957, the company exported the Crown sedan to the U.S., only to discover within a month that its headlights fell short of U.S. regulations and its engine struggled on American highways. This failure became Toyota's most valuable lesson in globalization, teaching it the importance of understanding and adapting to local markets.

The 1960s marked a turning point for Toyota. In 1965, it launched the Corona RT43L, redesigned specifically for the U.S. market with an automatic transmission, a 1900cc engine, and a competitive price tag of $1,860—positioning it between American and European models. The car quickly gained traction among consumers.

The 1966 Corolla further solidified Toyota's global DNA with its "80-point plus α" design philosophy: achieving at least 80 points in all performance metrics while excelling in one area (the α). This affordable sedan boosted Toyota's U.S. sales from 98,000 to 155,000 units after its 1968 U.S. debut, making it America's second-largest imported brand.

From 1961 to 1979, Toyota's exports surged from 12,000 to 1.384 million units, while overseas production grew 82-fold, completing its transformation from a Japanese automaker to a global player. This 19-year journey was undoubtedly arduous and required significant strategic adjustments.

What truly elevated Toyota to world-class status was its ability to survive the dual challenges of the 1970s oil crises and trade frictions. When the first oil crisis hit in 1973, international oil prices soared from $3 to $12 per barrel, shifting U.S. consumer preferences toward fuel efficiency.

Toyota capitalized on this shift by avoiding direct competition with American mainstream models and focusing on compact cars. It leveraged the oil crisis to enter global markets more effectively. Critically, Toyota established its lean production system, achieving minimal production cuts during demand slumps and rapid ramp-ups during recoveries through just-in-time (JIT) inventory management, zero inventory goals, and continuous improvement practices.

This system later became a management classic, underpinning Toyota's global competitiveness and serving as a model for other industries.

In the 1980s, U.S.-Japan trade frictions intensified, forcing Japan to implement voluntary export restraints. Toyota's response became a textbook case in globalization: in 1984, it jointly established NUMMI with General Motors, marking Toyota's true globalization breakthrough by producing Toyota-quality vehicles with American workers and facilities.

Toyota's overseas expansion followed four clear phases: Phase 1 (1980-1984) focused on establishing bases in Asia and Africa; Phase 2 (1985-1991) built North American capacity through NUMMI and other joint ventures; Phase 3 (1992-2001) expanded European local production; and Phase 4 (2002-2008) completed production layouts in North America, Asia, and Europe.

By 2007, Toyota held 16.1% of the U.S. market, second only to GM. Overseas sales grew from under 1 million in 1980 to over 2.6 million in 2007, completing the transition from an export-oriented company to one with localized operations.

Toyota's 70-year globalization journey reveals key principles: maintaining strategic focus on technological routes, aligning supply and demand, adapting market entry strategies (from direct exports to joint ventures to wholly owned subsidiaries), and flexibly navigating trade barriers. This provides a complete blueprint for later entrants into the global market.

02 China's New Era of Automotive Globalization

History is repeating itself, albeit in a new context. Today, Chinese automakers stand at a crossroads similar to Toyota's past. In the first two months of 2026, China exported 1.352 million vehicles (a 48.4% year-over-year increase), including 583,000 NEVs (a 110% year-over-year increase), accounting for over 40% of total exports.

Like Toyota during the oil crisis, persistently high international oil prices amplify the lifecycle cost advantages of NEVs, boosting China's global competitiveness. Geely's exports surged 129% year-over-year in January-February, while BYD's overseas sales grew 51%, showing strong momentum among leading Chinese automakers.

However, China also faces trade barriers akin to those Toyota encountered in its U.S.-Japan frictions. In mid-2024, the EU imposed anti-subsidy tariffs on Chinese EVs, but in January 2026, it released guidelines allowing Chinese exporters to replace tariffs with minimum price commitments, effectively shelving the dispute and opening a new avenue for negotiation.

More notably, Chinese automakers are exploring new globalization paths beyond Toyota's experience. Reports indicate that Chinese firms in Europe are shifting from an export-dominated trade model to a symbiotic one of "vehicle exports + technology transfer + local production."

This represents an upgrade from mere product exports to a comprehensive output of technology, management, and brands. Chinese automakers can now learn from Toyota's core lessons while leveraging their unique strengths and the current global market dynamics.

Critically, they must seize the technological transformation window by maintaining focus on electrification and intelligence. Toyota's persistence in fuel efficiency during the oil crisis paid off globally. Today, Chinese automakers lead in NEV cost-effectiveness (energy consumption, pricing, configurations).

In terms of intelligence, China leads globally in technologies like LiDAR, domain controllers, and vehicle-road-cloud integration, with L2 penetration reaching 64.2% and navigation-assisted driving at 22.9%. Academician Li Keqiang notes that China has shifted from catching up on individual technologies to innovating in system architectures centered on vehicle-road-cloud integration, marking a significant leap forward.

As many auto executives have said, globalization for Chinese brands essentially means local adaptation. Market entry should shift from being export-driven to localized deep cultivation. Toyota, after facing trade frictions, adopted strategies like joint ventures and wholly owned plants to better integrate into local markets.

Chinese automakers now have more flexible options. Leapmotor's joint venture with Stellantis leverages global channels for European expansion. XPENG, GAC, and others use Magna's European plants to reduce policy risks through local supply chains, demonstrating a more nuanced and strategic approach.

Meanwhile, Chinese firms can adopt asset-light strategies, repurposing idle factories of international automakers to lower overseas investment risks. Examples include Chery taking over Nissan's South African plant, Geely's partnership with Renault in Brazil, and Great Wall's negotiations with Mercedes-Benz over a shared South African factory. These diversified entry methods surpass Toyota's earlier options and showcase Chinese ingenuity.

While Chinese automakers face intense domestic competition, Toyota too was once labeled a "price cutter" during its globalization phase. It ultimately built brand value through lean management and technological upgrades. Chinese automakers must similarly prioritize value over price wars to cultivate long-term brand competitiveness and sustainability.

Looking back from 2026, all automotive professionals recognize that China's auto globalization is undergoing a critical transition from scale expansion to quality advancement. The question remains: Can China forge a globalization path that surpasses the Japanese or even Toyota's model? The answer is worth anticipating and will shape the future of the global automotive industry.

Editor: Cao Jiadong Sub-editor: He Zengrong

THE END

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?