Rapid Scale Growth, Yet 5.6 Billion Yuan in Losses: New Energy Vehicle Insurance Poised for a Profitability Turning Point

04/03 2026

04/03 2026

542

542

On March 31, 2026, the China Association of Actuaries and China Banking and Insurance Information Technology Management Co., Ltd. jointly released the 2025 operating data for new energy vehicle insurance, revealing a mixed performance for the industry. The premium scale reached 190 billion yuan, with 43.58 million vehicles insured, marking year-on-year growth of 40.1% and synchronous expansion, respectively. This underscores the robust growth momentum of the new energy vehicle insurance market. However, the reality of 5.6 billion yuan in underwriting losses and 143 high-claim vehicle models also highlights that the industry remains trapped in a structural dilemma, with "car owners complaining about high costs and insurers lamenting losses."

The number of new energy vehicles in the Chinese market is surging, and competition in the new energy vehicle insurance sector is becoming increasingly complex. Traditional insurers are exploring profit models amid loss pressures, automotive companies are leveraging their data and ecosystem advantages to enter the insurance market for their own brands, and regulators are paving the way for industry transformation through policy guidance and institutional innovation.

▍Profitability Challenges Amid Rapid Scale Growth

The dilemma facing new energy vehicle insurance stems not from a single factor but from the interplay of technical characteristics, industrial ecosystems, and market mechanisms. PICC Property & Casualty pointed out in an industry report that new energy vehicle insurance faces three core challenges: high claim rates, escalating repair costs, and rising personal injury compensation. These three pain points collectively drive up the industry's combined cost ratio, squeezing profit margins.

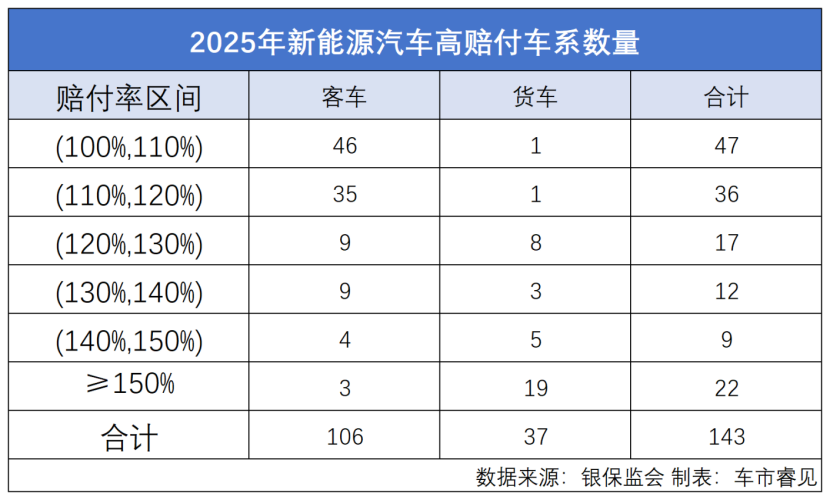

From a claims perspective, the electrification and intelligent features of new energy vehicles make their risk profiles significantly different from those of traditional fuel vehicles. Data indicates that the overall claim rate for new energy vehicles is approximately 20% higher than that of fuel vehicles. Key contributing factors include misjudgments by intelligent driving assistance systems, battery thermal runaway risks, and expanded collision losses due to lightweight vehicle body designs. More notably, the number of high-claim vehicle models continues to rise. In 2025, 143 vehicle models had a claim ratio exceeding 100%, an increase of six from the previous year. Among them, high claims for trucks (≥150%) are particularly pronounced, with 37 high-claim truck models becoming the core source of industry claim pressure.

Escalating repair costs are another major driver of losses in new energy vehicle insurance. Due to the high technical barriers of core components such as batteries and electric drives, repair channels are highly concentrated within automotive companies' authorized systems, leading to persistently high parts prices and labor costs. Taking battery replacement as an example, the battery cost for mainstream new energy vehicle models accounts for 40%-60% of the vehicle's total value, with a single battery replacement often exceeding 100,000 yuan, far surpassing the repair costs of fuel vehicles in the same class. Meanwhile, electronic components such as sensors and chips in intelligent driving systems are not only expensive but also require specialized equipment and software authorization for repairs, further driving up claim costs.

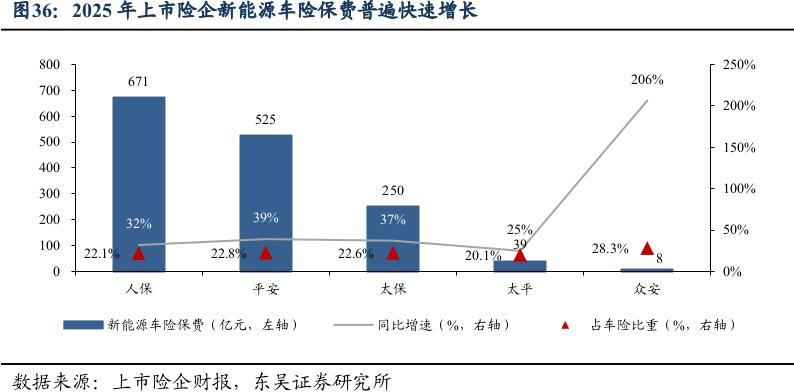

Leading traditional insurers, leveraging their resource and technological advantages, have taken the lead in achieving profitable underwriting for new energy vehicle insurance, setting a benchmark for industry transformation. Among A-share listed property and casualty insurance companies, PICC Property & Casualty achieved a combined cost ratio below 100% for new energy vehicle insurance in 2024. In 2025, it underwrote 15.56 million new energy vehicles, a year-on-year increase of 34.3%. The annual premium income from new energy vehicle insurance reached 67.1 billion yuan, a year-on-year increase of 31.9%, with new energy vehicle premiums accounting for 22.1% of total premiums, up 4.9 percentage points year-on-year. Management further stated at a recent earnings briefing, "We expect the combined cost ratio for new energy vehicle insurance to further improve in 2026, with profitability levels continuing to rise."

At the same earnings briefing, Fu Xin, Deputy General Manager and Chief Financial Officer of Ping An Insurance, revealed when introducing Ping An's new energy vehicle insurance that the company's new energy vehicle insurance business has achieved profitable underwriting, with the combined cost ratio reduced to below 100%. Chen Hui, General Manager of China Pacific Property Insurance, stated when discussing new energy vehicle insurance that in 2025, the company's new energy vehicle insurance growth rate exceeded the overall growth rate of vehicle insurance, with significant improvements in overall business costs for new energy vehicle insurance. The home-use new energy vehicle insurance business has now entered a stable profitable range.

The profit breakthroughs of leading insurers contrast sharply with the struggles of smaller insurers. Data shows that in 2025, the combined cost ratios for new energy vehicle insurance among smaller insurers were generally above 105%, with some companies even exceeding 110%, trapped in a vicious cycle where more underwriting leads to greater losses. The core reasons for this phenomenon lie in insufficient risk identification capabilities, lack of data accumulation, and weak bargaining power in repair channels, leaving smaller insurers unable to accurately price high-risk models or control claim costs.

▍New Entrants from Automotive Companies, Traditional Insurers Accelerate Transformation

The rise of automotive company-affiliated insurance has injected new vitality into the new energy vehicle insurance market, with core advantages lying in data closed loops and industrial chain synergy. In 2025, BYD Insurance achieved insurance business revenue of 2.871 billion yuan, doubling year-on-year, with a net profit of 93.624 million yuan, turning from loss to profit. The combined cost ratio dropped to 102.49%, and the combined claim ratio improved to 97.28%, setting a benchmark for profitable automotive company-affiliated insurance.

BYD Insurance's success stems from its ability to control full-lifecycle data for new energy vehicles. As a vehicle manufacturer, BYD can access core information such as battery health status, motor operation data, and intelligent system fault records, providing a precise basis for risk assessment and pricing. Meanwhile, BYD Insurance leverages its parent company's repair network and parts supply system to significantly reduce claim costs, achieving an ecological closed loop of "insurance + repair + data."

In addition to BYD, automotive companies such as Tesla and Xiaomi are also actively expanding into the insurance business. Tesla Insurance, leveraging its Autopilot data advantages, has achieved personalized pricing based on driving behavior, with low-risk drivers eligible for premium discounts of up to 30%. BNP Paribas Cardif Tianxing Insurance, a stakeholder in Xiaomi Group, has also begun piloting renewal business for existing Xiaomi vehicle customers.

The rise of automotive company-affiliated insurance not only provides the industry with a new profit model but also drives the optimization of the entire new energy vehicle insurance ecosystem. On the one hand, the competitive pressure from automotive company-affiliated insurance prompts traditional insurers to accelerate digital transformation and data accumulation. On the other hand, to reduce insurance costs, automotive companies are beginning to consider repair economy and risk control during the product design stage, driving cost optimization throughout the full lifecycle of new energy vehicles, from "manufacturing" to "usage."

The synergy between government policies and market innovation is accelerating the transformation of the new energy vehicle insurance industry. In March 2026, the China Banking and Insurance Regulatory Commission, jointly with multiple departments, issued the latest policies for new energy vehicle insurance, further clarifying the industry's development direction. Key content includes: addressing issues of overly high premium pricing for certain vehicle models and overly broad vehicle classifications, reducing unreasonable premiums from the pricing source; calculating premiums at the lowest tier for low-risk home-use electric vehicles to avoid "one vehicle's high cost driving up industry-wide premiums"; and supporting battery-separable insurance models to provide differentiated insurance solutions for battery-swappable vehicle models.

Meanwhile, the development of a risk classification system for domestic new energy vehicle models is underway. The introduction of this classification system will encourage automotive companies to focus more on improving vehicle safety and repair economy, ultimately reducing vehicle repair costs and benefiting new energy vehicle consumers. Under policy guidance, the industry has responded positively. Data shows that with the increasing proportion of older vehicles, improved driving habits, and the popularization of assisted driving technology, the claim rate for new energy vehicles is gradually declining.

In particular, the popularization of AEB (Automatic Emergency Braking System) has significantly reduced accident risks, with trucks equipped with AEB experiencing a 7% lower claim risk compared to those without. According to national standards, starting July 1, 2026, new heavy commercial trucks will be required to have AEB as standard equipment, with the requirement extending to light trucks starting January 1, 2028. This policy will significantly reduce the high-claim risks for trucks, providing crucial support for industry profitability recovery.

With technological advancements, data accumulation, regulatory guidance, and industrial synergy, the new energy vehicle insurance industry is expected to achieve overall profitability balance by 2026-2027. Industry insiders predict that the combined cost ratio for new energy vehicle insurance will further optimize to below 98% in 2026 and is expected to drop to around 95% by 2027, achieving profitable underwriting across the entire industry.

For vehicle owners, this means more reasonable premiums, more comprehensive coverage, and a wider range of innovative products such as battery-separable insurance and personalized pricing. In the future, the new energy vehicle insurance market will feature a collaborative development model among "insurers + automotive companies + tech companies," achieving a triple win where insurers profit, automotive companies reduce costs, and vehicle owners benefit through data sharing, product innovation, and service upgrades. Data-driven operations and ecological synergy will become core competencies. For the entire new energy vehicle industry, reduced insurance costs and enhanced risk control will further boost the market competitiveness of new energy vehicles, driving high-quality industrial development.

Layout 丨 Yang Shuo

Image Sources: Qianku.com, Soochow Securities

-

![]()

Shenzhen’s Longgang District Unveils New Rules for Autonomous Vehicles: Initial Deployment of 30 Vehicles, 5% Inspection Rate, and Nationwide Cross-Regional Recognition

-

![]()

Overestimated 'NIO, Xpeng, and Li Auto': Underestimated 'BYD, Geely, and Chery'

-

Are Shovel Buyers Running Low on Cash? Has the Storage Market Hit Its Peak?

-

![]()

2026 Comprehensive Solution Analysis: Optimizing Large-Scale Surveillance Storage

-

![]()

Emerging Leaders Surge Ahead, While Others Grapple with Challenges|Mid-Year Review ①

-

![]()

BYD Executive Sheds Light on Electric Vehicle Wading Prowess: Theoretical Edge Over Fuel Cars, Yet Battery Seal Integrity Is Key

-

![]()

Zhipu Stages a 'Deep V' Turnaround on Lock-up Expiry Day: Can the 'Pioneer Large Model Unicorn' Maintain Its Edge?

-

![]()

Switch Transition from Copper to Optical: From 500 Wafers to a $10 Billion Market