Can China Tourism Group Duty Free Corporation Soar Amidst Hainan’s Customs Transition?

04/01 2026

04/01 2026

653

653

On the evening of March 30, CTG unveiled its 2025 annual report. With performance estimates already disclosed, no major surprises were anticipated (Bloomberg's projections were outdated). Dolphin Research delves into the results from two angles: ① the latest quarterly performance trends; ② detailed data revealed in the semi-annual/annual reports, as outlined below:

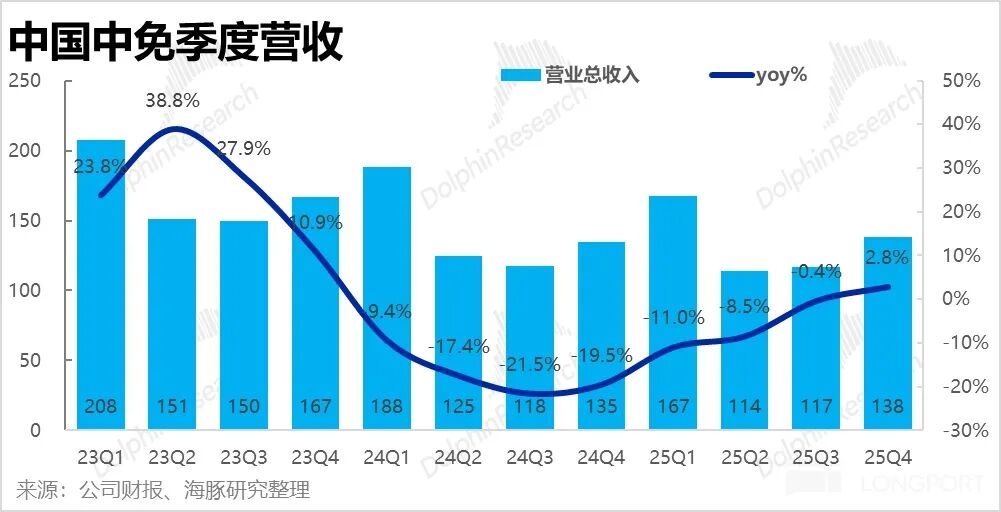

1. Revenue Growth: CTG's total revenue slightly surpassed RMB 13.8 billion, marking a 3% year-on-year increase and the first positive growth since 2024. This signals a positive performance shift, fueled by Hainan's customs transition and policy incentives.

Offshore duty-free sales in Hainan jumped 19% year-on-year in Q4, also turning positive for the first time since 2024. However, this recovery was mainly driven by higher per-capita spending due to expanded duty-free categories, while passenger traffic growth remained modest.

Given that the customs transition was implemented in mid-to-late December, its limited impact on Q4 was expected. The focus now shifts to whether passenger traffic will rebound in subsequent quarters.

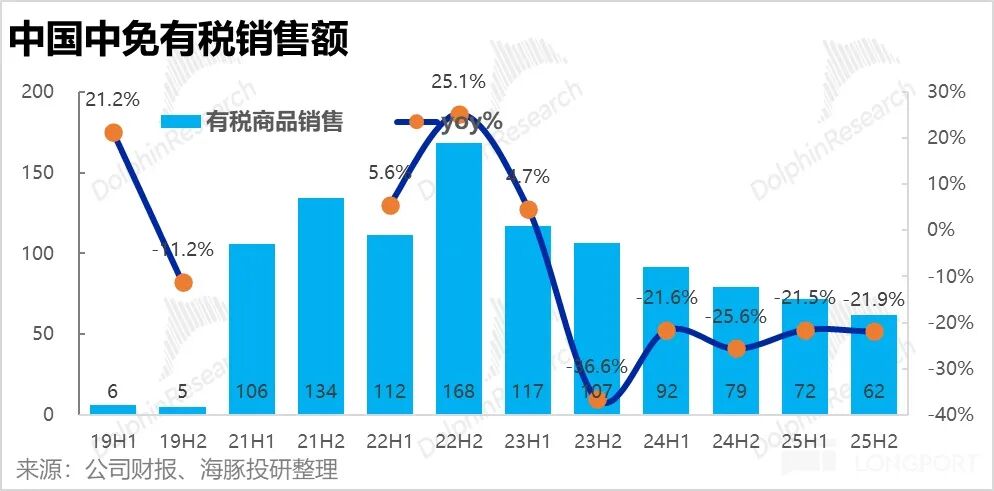

2. Revenue Breakdown: Taxable goods revenue fell by approximately 22% year-on-year in H2 2025, showing little improvement from H1. The gradual phase-out of transitional taxable businesses during the pandemic continued to weigh on performance.

In contrast, duty-free sales growth turned positive at around 11% in H2 2025, indicating a clear recovery trend.

Notably, Hainan's total sales revenue declined only slightly (~1%) year-on-year in 2025, while Shanghai's revenue (primarily from airport channels) plummeted by 25%. This underscores Hainan's recovery under policy support, contrasting with weakness in other channels.

3. Gross Profit: CTG achieved RMB 4.6 billion in gross profit in Q4, with the gross margin rising from 31.8% in Q3 to 33.4%, a significant improvement from 28.5% year-on-year.

The margin expansion was driven by: a) a lower proportion of low-margin taxable sales, b) a notable increase in taxable sales margins, and c) stable duty-free sales margins.

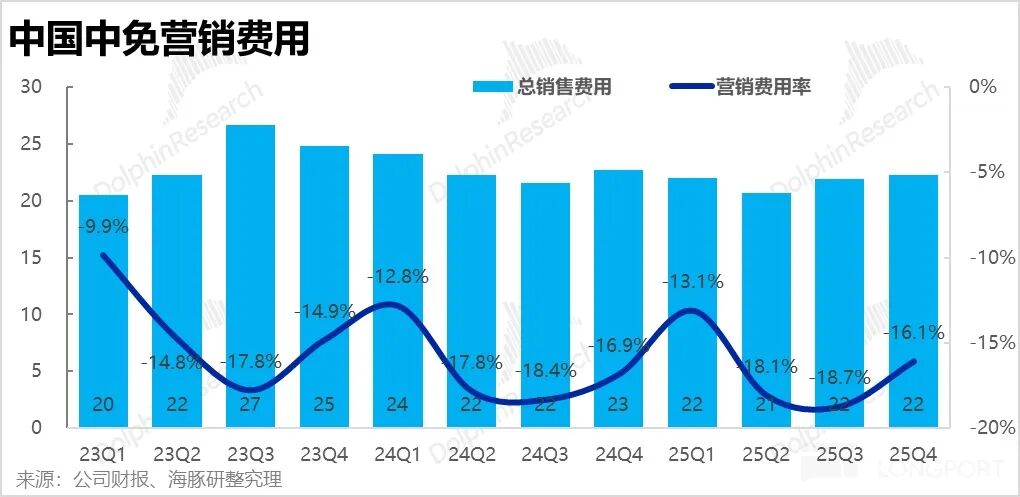

4. Selling Expenses: Selling expenses reached RMB 2.23 billion in Q4, down 1.8% year-on-year. Despite minimal change, the expense ratio narrowed by approximately 0.8 percentage points due to higher revenue scale.

The combined effect of margin improvement and reduced marketing expenses lifted the gross-to-sales spread by approximately 3.6 percentage points year-on-year, driving substantial profit growth.

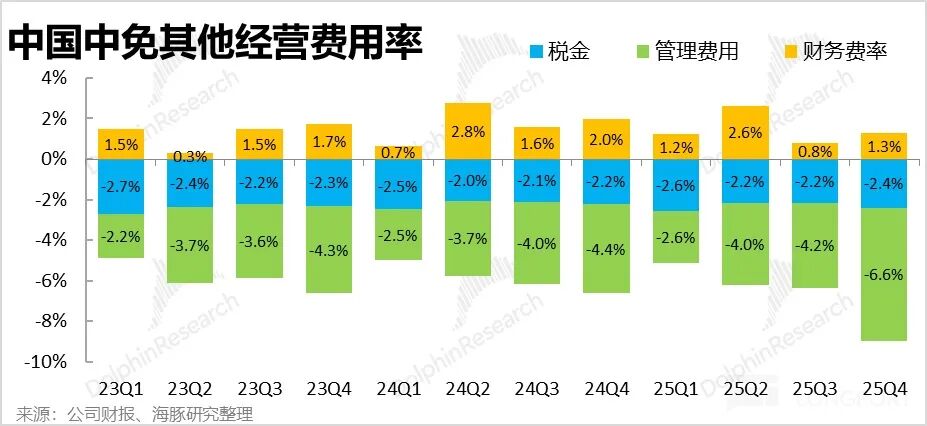

5. Other Expenses: Non-marketing expenses dampened profit release. Tax payments rose 0.2 percentage points as a share of revenue due to higher duty-free sales. Net profit from financial contributions also declined slightly year-on-year.

Administrative expenses surged from RMB 590 million last year to RMB 910 million, primarily due to a one-time goodwill impairment of a subsidiary this quarter. Excluding this, administrative expenses remained stable year-on-year.

6. Profit Improvement: Despite drags from other expenses, profit growth remained significant due to stronger margin and expense improvements. Operating margin reached 5.9%, up 0.5 percentage points year-on-year (8% excluding the one-time administrative expense impact), with operating profit reaching RMB 820 million, up 14% year-on-year.

Key Profit Metric: Net profit after non-recurring items soared 95% year-on-year to RMB 510 million (also due to a low base last year). With operating leverage, profit improvement was pronounced.

7. Dividends: The company declared an annual dividend of RMB 0.45 per share, totaling approximately RMB 935 million. Combined with the approximately RMB 490 million interim dividend announced in Q3, total 2025 dividends accounted for approximately 1.2% of the company's current market value.

While the dividend yield is low (due to high valuation multiples), it represents 40% of annual net profit—not overly generous but respectable.

Dolphin Research's View:

This quarter largely continued the recovery trend initiated in Q3, with strengthening momentum. On one hand, revenue growth halted declines, reversing prior operating deleveraging and diseconomies of scale. On the other hand, profits in Q4 2024 and early 2025 were at historic lows, making the year-on-year and quarter-on-quarter profit jumps more pronounced against this extremely low base.

The primary driver of this positive trend is the impact of "Hainan's customs transition," mentioned last quarter, which manifests in two ways:

1) Policy Upgrades Ahead of Transition: In mid-October, ahead of the transition, the government upgraded offshore duty-free shopping policies, including:

a) Expanding duty-free categories from 45 to 47, adding pet supplies, portable instruments, micro-drones, and small appliances.

b) Broadening eligibility to include departing tourists and allowing unlimited duty-free purchases for Hainan residents with off-island records in a natural year.

c) Allowing select domestic goods (e.g., apparel, footwear, ceramics, scarves, coffee, tea) in duty-free stores, with VAT/consumption tax exemptions (previously limited to imported goods).

2) Post-Transition Boost: Since Hainan's customs transition on December 18, 2025, overseas travelers have gained significantly easier access to Hainan, theoretically boosting passenger traffic and potential duty-free shoppers.

In the medium-to-long term, Hainan may leverage its free-port status to develop stronger re-export trade, manufacturing, and supporting services, attracting high-quality enterprises and migrants, and lifting overall consumption.

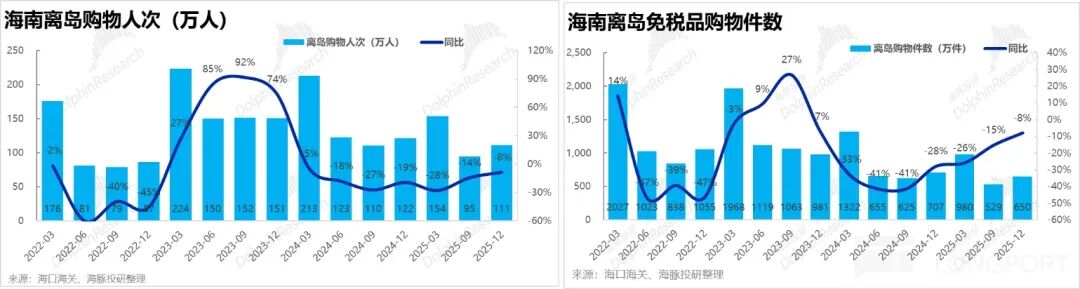

Recent offshore duty-free sales data suggest Q4 recovery was driven more by October's policy easing than December's customs transition. Off-island shopper numbers remained negative (-8% year-on-year) in Q4, while per-capita spending surged nearly 30%, indicating limited passenger traffic growth and stronger benefits from expanded duty-free categories.

However, the transition's late-December start limited its Q4 impact. Data from January-February 2026 showed off-island shopper numbers turning positive (21% and 13% year-on-year), signaling that policy easing and the transition are now boosting traffic. Sales growth has shifted from nearly price-dependent to healthier volume-and-price-driven expansion.

CTG also faces challenges. Shanghai Airport's recent duty-free bid awarded CTG only Pudong T2 and Hongqiao T1&T2 rights, losing Pudong T1. Additionally, duty-free operations at Pudong T2 and Hongqiao T1&T2 are managed by a CTG-Shanghai Airport joint venture (51% CTG, 49% Shanghai Airport), reducing CTG's profit share compared to full ownership and effectively raising airport commissions.

This aligns with the financial report's trend of continued sharp declines in Shanghai channel revenue, indicating pressure in other channels despite offshore duty-free recovery.

A detailed value analysis is published in the same-titled article under the "Insights-Deep Dive" section of the Longbridge App.

Detailed Review:

I. Revenue Stabilizes and Rebounds Amid Transition Benefits

In Q4 2025, CTG's total revenue slightly exceeded RMB 13.8 billion, up 3% year-on-year, marking the first positive growth since 2024. Driven by Hainan's customs transition and offshore duty-free policy stimulus, performance is trending upward.

Hainan's offshore duty-free sales rose 19% year-on-year in Q4, turning positive for the first time since 2024, showing clear recovery signs.

However, recovery was driven primarily by higher per-capita spending (+~30% for both average spending and unit price) due to expanded duty-free categories, while passenger traffic recovery remained modest (shopper numbers fell 8% year-on-year, though at a slower pace).

Given the transition's mid-to-late December implementation, its limited Q4 impact was unsurprising. Whether recovery accelerates in Q1 2026 bears watching.

II. Duty-Free Outperforms Taxable; Offshore Outperforms Airport

By revenue type (semi-annual disclosure), taxable goods revenue fell ~22% year-on-year in H2 2025, matching H1's decline. The gradual phase-out of transitional taxable businesses during the pandemic continued to drag on overall sales.

Meanwhile, duty-free sales growth turned positive at ~11% in H2 2025, aligning with ~9% growth in Hainan's offshore duty-free sales, indicating recovery in the core business.

Notably, Hainan's total sales revenue (offshore duty-free + taxable, ~54% of total) declined only slightly (~1%) year-on-year in 2025, while Shanghai's revenue (primarily airport channels, 23% of total) plummeted 25%. This highlights Hainan's recovery under policy support, contrasting with weakness in other channels.

III. Margin Recovery Driven More by Taxable Business

CTG achieved RMB 4.6 billion in gross profit in Q4, with the gross margin rising from 31.8% in Q3 to 33.4%, a significant improvement from 28.5% year-on-year.

Breaking down margins by revenue type, the key drivers were: a) a lower proportion of low-margin taxable sales, b) a notable increase in taxable sales margins, and c) stable duty-free sales margins in H2 2025 versus H1.

This suggests the transition has yet to significantly boost duty-free sales margins. However, margins still rose 1.4 percentage points year-on-year due to the low base last year.

IV. Modest Decline in Marketing Spending; Scale Effects Significant

Selling expenses reached RMB 2.23 billion in Q4, down 1.8% year-on-year. While CTG's marketing spending remains relatively rigid, the expense ratio narrowed by approximately 0.8 percentage points due to higher revenue scale.

As the second-busiest season after Q1's Spring Festival, Q4's marketing expense ratio passively contracted to 16.9%, down 1.5 percentage points from Q3.

The combined effect of margin improvement and reduced marketing expenses lifted the gross-to-sales spread to RMB 2.4 billion, surging ~50% quarter-on-quarter and year-on-year. The spread ratio improved by approximately 3.6 percentage points year-on-year, driving substantial profit growth.

V. Operating Leverage Drives Profit Growth

However, other expenses dragged on profit release in Q4. Tax payments rose 0.2 percentage points as a share of revenue due to higher duty-free sales. Net profit from financial contributions (interest income - interest expense) also declined slightly year-on-year.

Administrative expenses surged from RMB 590 million last year to RMB 910 million, likely due to a one-time goodwill impairment of a subsidiary this quarter (estimated at ~RMB 300 million). Excluding this, administrative expenses remained stable year-on-year.

Overall, despite the drag from other expenses, the improvement in gross profit margin was more significant, leading to an operating profit margin of 5.9% for China Duty Free Group (CDFG) this quarter, a year-on-year increase of 0.5 percentage points (excluding the one-time impact of administrative expenses, the operating profit margin reached 8%), with an ultimate operating profit of RMB 820 million, a 14% year-on-year increase.

The primary profit metric of concern to the market, net profit attributable to shareholders after non-recurring items, was RMB 510 million, surging by 95% year-on-year. The combination of a low base last year and the further release of operating leverage this quarter resulted in a notably significant improvement in profits.

produce, copy, reproduce, duplicate, forward, or create any form of derivative copies in any manner, and/or (ii) directly or indirectly redistribute or transfer the report to any unauthorized parties. Dolphin Research reserves all relevant rights.</p></div>

<!-- <p><span style=)

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models