Market Value Surpasses 400 Billion Yuan! Intelligent Agents Soar by 248%! Is Zhipu AI Set to Become China's Anthropic?

04/07 2026

04/07 2026

586

586

After an 83% API price hike, Zhipu AI's token sales exploded—a counterintuitive data point from its first post-IPO earnings report. Over the past 12 months, MaaS platform ARR surged 60x to 1.7 billion yuan, with paying developers exceeding 242,000, seemingly validating the narrative that "upper bounds of intelligence determine pricing power."

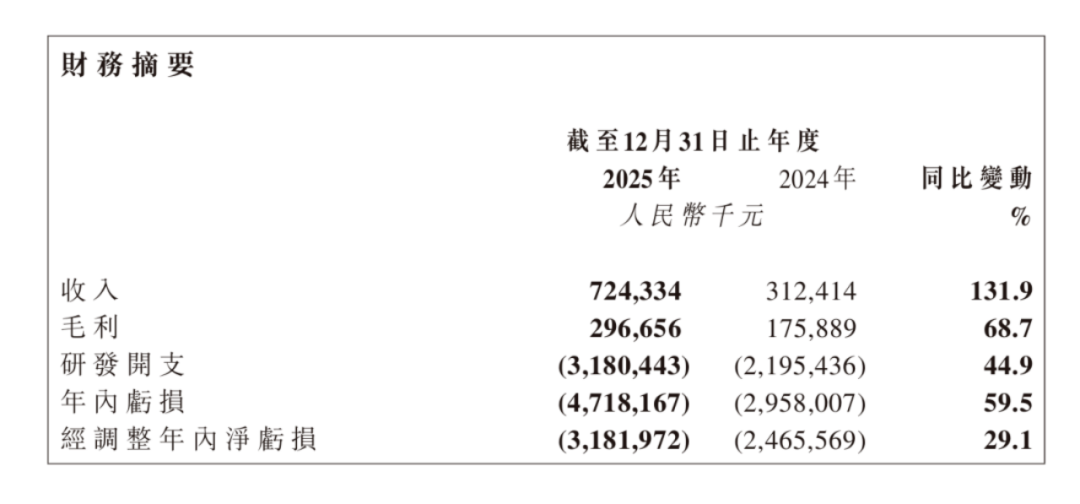

But magical realism soon followed: 2025 revenue hit 724 million yuan (+131.9% YoY), yet net losses ballooned to 4.718 billion yuan (+59.5% YoY). R&D spending reached 3.18 billion yuan, accounting for 439% of revenue, underpinning a 400 billion HKD market cap and 500x price-to-sales ratio.

Just two days after the earnings release, shares of Zhipu—which surged 33% on April 1 to hit a record 410 billion HKD market cap—plummeted 14.86% to close at 779 HKD on April 3, erasing over 60 billion HKD in a single day.

(Image Source: East Money)

From "volume and price surge" to "valuation collapse," as "token consumption scale" replaces "market dream rates" as the new capital anchor, has Zhipu found the inflection point for AGI commercialization, or is it undergoing a phase of "faith overdraft" reckoning?

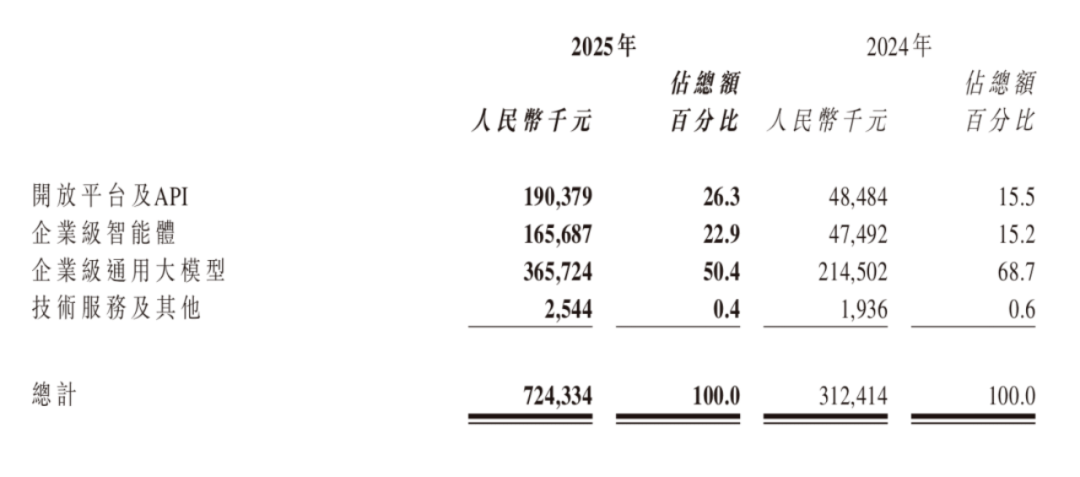

Revenue Structure Shift: From "Project-Based" to "Token Economy"

The quality of Zhipu's revenue growth must be examined through its shifting revenue mix. In 2025, localized deployment revenue reached 534 million yuan (73.7% of total, +102.3% YoY), while cloud deployment revenue hit 190 million yuan (26.3%, +292.6% YoY). On the surface, localized deployment remains the foundation, but explosive cloud growth reveals deeper business model transformation.

(Image Source: Company Financial Reports)

This transition came with painful gross margin declines. Overall gross margin fell from 56.3% to 41.0% in 2025, primarily due to rising shares of low-margin cloud business (though its margin improved from 3.3% to 18.9%, still far below localized deployment's 48.8%). This "volume-for-price" strategy essentially tests Zhipu's proposed business formula: AGI commercial value = Upper bounds of intelligence × Token consumption scale.

Data validates this logic's initial success: In February 2026, Zhipu proactively raised API prices by 83% while MaaS platform ARR surged 60x to 1.7 billion yuan over 12 months, with paying developers exceeding 242,000. This "volume and price surge" is rare amid domestic large model price wars, suggesting GLM-5's technical capabilities (ranked first alongside OpenAI and Anthropic on Code Arena) indeed confer pricing power.

However, localized deployment gross margins plunged from 66.0% to 48.8%, hinting at rising delivery costs for B-end project-based business. As a "national team" player serving governments, financial institutions, and state-owned enterprises, Zhipu faces tensions between large customized demands and standardized products. In H1 2025, its top five clients still accounted for 45.5% of revenue, with customer concentration risks not fully resolved.

(Image Source: Company Financial Reports)

Loss Black Hole: The "Arms Race" Logic of R&D Investment

Zhipu's widening losses stem not from operational inefficiency but strategic "upfront investment." 2025 R&D spending reached 3.18 billion yuan (+44.9% YoY), with employee costs (including share-based payments) hitting 1.363 billion yuan. The 1,094 R&D personnel averaged over 1.2 million yuan in compensation.

This intensity contrasts starkly with overseas peers: OpenAI's R&D-to-revenue ratio is about 1.56:1, while Zhipu's stands at 4.4:1. This suggests Zhipu remains in an early stage of trading technical investment for market positioning, with a profitability cycle significantly longer than overseas leaders that have found scaling paths.

More alarmingly, general and administrative expenses surged 278.3% YoY, linked to organizational expansion pre- and post-IPO. Post-HKEX listing, Zhipu needs stronger compliance, risk control, and investor relations systems, with rising management costs challenging its "cost reduction and efficiency improvement" efforts.

Cash flow-wise, Zhipu held 2.259 billion yuan in cash and equivalents by end-2025, plus ~5 billion HKD (~4.516 billion yuan) from January 2026 IPO proceeds. Its cash reserves can support ~1.5–2 years of current R&D intensity, making 2026–2027 a critical window: either token economy scaling reduces costs, or it faces new financing or valuation corrections.

The Tension Between 400 Billion Market Cap and 700 Million Revenue

Capital market sentiment diverges sharply from fundamentals. By early April, Zhipu's market cap exceeded 400 billion HKD, nearly 8x its IPO price. At 724 million yuan in 2025 revenue, its price-to-sales (P/S) ratio exceeds 500x, far above traditional SaaS firms and most AI unicorns.

This valuation logic is shifting from "China's OpenAI" to "China's Anthropic." Anthropic's ARR soared from $1 billion at end-2024 to ~$19 billion by March 2026, with ~80% from enterprise API calls. Zhipu mirrors this path, with MaaS platform ARR reaching 1.7 billion yuan and API demand remaining strong post-price hikes, seemingly validating the "upper bounds of intelligence determine pricing power" narrative.

But risks lie in customer structure fragility. Zhipu discloses that 9 of China's top 10 internet firms deeply integrate GLM models, yet these giants are also major self-developed model players. CEO Zhang Peng responds that "big firms will self-develop but may lack competitiveness in all scenarios," though maintaining this technological edge will determine whether current large-scale usage faces diversion.

Additionally, financial instrument revaluations of 937 million yuan reflect fair value adjustments of convertible preferred shares from multiple funding rounds, which will continue affecting profit statement stability.

Future Watch: Agent Commercialization and "Sovereign AI" Globalization

Two bright spots in the earnings warrant long-term tracking:

First, the explosion of Agent (intelligent agent) business. Enterprise agent revenue jumped from 47.49 million to 166 million yuan (+248.8% YoY), with Claw Plan surpassing 400,000 subscribers in 20 days. This marks Zhipu's leap from "model provider" to "application ecosystem builder." If Agents become enterprise workflow standards, token consumption could grow exponentially.

Second, the "sovereign AI" globalization model. Zhipu recently secured a $10+ million national-level sovereign large model co-construction order from a Belt and Road country and partnered with Mercedes on on-device multimodal large models. This "technological sovereignty" export model, distinct from simple API exports, could unlock new valuation potential.

Zhipu's earnings reveal the true landscape of China's large model sector: technological commercialization is accelerating, but profitability remains a marathon. Its "volume and price surge" token economy validates that technological barriers can translate into commercial pricing power, but the chasm between its 400 billion yuan market cap and 4.7 billion yuan annual loss tests capital market faith in AGI long-termism.

For investors, key 2026 validation metrics will be whether cloud deployment gross margins break 20%, MaaS platform ARR sustains 60x growth, and R&D spending ratios fall from 439% to below 200%. Against a backdrop of industry reshaping by open-source models like DeepSeek, Zhipu's "closed-source + platform" strategy ability to maintain upper bounds of intelligence will determine whether this earnings report marks AGI commercialization's prologue or the capital feast's finale.

(This article does not constitute investment advice. Market risks exist; invest cautiously.)

END

Special Disclaimer: Content sourced from public internet channels. Contact us for removal if infringing. This article absolutely does not constitute any investment advice, guidance, or commitment, and is solely for industry exchange and discussion. Market risks exist; invest cautiously!

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?