AI Server Contender AnQing Computers Rushes for IPO with Nearly 5.5 Billion Yuan in Annual Revenue, Yet Faces 'Chip' Challenges

04/15 2026

04/15 2026

621

621

Produced by | Frontline of Entrepreneurship

Art Editor | Xing Jing

Reviewed by | Song Wen

As AI computing power becomes the 'water, electricity, and coal' of the digital age, a global battle for dominance in the AI server market is underway. On this golden track, NVIDIA dominates the global market share with its GPU advantage, while domestic leaders such as Inspur Information, Huawei, New H3C, and Sugon are also accelerating their market grab.

Amid the intense competition in the AI server market, on April 2, 2026, AnQing Computer Information Co., Ltd. (hereinafter referred to as AnQing Computers), a Tianjin-based company specializing in AI computing equipment, submitted its application to list on the main board of the Hong Kong Stock Exchange, with CICC serving as the sole sponsor.

Based on 2024 revenue, AnQing Computers is China's sixth-largest AI computing equipment solution provider and the largest independent company among them. In 2025, it achieved revenue of approximately 5.5 billion yuan, a surge of over 99% year-on-year.

However, a deeper analysis reveals a more complex picture—declining gross margins, a lack of 'self-sufficiency,' and heavy reliance on external supply chains. These challenges add uncertainty to its IPO process and future development.

1. Sixth-Place AI Server Player with Post-Investment Valuation Exceeding 3.5 Billion Yuan

Yu Yueyuan, the 46-year-old founder, chairman, and president of AnQing Computers, graduated from Beijing Jiaotong University in 2013 with a bachelor's degree in logistics management and earned an Executive MBA from Tsinghua University in 2021.

Before founding AnQing Computers, Yu worked for nearly 13 years at Beijing Tianqin Yida Technology Co., Ltd., a company specializing in servers and system integration, serving as its general manager.

He established AnQing Computers in 2017, focusing on the development, design, production, and sales of AI computing equipment.

From 2022 to 2025, AnQing Computers was selected as a national-level 'Little Giant' enterprise in specialized and sophisticated manufacturing, a Tianjin manufacturing single-champion enterprise, and was rated among Tianjin's first batch of 'Cheetah Enterprises.'

(Image / Prospectus)

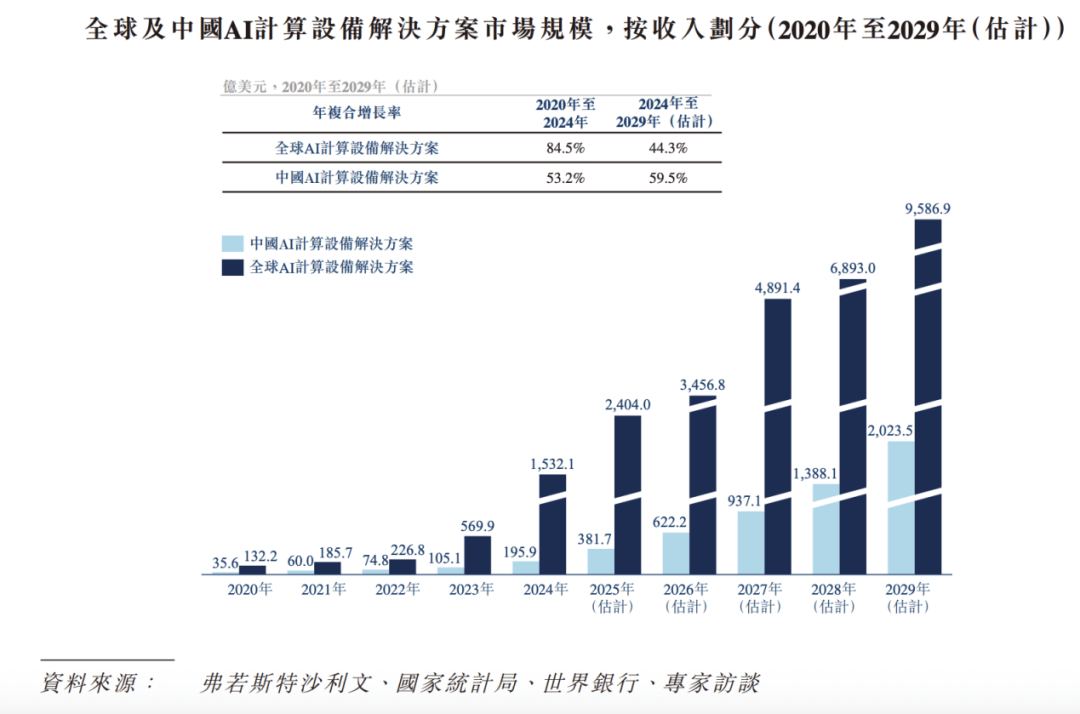

AnQing Computers operates in the rapidly growing AI computing equipment industry: Data from Frost & Sullivan, the National Bureau of Statistics, and the World Bank show that China's AI computing equipment solution market size grew from $3.6 billion in 2020 to $19.6 billion in 2024, with a compound annual growth rate (CAGR) of 53.2%. It is expected to reach $202.4 billion by 2029, with an even higher CAGR of 59.5% from 2024 to 2029.

However, AnQing Computers finds itself in a somewhat awkward position in this market.

(Image / Prospectus)

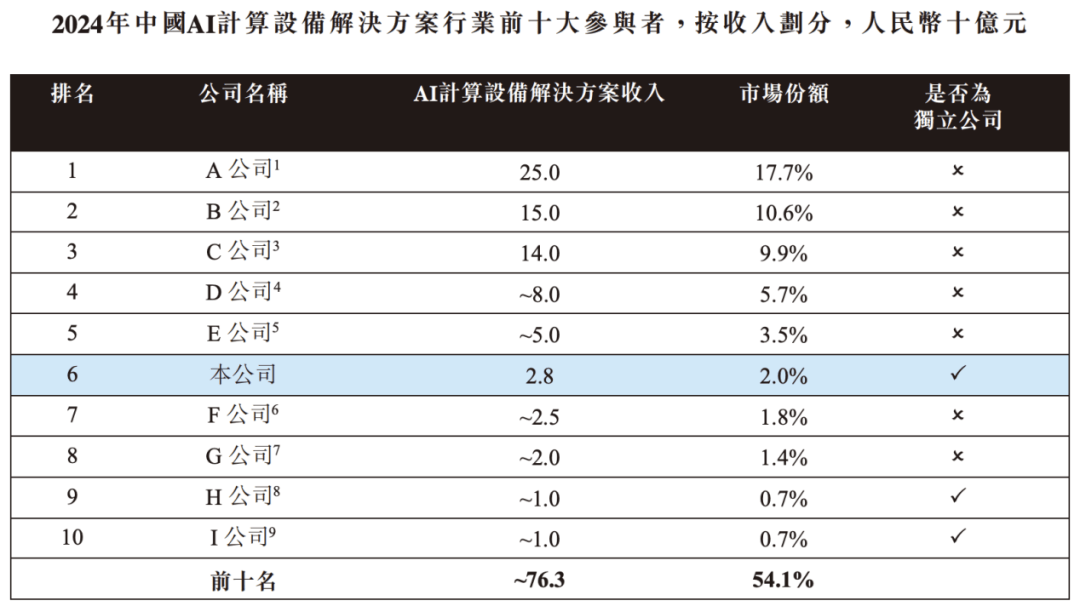

According to Frost & Sullivan, based on 2024 revenue, AnQing Computers ranks sixth among China's AI computing equipment solution providers with a 2% market share.

The top five companies, including Inspur Information and Supercomputing Convergence, account for nearly half of the market (47.4% combined). 'Company F,' which ranks just behind AnQing Computers, holds a 1.8% market share, indicating that AnQing Computers is squeezed between industry giants.

Nevertheless, AnQing Computers has attracted significant investor interest. From 2020 to 2025, the company secured five rounds of financing from investors including SenseTime, Hanhu Venture Capital, Tiandi Chouqin, Qingke Hejia, and Wanfang Funds.

After completing its latest funding round in December 2025, AnQing Computers' valuation reached approximately 3.58 billion yuan.

Before the IPO, founder Yu Yueyuan controls 67.37% of the company's equity through Shixun Technology and Jinggu Information, making him the absolute controlling shareholder. Company director and vice president Yang Lingyun holds an 11.60% stake through Mingji Information. Jinggu Information and Mingji Information are employee stock ownership platforms for core team incentives.

Additionally, SenseTime holds a 3.83% stake, Hanhu Venture Capital holds 3.99%, Tiandi Chouqin holds 3.6%, and Wanfang Zhenyi holds 1.4%.

In 2023, AnQing Computers also received investments from Beijing-Tianjin-Hebei Investment and Xicheng Zhiyuan. However, in April 2025, the company fully repurchased shares from both institutions and reduced its registered capital from approximately 163 million yuan to about 148 million yuan.

When asked whether the exit of Beijing-Tianjin-Hebei Investment and Xicheng Zhiyuan was related to the company's shift from A-shares to Hong Kong shares, Frontline of Entrepreneurship did not receive a response from AnQing Computers as of press time.

During the same period, shares held by three institutional shareholders—Jinzheng Kechuang, Liangyi Zhongfu, and Qigang Chengshi—were also repurchased to varying degrees, reducing their stakes.

Notably, AnQing Computers had signed agreements with some investors containing redemption rights, anti-dilution, and liquidation preference clauses. As of the prospectus filing date, all special rights clauses had been terminated but remained triggerable. If the company withdraws its IPO, is rejected, or fails to complete a qualified listing by June 30, 2027, shareholders' special rights will be reinstated.

2. Revenue Nearly Doubles in 2025, But Gross Margins Continue to Decline

At first glance, AnQing Computers' growth trajectory appears impressive.

The prospectus shows that AnQing Computers' revenue surged from 2.206 billion yuan in 2023 to 2.76 billion yuan in 2024 and further to 5.5 billion yuan in 2025, representing a 99.28% year-on-year increase in 2025.

(Image / Prospectus)

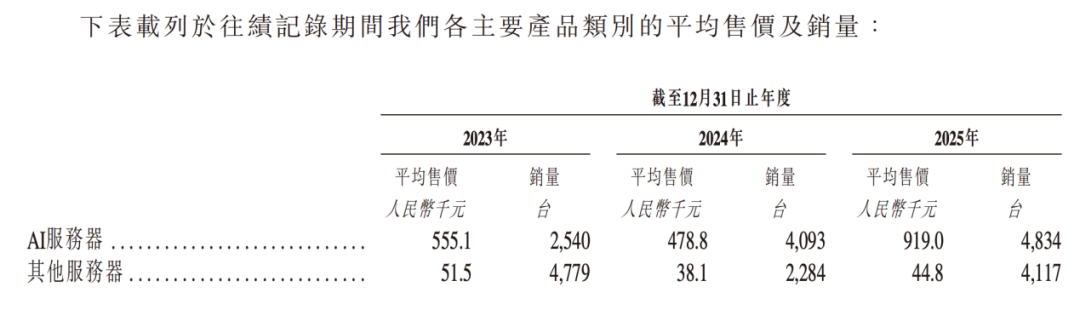

In 2025, a year of explosive AI computing demand, AnQing Computers clearly benefited from the industry boom—selling 8,951 servers, including 4,834 AI servers with an average price of 919,000 yuan, far higher than the 555,100 yuan average in 2023 and 478,800 yuan in 2024.

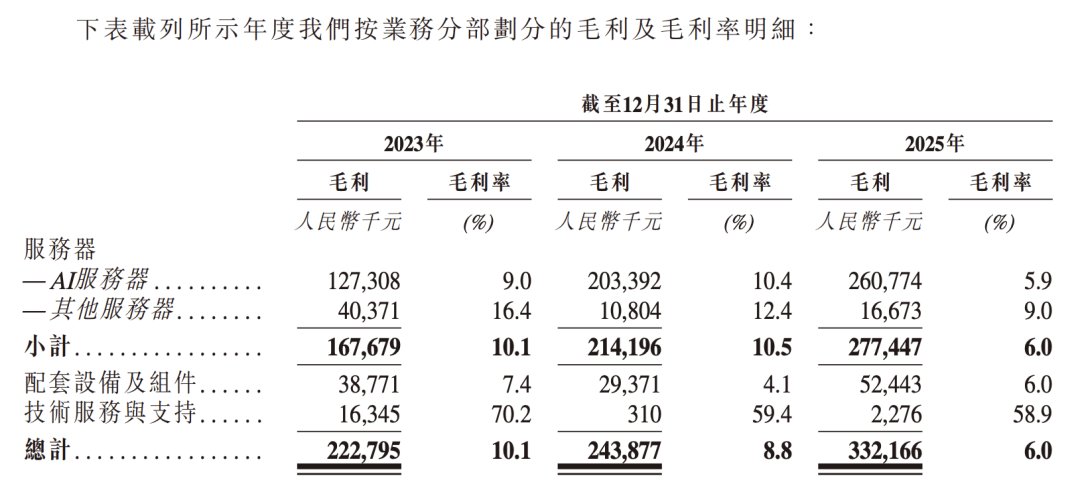

However, behind the revenue surge lies a persistent decline in gross margins.

From 2023 to 2025, AnQing Computers' overall gross margins were 10.1%, 8.8%, and 6.0%, respectively. The company attributed the decline to temporary and cyclical increases in raw material prices.

(Image / Prospectus)

To mitigate the impact of rising raw material costs, AnQing Computers increased procurement volumes and inventory levels during the period, leading to higher working capital requirements and negative operating cash flow.

The prospectus shows that from 2023 to 2025, AnQing Computers reported profits of 54.435 million yuan, 63.675 million yuan, and 122 million yuan, respectively. Adjusted net profits were 71.903 million yuan, 75.537 million yuan, and 140 million yuan, respectively.

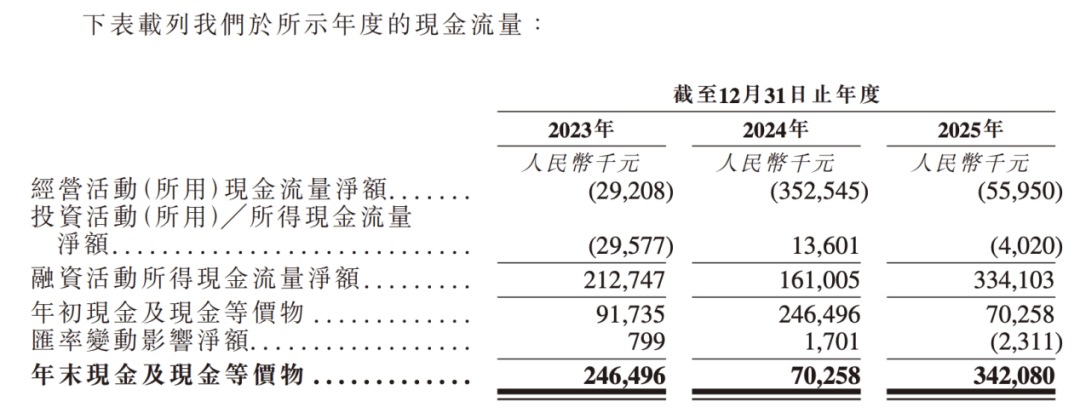

During the same period, the company's net operating cash flow was -29.208 million yuan, -353 million yuan, and -55.95 million yuan, respectively, with a cumulative net outflow of 438 million yuan over three years.

(Image / Prospectus)

Persistent negative operating cash flow means AnQing Computers relies on external financing for daily operations, R&D, and capacity expansion, exposing it to funding risks if financing is disrupted.

As of the end of 2025, AnQing Computers' total interest-bearing bank loans stood at 856 million yuan, up about 94% from 442 million yuan at the same time in 2024.

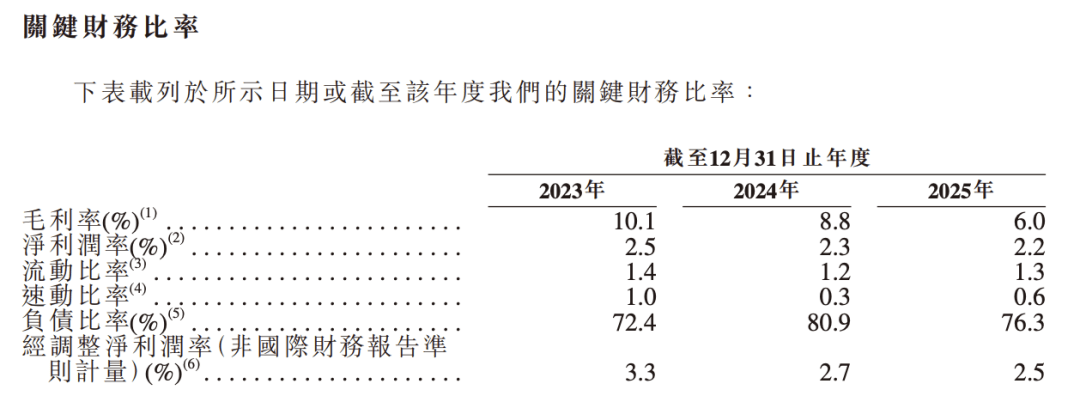

According to the prospectus, AnQing Computers' asset-liability ratio exceeded 70% from 2023 to 2025, peaking at 80.9% in 2024 before declining to 76.3% in 2025, still higher than the 2023 level.

(Image / Prospectus)

Currently, AnQing Computers faces pressure from both inventory buildup and accounts receivable.

In 2024, inventory surged by 1.136 billion yuan to 1.48 billion yuan due to large customer orders. Products were either in production or en route by year-end, but cash had not yet been recovered as customer acceptance and payment milestones were incomplete, creating a significant timing mismatch between inventory and cash inflows in 2024.

In 2025, inventory further increased to 1.593 billion yuan, tying up even more capital.

From 2023 to 2025, AnQing Computers' trade receivables and bills stood at 201 million yuan, 162 million yuan, and 587 million yuan, respectively.

Additionally, to recover customer debts, AnQing Computers filed a lawsuit against a client in March 2026, claiming approximately 245 million yuan in unpaid contract amounts and late payment penalties.

In summary, despite rapid revenue and product sales growth, AnQing Computers still faces declining gross margins, persistent negative operating cash flow, and high asset-liability ratios. Combined with significant capital tied up in inventory and receivables, these factors highlight concerns over growth quality and funding chain risks, casting doubt on the sustainability of its rapid expansion.

3. Supply Chain Vulnerabilities and Escalating Chip Control Concerns

Beyond internal financial challenges, AnQing Computers also faces external supply chain risks.

The prospectus reveals that from 2023 to 2025, procurement from AnQing Computers' top five suppliers accounted for 47.7%, 69.9%, and 63.3% of total purchases, respectively, indicating high supplier concentration. These suppliers primarily provide core components such as server platforms, CPUs, motherboards, and accelerator cards.

The heart of AI servers lies in GPU chips, whose performance directly determines server computing power, with NVIDIA dominating the global GPU market.

As one of the few partners in the Asia-Pacific region to receive NVIDIA's Elite OEM certification, AnQing Computers gains early access to NVIDIA's product roadmaps, design specifications, development materials, and test samples. This relationship enables direct product supply from NVIDIA and ongoing technical support throughout the product lifecycle.

However, just before AnQing Computers' IPO, the U.S. passed the CHIPS and Science Act, marking a significant shift in chip export controls from licensing to technology monitoring, extending oversight to the full lifecycle of chip usage.

Coinciding with AnQing Computers' prospectus filing, the U.S. Senate and House jointly proposed the Multilateral Coordination Act on Hardware Technology Controls (MATCH Act), which seeks to ban not only the sale of new equipment but also after-sales maintenance and spare parts supply for Chinese chip factories. It even mandates U.S. allies like Japan, the Netherlands, and South Korea to implement similar controls. The bill remains in the proposal stage, but its passage warrants close attention.

Although the prospectus states that AnQing Computers is 'among the first few suppliers capable of mixed computing with both domestic and non-domestic AI computing equipment,' the U.S.'s comprehensive tightening of restrictions on high-end computing power and chip manufacturing chains poses severe supply chain challenges for AI server manufacturers like AnQing Computers that rely on high-end GPUs.

AnQing Computers acknowledges in the prospectus that it faces risks related to international trade policies, trade restrictions, export control laws, and economic or trade sanctions.

Frontline of Entrepreneurship also sent inquiries to AnQing Computers regarding the extent to which its core products rely on overseas suppliers like NVIDIA and AMD, the potential impact of recent U.S. legislation on its future performance, any mitigation strategies, and when domestic chip manufacturers might achieve full substitution. No response was received as of press time.

In summary, supply chain risks centered on 'chip' issues represent one of the uncertainties in AnQing Computers' IPO journey. This challenge is not unique to AnQing but a structural issue facing China's entire AI computing power industry.

Against the backdrop of intensifying tech competition, building a secure and controllable supply chain will be a critical factor determining the future of AnQing Computers and the broader sector.

Only by maintaining steady and sustainable growth can AnQing Computers live up to expectations. Whether it can resolve its core challenges with capital support and transition from a 'sixth-place player' to a 'dark horse' in the sector remains to be seen. Frontline of Entrepreneurship will continue to monitor developments.

*Note: The featured image and unnamed images in this article are from Shetu.com, used under the VRF protocol.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?