Is the Era of Influencer Live Streaming Over? Live Streaming May No Longer Need 'Super Influencers'

04/15 2026

04/15 2026

676

676

On April 8, during the 10th-anniversary celebration of Taobao Live, Li Jiaqi took the stage to talk about his decade-long journey and, choking up, announced that he plans to take two quarters off from live streaming this year. The topic quickly trended on Weibo, sparking widespread public discussion.

This year, the live streaming industry has entered a turbulent phase. A few days ago, YouSiyi faced a major scandal, effectively wiping out half of the influencer circle, from top-tier influencers to celebrities and review bloggers, all lining up to apologize. This collective downfall of leading influencers has plunged the entire live streaming e-commerce sector into an unprecedented crisis of trust. No one expected that for a blatantly fake health product, none of these influencers, who pride themselves on having professional product selection teams, would notice.

At this point, whether Li Jiaqi is retiring from the limelight or attempting to 'depersonalize' his brand remains unclear. However, his temporary exit undoubtedly signals the inevitable decline of influencer-led live streaming. Coupled with the YouSiyi incident, more consumers are likely to become disillusioned with influencer-led live streaming, further accelerating its downturn.

Of course, more critically, a large number of brands are reducing or abandoning influencer-led live streaming, which deals a 'fatal blow.'

Has the era of influencer-led live streaming come to an end?

From its rise to prosperity, influencer-led live streaming has played a significant role, and many brands owe their popularity to top influencers with massive followings.

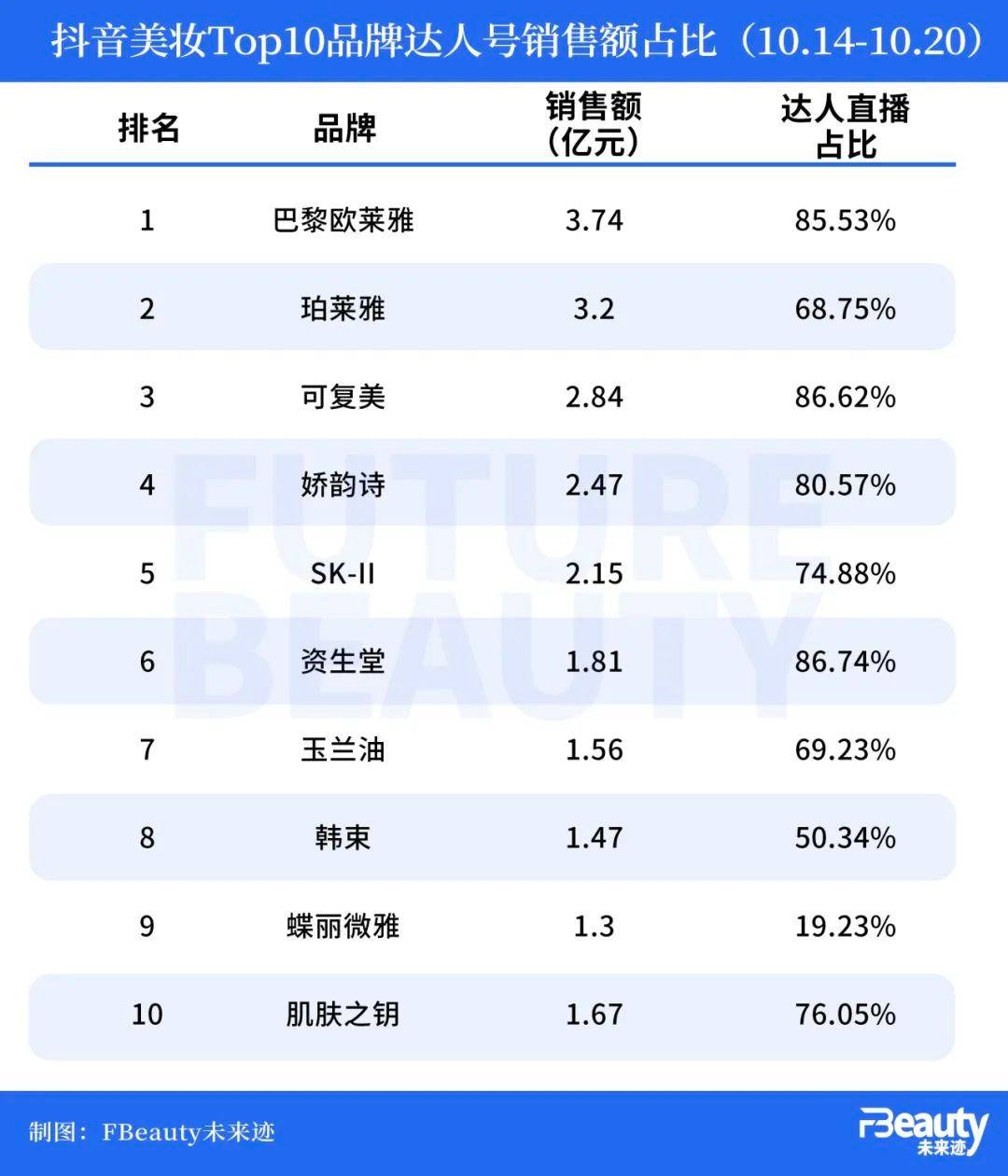

Especially in the vast beauty and skincare market, the surge in online sales over the past few years can be attributed to influencer-led live streaming. During the 2024 'Double 11' shopping festival, according to data from Chanmama, if we analyze the GMV sources of the top 10 beauty brands on Douyin over the past week (October 14-20) across four channels—'brand self-operated accounts,' 'merchant self-operated accounts,' 'influencer accounts,' and 'product cards'—nearly all brands derived over 70% of their GMV from influencer accounts.

For instance, L'Oréal Paris, ranked first on Douyin's beauty list, generated RMB 374 million in GMV in one week, with influencer-led sales accounting for over 85%. Similar patterns were observed for brands like Forget Beauty, Clarins, Shiseido, and L'Oréal, all with influencer-led sales exceeding 80%. The same trend applied on Kuaishou, where WHOO achieved RMB 1.687 billion in GMV, with Xin Youzhi alone contributing RMB 1.4 billion in sales.

However, influencer-led live streaming is now being strategically 'abandoned' by brands.

Taking beauty brands as an example, on Douyin's 'Top 20 Beauty Influencers' list for the first quarter of this year, several well-known influencers from the same period last year, such as Wei Xue, Jia Nailiang, Zhang Meng and Xiaowu, the Rainbow Couple, and Dada, were no longer in the top 20.

Behind the 'disappearance' of top influencers lies a shift in focus among beauty brands from influencer-led to self-operated live streaming. For instance, at last year's performance review meeting, Marubi Biotechnology announced adjustments to its influencer-led and self-operated live streaming strategies. Similarly, brands like Chando, Proya, and even some foreign brands that once heavily relied on top influencers to drive sales are now choosing to reduce influencer-led efforts and ramp up self-operated live streaming.

According to data from third-party platforms, in the first quarter of 2026, 85% of the top 20 beauty brands saw a decline in the proportion of sales generated through influencer promotions. For example, Proya's influencer-led sales dropped to 25.16%, while its self-operated live streaming rose to 57.26%. Marubi's influencer-led sales fell to 36.36%, with self-operated live streaming increasing to 53.27%. Additionally, brands like KanS and ZaoWuZhe saw their influencer-led sales proportions drop to single digits.

The changes are not limited to beauty brands. In March this year, rumors circulated on social media that Blue Moon had disbanded its influencer-led live streaming teams on platforms like Douyin. Over the past two years, Blue Moon had been one of the biggest spenders on influencer-led live streaming, partnering with nearly all top influencers on Douyin and routinely achieving sales exceeding RMB 100 million per session.

While we cannot confirm the veracity of these rumors, it is clear that Blue Moon has adjusted its channel strategy this year. In late March, the company signed a strategic cooperation agreement with JD Supermarket, aiming to achieve RMB 5 billion in sales on JD within three years. This move to a comprehensive e-commerce platform directly reveals the brand's intention to reduce its over-reliance on influencer-led live streaming and correct its past strategy of heavily betting on top influencers and traffic.

In fact, early last year, Li Liang, Vice President of Douyin Group, stated that for Douyin E-commerce, merchant-operated live streaming is the mainstream, with the number of small and medium-sized merchants launching such streams far exceeding those relying on influencer-led live streaming. While top influencers once seemed to prop up the entire live streaming e-commerce sector, it is now evident that influencer-led live streaming is losing its dominance.

A 'Conspiracy' Between Brands and Platforms

Why are more and more brands choosing to reduce or abandon influencer-led promotions? Simply put, because it is no longer profitable for them.

A founder of a beauty brand noted, 'In 2024, the commission rate for influencer live streaming might have been around 40%, but by 2025, it had risen to nearly 60%.' Many beauty brands once relied heavily on influencers to drive sales, but now, with marketing investments increasing and marginal returns shrinking, the rising commission rates further squeeze brand profit margins, trapping them in a cycle of increased revenue without increased profitability.

The same applies to other categories, such as health supplements. The YouSiyi scandal exposed just the tip of the iceberg regarding the exorbitant profits in the health supplement industry, where influencer commissions are significantly higher than for other product categories. An e-commerce industry insider revealed that if a health supplement brand relies solely on an influencer's Comes with built-in traffic (organic traffic) without purchasing additional traffic, the influencer can earn a commission of 40%-50%.

Excessive commission rates, persistently high return rates, and the increased risks associated with frequent scandals involving top influencers are all causing brands to become more cautious about relying on influencer-led live streaming.

But this may only be the surface. The decline and eventual end of influencer-led live streaming are, more fundamentally, a shared choice by brands and platforms. The rise and growth of super influencers have significantly weakened the bargaining power of brands and platforms, tilting the balance of interests. Both brands and platforms now seek to rewrite the rules. Additionally, as platforms, especially content platforms like Douyin and Kuaishou, shift their focus in live streaming e-commerce from stimulating impulsive purchases to fostering user shopping habits, and as brands that have successfully scaled up urgently need to retain users and tell their brand stories, the strategic value of influencer-led live streaming has greatly diminished.

In fact, data shows that the sales growth driven by influencer-led live streaming has slowed. Taking Proya as an example, from 2021 to the first half of 2024, its revenue growth remained consistently high at 36%-38%, but in 2025, growth dropped sharply to 7.21%. Moreover, in 2024, Proya's revenue growth was 8 percentage points lower than its sales expense growth.

Relying on influencers to sell products is essentially a crude traffic-driven approach. Some brands and products lack clear positioning yet proceed with OEM production, spend heavily to partner with top influencers, and rely on influencer-led live streaming to guide consumption and open up the market. However, once marketing investments are reduced, product sales plummet. Even established brands find themselves 'trapped' in a cycle of sustained high-cost investments, forced to accept the profit margins being eroded by influencer-led live streaming.

This dilemma highlights that the driving force behind consumer purchases comes not from the products or brands themselves but rather from the influence of the influencers. Therefore, for a brand to truly capture consumer mindshare and reshape its brand image, it must first abandon the path of relying solely on influencer-led live streaming for sales growth.

This aligns with the platforms' intentions. Douyin and Kuaishou hope to cultivate daily shopping habits among consumers on their platforms, rather than having purchases driven solely by influencer recommendations.

Domestic Brands Cannot Rely Solely on Influencer-Led Live Streaming for True Success

The rise of content e-commerce, represented by live streaming e-commerce, presents an opportunity that domestic brands cannot afford to miss. Many once-forgotten domestic brands have leveraged live streaming e-commerce to regain popularity and gain traffic.

In the beauty category, live streaming e-commerce has even directly enabled domestic brands to overtake international beauty giants.

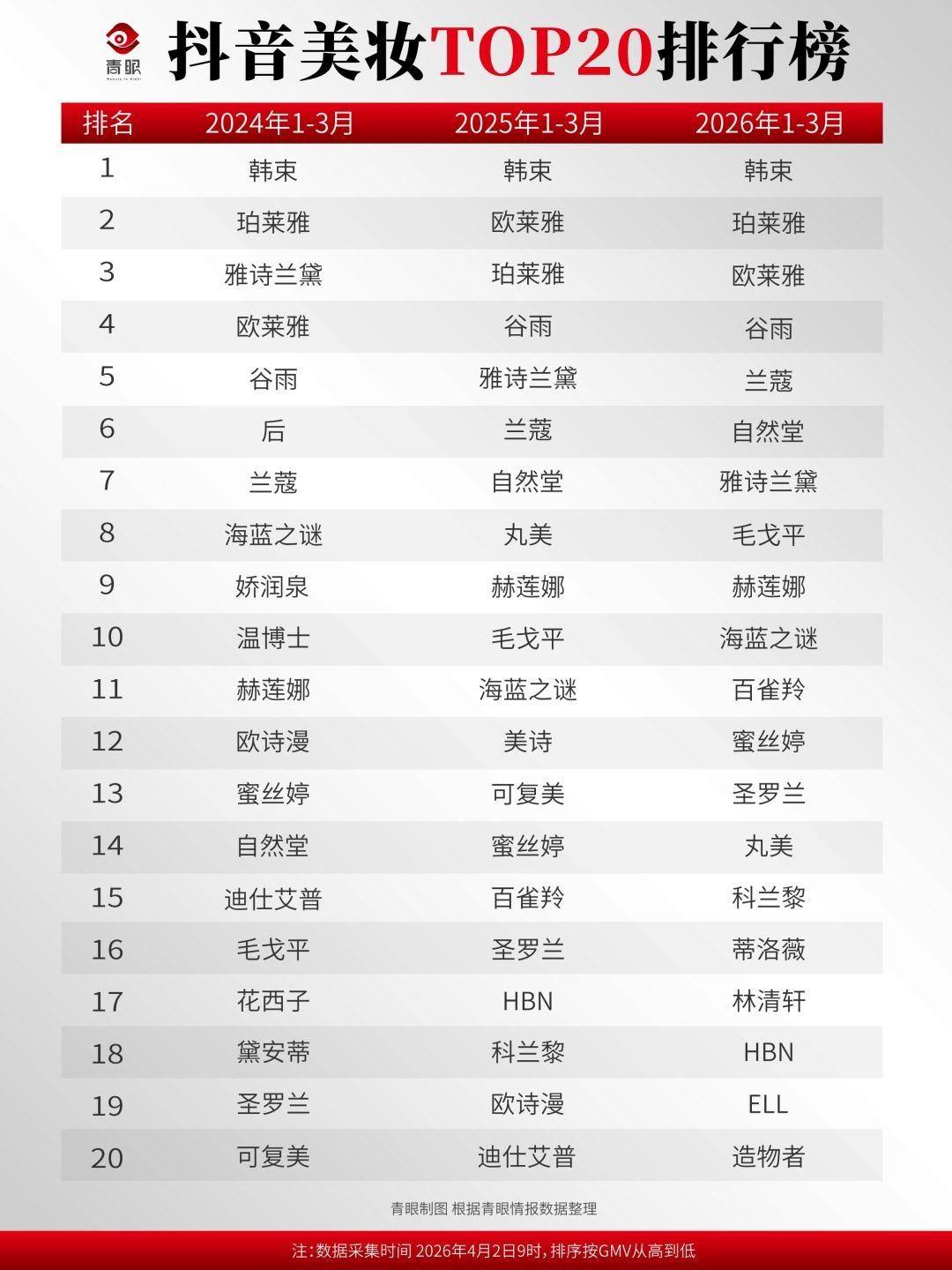

According to the Douyin Beauty Top 20 list for March 2026, the dominance of domestic brands has become increasingly clear. Not only do they outnumber foreign brands on the list, but the top four are all domestic brands—a first in the March Douyin Beauty list over the past three years. Additionally, based on the list for the first quarter of 2026 (January-March) compiled by Qingyan, 13 of the 20 brands were domestic, accounting for 65%. These brands have all experienced rapid growth on Douyin over the past five years.

During the era of shelf e-commerce, the beauty market was largely dominated by foreign brands. However, with the advent of live streaming e-commerce, domestic beauty brands have found an opportunity to turn the tide, largely thanks to live streaming e-commerce and, in particular, the influence of a few super influencers. Nevertheless, we must also recognize that this 'turning of the tide' primarily reflects a narrowing of the scale gap rather than a surpassing of brand influence.

Simply put, few domestic beauty brands can truly be considered 'big brands' because, to date, no Chinese beauty company has achieved true globalization.

According to the '2025 Top 50 Cosmetic Brands' survey released by the China Association of Fragrance Flavour and Cosmetic Industries, while domestic brands hold a numerical advantage, their brand premium capabilities still lag significantly behind international giants. Data shows that among the top 50 brands, L'Oréal Group accounts for 9, Procter & Gamble for 4, Estée Lauder for 3, Shiseido for 3, Huanya for 2, and LV for 2.

Similar situations exist in other categories, such as the maternal and child market. Over the past few years, domestic brands have successfully seized market share from foreign brands and gained increasing recognition from consumers. However, in the mid-to-high-end market, foreign brands still dominate.

New channels, represented by live streaming e-commerce, have provided domestic brands with a new path to rapidly scale up and expand. However, live streaming e-commerce has also, to some extent, limited the opportunities for domestic brands to become stronger. To maintain sales, brands must sustain high marketing costs, which squeezes resources for product R&D. Moreover, as top influencers consume an increasing share of profits, brands lack sufficient funds to deepen product development and actively invest in self-research.

For instance, Proya, which has surpassed RMB 10 billion in revenue, spends far more on marketing than on R&D. As of the end of 2024, Proya employed 2,195 sales personnel compared to just 389 R&D personnel. In 2024, its R&D expenditure was RMB 210 million, approximately 4% of its sales expenses and 1.9% of its annual revenue.

Overemphasis on marketing at the expense of R&D is a common issue among many domestic brands, and the era of live streaming e-commerce has exacerbated this problem. Now, as the sales miracles created by traffic begin to fade, these brands are reflecting on and seeking to change their strategies.

As for the top influencers who were once highly anticipated, they may soon fall from their pedestal of widespread adoration.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models